The high conviction offshore portfolio

Summary: Many fund managers fail to beat the index as they own too many stocks. Holding larger positions of the right stocks helps to boost performance. I am proposing two high-conviction, actively managed 10 stock portfolios, with different levels of risk and return, from the companies I have been recommending to subscribers. |

Key take out: Start buying now – don't try to time the market. For stocks that have recently had a strong run, buy a bit now and add to the position on “risk-off” days. |

Key beneficiaries: General investors. Category: International investing, investment portfolio construction. |

Only 20% of US equity fund managers beat the market in 2014. Less than one in five active managers outperformed the stock market, according to strategist Savita Subramanian from Bank of America Merrill Lynch. That's the worst performance in over a decade.

BofA data cover all actively managed US large-cap equity funds, including those tilted towards value stocks or growth companies. In fact, according to BofA there has only been one instance in the past 10 years when a majority of active managers beat the index – and that was 2007.

Now the reasons for this chronic underperformance are many and most are outside the scope of this article. But one thing is clear in reading the commentaries of the major fund providers: they own too many stocks. As a result their portfolios resemble and track the market. Genuine alpha generation that significantly impacts return is rare when you hold 80, 90 or 200 companies in a portfolio.

For the last decade and a half, I have been a high conviction portfolio manager, holding between 25 and 40 companies in a global portfolio. According to a Mercer survey of global investment managers who manage funds for Australian investors, I was ranked sixth out of 100 managers over the five-year period to October 31, 2013, generating some 4.7% p.a. over the index. Attribution analysis points to stock selection as the dominant factor in my outperformance. In other words, I held larger positions of the right stocks. Holding far fewer stocks if you are a dedicated stock picker has always made sense to me.

Holding and keeping track of even 25 stocks would be impractical for most Eureka Report subscribers, so I am proposing a high-conviction, actively managed 10 stock portfolio (actually, two portfolios with different levels of risk and return), constructed from the companies I have been recommending to subscribers since last July.

The two portfolios look like this:

Eureka portfolio 1: “Conservative” growth

Google (see Searching for value in Google, December 22, 2014)

Amazon (see Prime time for Amazon, December 15, 2014)

Harley-Davidson (see Harley-Davidson rumbles to life, November 3, 2014)

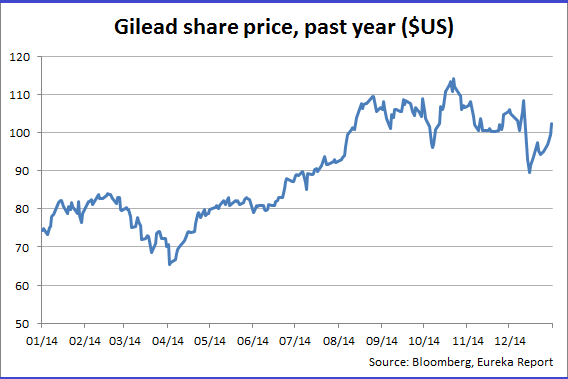

Gilead Sciences (see Gauging Gilead's superior growth, October 27, 2014)

Xilinx (see Xilinx: A global disruptor that's pure logic, July 30, 2014)

Tata Motors (see Tata Motors: Driving a good bargain, September 1, 2014)

Ezion (see Ezion charts a new course, October 6, 2014)

Schlumberger (see Schlumberger: Energised for growth, August 25, 2014)

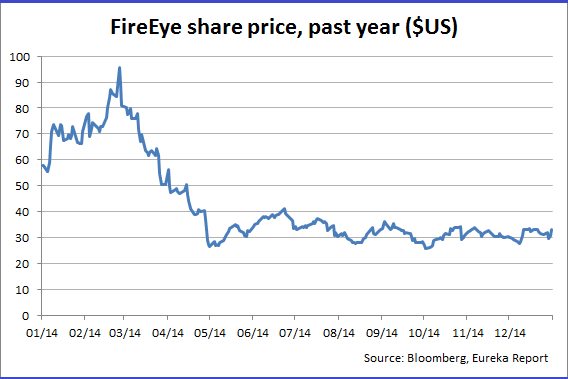

FireEye (see FireEye: Disrupting the cybercriminals, August 11, 2014)

Techtronic (see Techtronic powers up, September 8, 2014)

Portfolio characteristics: Larger market capitalisations, solid balance sheets, growth rates in excess of market, reasonable valuations.

Diversification: Good for a concentrated portfolio, with a nice spread of industries from technology, automotive, energy, retail and biotech. Thirty per cent of the portfolio is non-US.

Eureka portfolio 2: Aggressive growth

Facebook (see Why we like Facebook, October 20, 2014)

Amazon (see Prime time for Amazon, December 15, 2014)

Dow Chemical (see Dow Chemical rouses into action, November 24, 2014)

Gilead Sciences (see Gauging Gilead's superior growth, October 27, 2014)

FireEye (see FireEye: Disrupting the cybercriminals, August 11, 2014)

Splunk (see Splunk: “Big Data”, big opportunities, August 18, 2014)

Ambarella (see Capturing Ambarella's disruptive technology, September 29, 2014)

Celldex Therapeutics (see Celldex: Pioneering a cure to cancer?, October 13, 2014)

Sierra Wireless (see Sierra Wireless is wired for growth, December 1, 2014)

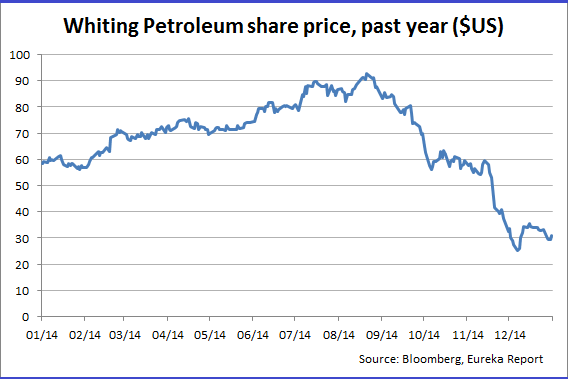

Whiting Petroleum (see Our first offshore stock pick, July 16, 2014)

Portfolio characteristics: Very high top line growth, small to mid-cap bias with a strong emphasis on “disrupters”, low degree of leverage, a high beta “risk on” portfolio, high return potential.

Diversification: Not optimal with a large 50% weight in technology but the companies operate in very different sub-industries that may not be tightly correlated with one another. Heavy US bias.

Portfolio construction and timing

I am suggesting weighting stock positions equally for both portfolios once set up. Each position will represent 10% of the portfolio. Investors can and should adjust portfolio positions over time. For example, if Facebook eventually becomes 12.5% of the fund and the investment thesis is intact, one could always cut it back to 10% and add to laggard positions. Disciplined rebalancing in my experience can add value over time.

In setting up Eureka portfolio 1, one could buy most of the portfolio now. None of the stocks except Gilead have had a huge run in 2014 and GILD has been weak recently. Schlumberger will trade with the oil price so you might want to build the position on down days. FireEye is the most volatile stock in that portfolio so take advantage of it. Cybersecurity, in my opinion, will incur a proportionately large amount of IT spend in 2015 and FireEye is one of my highest conviction buys here.

Eureka portfolio 2, given its weighting in smaller capitalisation and ultra-high growth names, is a slightly different situation. Facebook, Amazon, Dow and Gilead can be bought now. The others – Splunk, Ambarella, Celldex, and Sierra Wireless – have all had some pretty good runs in 2014, so I would look to build positions over time using the individual stock's volatility (and that of the market) to one's advantage. That is, buy a bit now and add to the position on “risk-off” days. Whiting Petroleum, like Schlumberger only more so, is subject to the vagaries of the oil price which I expect will remain will remain volatile over the near term. When the oil price recovers later this year, as I believe it will, Whiting will be a big winner.

No matter which portfolio is being purchased, start now. Don't try and be a market “timer”. The innumerable factors that influence the markets on a daily basis are beyond even the understanding of algorithm-fed super computers. Anyone who thinks they can predict short-term market movements is a deluded fool. The factors that influence individual companies, such as news flow, sentiment, earnings etc are more easily understood and readily available to individual investors, so let's use them.

I intend to actively manage and monitor both portfolios on a daily basis. The investment ideas that are presented weekly in Eureka Report will not necessarily be placed in either portfolio but will instead form part of an investable ideas universe. From time to time, I will recommend selling certain portfolio stocks and buying others.

If pressed, most portfolio managers would admit that the easiest decision to make is the “buy” decision and the hardest is the “sell” decision. My rule of thumb is to sell if I sense a company's fundamentals are deteriorating and the projections of earnings and profitability are unlikely to be met over the medium term. With concentrated portfolios you also need to add fresh ideas from time to time so a stock might be sold if it has appreciated far beyond expectations or seems to lack any meaningful catalyst over the short to medium term. This discipline forces a portfolio manager to only hold what he or she considers are the “best of the best”.