Dow Chemical rouses into action

Summary: The second largest chemical company in the US, Dow Jones, is undergoing transformational change. While it already participates in nearly every niche of the global manufacturing economy, investors have criticized the company for a poor operational track record – and it is acting. Restructuring initiatives, including divesting poor-performing businesses, a cost-cutting program and aggressively buying back common stock, will benefit shareholders over the medium term. |

Key take-out: Dow Chemical represents good value as its business segments – particularly performance plastics – provide strong growth and as it shifts towards specialty products and more efficient production. We have a target price of $US65, reflecting a 25% return at current prices. |

Key beneficiaries: General investors. Category: International Shares. |

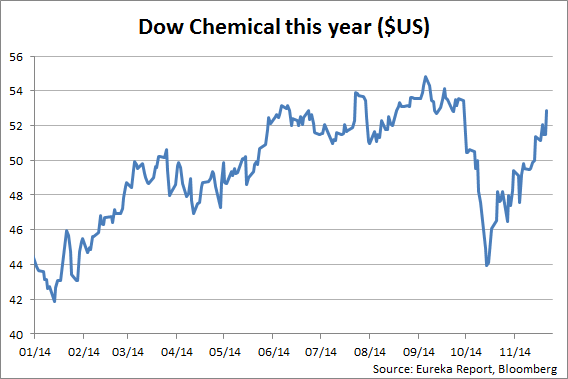

Recommendation: Buy Price at call: $US52.82 Target price: $US65 Risk: Low |

With a market cap of $US60.54 billion, Dow Chemical is the largest chemical company by revenues in the US and the second largest in the world.

In 2013, consolidated sales were $US57.1 billion and earnings before interest, tax, depreciation and amortisation (EBITDA) were $US8.36 billion.

Dow is the world's largest producer of ethylene and chloralkali products, which are the basic components that support its leading cost position as a manufacturer of commodity plastics, polyurethanes, caustic soda, epoxies, and many other basic and specialty chemicals.

Dow is highly integrated, has a broad product portfolio, and it participates in nearly every niche of the global manufacturing economy.

Dow divides its business portfolio into six segments:

- Performance plastics – 26% of revenues and 44% of EBITDA

- Performance materials – 24% of revenues and 16% of EBITDA

- Feedstocks and energy – 17% of revenues and 9% of EBITDA

- Agricultural sciences – 13% of revenues and 10% of EBITDA

- Coatings & infrastructure solutions – 12% of revenues and 10% of EBITDA

- Electronics & functional materials – 8% of revenues 11% and of EBITDA.

Dow is a proxy for global growth in that 36% of the company's sales come from North America; 31% from Europe, the Middle East and Africa, 17% from the Asia-Pacific region and 16% from Latin America.

Being global is always a nice attribute to have in an investment but that's not the main reason to consider Dow Chemical.

Dow is what I would call a “self-help” story: a company undergoing transformational change that will benefit shareholders over the medium term. That's the reason to own the stock.

Australian born chief executive Andrew Liveris is leading the restructuring effort, which involves divesting low margin and non-core businesses, initiating a global cost reduction program, transforming its broad product portfolio, consolidating its numerous and diverse joint ventures (JVs) and aggressively buying back common stock.

To be fair, the timing of this activity and sense of urgency could in part have come from the presence of a pesky “activist” shareholder Dan Loeb of hedge fund Third Point LLC, who early this year publicly criticised the company for its “poor operational track record” and margins which lagged global peers.

Loeb believes the answer lies in breaking the company up and separating the commodity and specialty chemical businesses. Dow has rejected the argument and believes that by executing on earnings and cash flow is the best way to deliver shareholder value.

Dow recently held an analyst day to update the market as to its agenda. Updates included:

- Increasing the divestiture target to a range of $US7-8.5 billion by mid-2016. This increase – which had earlier been $US4.5-6 billion – includes a reduction in ownership of two Middle East JVs. Businesses to be divested are low margin, cyclical and commodity related.

- An announcement of a larger share buyback with some $US5 billion targeted in addition to the $US4.2 billion already done this year.

- A cost-cutting program with over $US1 billion to be taken out over the next three years. A system wide implementation of the SAP enterprise system should aid in these efforts.

- Growth projects are on track with a new high capacity ethylene cracker to be online in the first half of 2017 and a new propylene dehydrogenisation (PDH) facility will be operational by 2015.

Looking at Dow's latest earnings release (October 22, 2014), most businesses are actually doing pretty well.

The company posted top and bottom line results ahead of expectations, driven by its plastics division (Dow's largest) where margins widened on better pricing and lower raw material costs. Earnings per share were 72 cents, a 45% gain year-on-year. Revenues expanded 4.9% to $US14.4 billion for the quarter and all geographical regions participated positively.

EBITDA growth was impressive, expanding 24% year-on-year, and free cash flow came in at $US845 million. Guidance was positive, especially for plastics where Liveris flagged ongoing pricing power into 2015.

Performance plastics – the main growth driver

Of all Dow's six main business segments, performance plastics is providing the most growth. In 2013 this segment accounted for 25% of earnings. Performance plastics is really three businesses: Dow Elastomers, Dow Electrical and Telecommunications, and Dow Packaging and Specialty Plastics. These businesses have broad geographic reach with sales in more than 100 countries in the world.

The performance plastics segment of the company reported revenues of around $US14.6 billion in the last year, with major contributions from packaging and specialty plastics. Recently, this segment reported sales growth of 8.5% to $US3.92 billion in the third quarter, with EBITDA margins increasing to 32.5%.

Major shifts in population demographics, consumer demand for increased convenience, growth in telecommunications networks (specifically broadband and LTE networks), and renewable energy applications are the prime reasons for the strong performance.

Performance plastics has also benefited from the so called “shale boom” in the US. The prices of raw materials such as ethane and naphtha have decreased, providing the company with a competitive edge over its European rivals and higher profitability. Dow has strategically located its polyethylene units near the hydrocarbon cracking facilities in order to enable backward integration into feed stocks.

With strengthening GDP and improving US ethane production, the company's operating rates will move north of 90% in 2015, providing another tailwind for profitability.

Dow has begun construction of its world-scale ethylene production facility in Freeport, Texas, which is expected to be completed by early 2017. The region has accounted for a significant portion of the operating income in the past, and the new project is estimated to yield around 1,500 kilotons per annum [KTA], adding substantially to the output of the company.

The company also has a JV program with Saudi Aramco, the largest oil refining company in the Middle East, to form Sadara Chemical Company – the biggest Middle-Eastern chemical company. Sadara officials reported that Middle East's ethylene capacity is now 20% of global production and the company's world scale operations, supported by strong backward integration to competitive feed stocks, will be a key enabler to drive long-term growth.

It is anticipated that the JV will bring in EBITDA margins of 35-40% and potential earnings for Dow of approximately $US500 million annually during the first 10 years following start-up. This will considerably increase the plastics segment revenues of the company along with a greater exposure to emerging markets in the region.

Recommendation

Dow is a buy at current prices (low $US50s). Even without an activist investor Dow has underlying earnings power in excess of $US5 per share by 2017 and there are a number of growth drivers currently in place (especially in plastics).

A strategic shift towards specialty products and new, more efficient production capacity coming on stream in the 2015-2017 period underpins the investment case.

My target price is $US65, reflecting a modest 15 times 2016 earnings per share (EPS) of $US4.35. At current prices that represents a 25% return.

Risks

- Macroeconomic – a slowdown in the global economy would pressure end market demand for Dow's products.

- Foreign exchange rates – Dow is exposed to numerous currency fluctuations given the global nature of its business.

- Commoditisation of products – some plastics and polyurethanes are at risk.

To see Dow Chemical's forecasts and financial summary, click here.