Why we like Facebook

Summary: Facebook is not the same company it was when its shares dived after listing on the share market in 2012. Chief executive Mark Zuckerberg and his team have succeeded brilliantly in blending the monetisation rates of the social media company's mobile and desktop platforms to produce an impressive growth trajectory, sending its shares to as high as $US79.04 this year. |

Key take-out: I have a price target of $US95 on Facebook, as the high growth and profitability metrics it has demonstrated over the past 12 months should persist over the medium term. You may wish to consider the stock as a core holding in your international portfolio but, as always with highly valued growth stocks, use the volatility of the market to build your position. |

Key beneficiaries: General investors. Category: International Shares. |

Recommendation: Buy Price at call: $US75.95 Target price: $US95 Risk: Medium |

Facebook needs no introduction given its ubiquity and popularity in the social network space. The company is having a great year and is up 35%, handily outperforming the S&P500 Index. But is this a “must have” stock for the global investor and is there still money to be made?

As I mentioned in an earlier piece Investing in technology disrupters, I passed on the Facebook initial public offering (IPO) at $US37 because the user metrics and revenue generation at the time didn't justify the price.

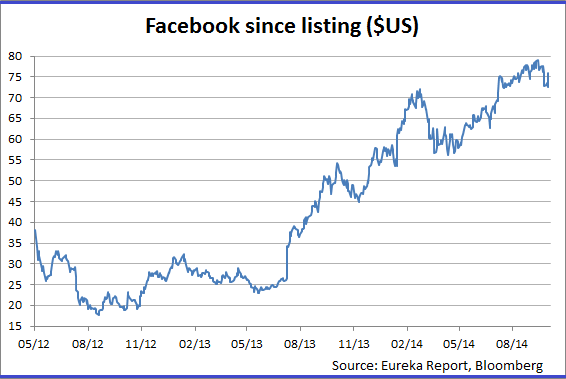

The market agreed and Facebook struggled, finally bottoming out at US$18 in September 2012. That price proved to be a great buying opportunity for my fund. Now the shares are up over 300% at $US73 and trade at a nosebleed inducing trailing price-earnings multiple of 84 times.

Facebook is not the same company it was in late 2012. The catalyst that initially drove the stock from its lows was a clearly articulated strategy to develop the mobile space and not remain solely in HTML and the world of the desktop.

Chief executive Mark Zuckerberg and his team have succeeded brilliantly and have managed to blend monetisation rates of both mobile and desktop to produce an impressive growth trajectory.

Since the IPO they have acquired 15 separate and diverse businesses including industry “disruptors” like Instagram (photo sharing), WhatsApp (mobile instant messaging), Oculus VR (virtual reality), WaveGroup Sound (sound studio) and LiveRail (video advertising).

The company now has over 1.3 billion monthly active users (up from 800 million in 2012) and 829 million daily active users. Around 1.07 million are monthly active mobile users and 654 million are daily active mobile users.

Facebook reported its second quarter results for 2014 on July 23 (the company reports on calendar year) and came in way above even the most bullish forecasts.

Compared to the same time last year total advertising revenue was up 67%, mobile ad revenues grew 153%, average price per ad increased 123% (due to a higher mix of News feed ads), the earnings before interest tax, depreciation and amortisation (EBITDA) margin was an impressive 86% and pro-forma earnings per share (EPS) US42 cents, some 30% higher than street estimates.

That's pretty impressive but the question is whether those growth metrics are sustainable for a company with a market cap north of $US200 billion.

Most estimates, quite rightly, expect revenue growth to moderate over the next three years. Consensus projections estimate revenues to be $US12.2 billion in 2014, $US16.5 billion in 2015 and $US21 billion in 2016.

That's a three-year compound annual growth rate (CAGR) of 39% but reflects a downtrend in growth from 54% in 2013-2015 to 34% in 2014-2015 and 28% in 2015-2016.

Therefore, in order to keep investors happy, Facebook must not only make more money off existing users but also capture a sizable portion of that vast pool of users that aren't on the internet-yet.

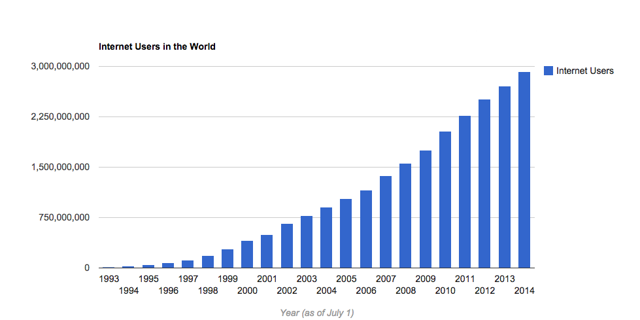

Around 40% of the world's population is connected to the internet right now, according to internetlivestats.com. This compares with less than 1% in 1995. In fact, there's been a tenfold increase in internet users from 1999 to 2013, with the first billion users reached in 2005, the second in 2010 and the third to be attained by the end of this year (see graph below).

Internet usage is expected to increase by another billion users by the end of 2017 if current trends persist. The majority of those will be mobile users in the developing world.

Indonesia is a good example: Internet penetration is less than 20% but 85% of the population is covered by a mobile data network. The challenge for Facebook is to get more of Indonesia's 250 million citizens online. To date there are 69 million “active” Facebook users in Indonesia. The potential is there.

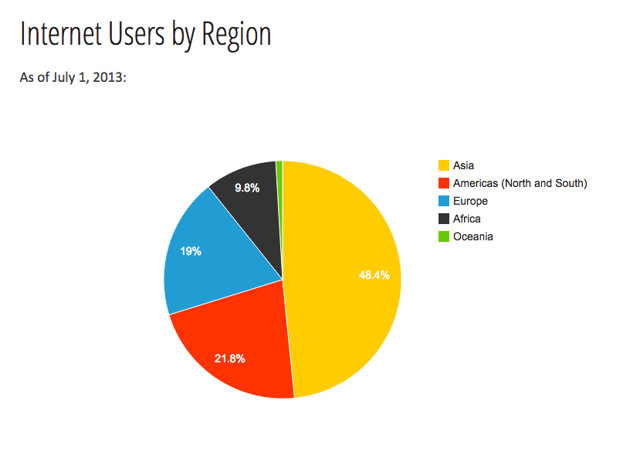

Approximately 80% of Facebook's daily active users are outside the US and Canada:

Conceptually, it's obvious that the existing market is there and the potential total global addressable market is there for the taking.

Facebook and a number of other global technology companies (Ericsson, Samsung, Qualcomm, Nokia, etc.) are working with a non-profit organisation called Internet.org in order to break down barriers and promote cheap access to online services, especially in developing economies.

Zuckerberg, during a visit to India in early October, offered to partner with the Indian government's “Digital India” program using Facebook's platform in order to get the masses online.

The most important driver for Facebook is advertising revenues and particularly higher margin “brand” advertising. Analysts believe that Facebook's recent quarter benefitted from a significant pickup from branded consumer products, automobiles and retailers.

Anecdotal surveys show BMW, Mercedes, and Acura have been very active as have Lay's, Pizza Hut, Kellogg's, and Quaker in the consumer space and Banana Republic and Levis in apparel. Assuming the feedback metrics are positive this is a trend that is unlikely to reverse and should persist into the third and fourth quarters of 2014.

In fact, Facebook's biggest competitive advantage relates to these metrics and ancillary services that Facebook offers the advertisers. The company recently announced that advertisers will be able to target users within one mile of a particular company based on their location. Advertisers can also now know whether a user has seen an ad no matter what device they are using.

Facebook knows who you are, your age demographic and what you like. It's an advertiser's dream come true. FB now has 1.5 million active advertisers overall.

Facebook's captive audience will remain a drawcard for advertisers. Consider that daily active users spend on average of 17 minutes on line. Facebook plus Instagram represents more mobile time than all the other online media providers – YouTube, Pandora, Yahoo!, Twitter, Linkedin, Pinterest, Tumblr, and Snapchat – combined.

Video is becoming more important for Facebook, reporting a 50% growth in views from May to July. The company is averaging over 1 billion video views a day and is rolling out auto-play videos in its news feed in the US. Viral events like the Ice Bucket Challenge are also driving video use. Video should also drive premium rates for video ad prices.

Facebook's growth over the next three years will also be provided by some of its recent acquisitions. Consider WhatsApp, which was recently purchased for $US22 billion in one of the largest internet transactions in history. This is a company that is growing monthly active users(MAU) in the instant messaging space 100% year-on-year. Over the past five months WhatsApp has been one of the top four apps downloaded globally.

While impressive, that makes WhatsApp only the seventh most popular service in the US (Facebook Messenger is the most popular, followed by Skype). Combine Facebook and WhatsApp, however, and you have the 800 pound gorilla of the global messaging space with over 700 million MAU even when allowing for some overlap (50%), attrition, etc. That's almost double that of WeChat, and 3.5 times that of Twitter.

Facebook is also considering introducing a purchasing function to the platform called “Facebook Buy”. It's early days and in a crowded space (Paypal, Amazon, Apple and Twitter are all active here) but assuming the company could leverage its vast user base this could be another engine of growth in the future.

Keeping users within your own ecosystem pays off. Just ask Apple.

Valuation

Facebook is trading on an 2014-15 EPS multiple of 33.6 times in 2015. One could make a case for purchasing at the stock at roughly one times three-year growth rate or less.

That's not a big ask, given Facebook growth metrics or those of growth stocks in general so I'm a buyer here with a target price of $US95, representing 35 times 2016 EPS of $US2.70.

As a check let's consider enterprise value (EV). Conservatively we can put the following values forward:

Total ($US billion) | Per Share ($US) | |

Core | 202 | 68 |

19.4 | 6.5 | |

21 | 7.25 | |

Net Cash 2014 | 10.5 | 3.55 |

Implied Equity Value | 252.9 | 85 |

(Shares outstanding are 2.9 billion in 2014)

Facebook's enterprise value at $US85 is not too far away from my target price.

Conclusion and recommendation

Facebook is a “buy” and, while I dislike the term “core holding”, this company is about as close as you can get to one. I believe that the growth and profitability dynamics demonstrated by the company over the past 12 months will persist over the medium term.

That being said, FB will have to consistently monetise the mobile business while defending a static (or declining) desktop business, as well as give investors a clear sense of how recent acquisitions will drive growth going forward.

Given the scale and reach of the company I believe they will succeed, so I would be a buyer at current prices (the stock is off some 9% from its highs).

As I always say in relation to highly valued growth stocks, use the volatility of the market to build your position.

Facebook reports its third quarter financial results on October 28 after the market closes. I expect a continuation of second quarter trends and analysts will be still trying to “keep up” with the growth in mobile ads and video.

Risks

- Founder risk. Investing with visionary founders like Mark Zuckerberg (Facebook), Elon Musk (Tesla), Larry Page (Google), and Jack Ma (Alibaba) has its risks and rewards. Founders may not always act with shareholder's best interests. Facebook has a dual class share structure (A&B) that does not benefit shareholders. Zuckerberg's Class B shares give him 10 times the voting power of A Class shareholders. Founders can be removed as Steve Jobs was in the 1990s. “Key man” risk is high in these companies (Could Sheryl Sandberg – the chief operating officer – take over?).

- Privacy issues. Facebook admitted to manipulating the emotional content of users without their knowledge. The public will remain extremely sensitive to similar invasions of privacy. Further breaches could have a negative revenue effect.

- Fatigue and saturation factor. The most active daily users are from the youngest demographic. They are fickle and could flock to the next “big thing”, whatever that may be. A recent user survey reported 30% of respondents admitting less daily activity on FB.

- Acquisition risk. Facebook's recent acquisitions have been expensive and may not pay off. Ill-timed and poorly thought out future purchases may dilute existing shareholders.

To see Facebook's forecasts and financial summary, click here.