Prime time for Amazon

Summary: The world's largest online retailer, Amazon, has lost some of its appeal to the market of late as investors lose patience about profitability. But make no mistake, Amazon is a dominant and disruptive company, with 250 million active customers and huge top-line growth forecast. If it can temper its investment spend on devices like the Fire Phone and instead focus on increasing its scale in developing markets and squeezing profitability out of Amazon Web Services, its future will be bright. |

Key take-out: The noise around profitability appears to have mispriced Amazon's business. I would buy at current levels, as I expect the stock to play catch up in early 2015. |

| Key beneficiaries: General investors. Category: International Shares. |

| Recommendation: Buy Price at call: $US307.32 Target price: $US400 Risk: Medium |

Amazon may be the world's largest online retailer, generating $89 billion in revenues this year, but it was one of the worst performing stocks in the S&P500.

The stock is off 20% in a market that's up 12% as investors finally lost patience with the company due to its oversized spending in infrastructure and device related businesses at the expense of profitability.

Amazon is absolutely dominant in the online retailing space in the US with a 50% market share and is the number one in many international markets. It is the world's most disruptive retailer, with over 250 million active customers.

Revenues are still forecast to grow at 20% plus over the next three years (remember, this is a company with a market cap of $US136 billion). Not only that, but Amazon consistently outpaces online retailing growth. For example, Amazon “Cyber Monday” sales were up 13.7% versus an increase of 8.1% from the industry.

Australians don't see the full-blown Amazon offering. Click on the local website and it's mostly books, e readers, etc. In the US and many other international markets it offers everything from consumer electronics, music, videos, home and garden supplies, groceries, beauty products, toys, sporting goods, automotive gear, clothing, and jewellery. US customers can access over 230 million items provided by Amazon or third party sellers with a click of a mouse or via their mobile phone.

Amazon's value proposition is the low price of its goods and fast delivery – sometimes the same day. In New York City the company is trialling a program using bike messengers that would give your order in an hour or so! Meanwhile, Amazon “Prime” customers get deliveries for free and other benefits.

So the company is dominant and disruptive – what's not to like?

Well, if Amazon continues on its current track, aggressively investing in infrastructure at the expense of profitability, and continues to post outsized losses as it has done in two of the past three quarters, then I'd prefer to sit on the sidelines.

However, if the company tempers its investment spend, de-emphasises it's device strategy (the Fire Phone was a flop), increases scale in its developed markets businesses (Japan, Germany and the UK) where it has considerable share positions, and squeezes some profitability out of of AWS (Amazon Web Services), then that would be interesting – particularly if upon analysis there is a mispricing of Amazon's business due to all the noise surrounding current profitability.

Amazon has three distinct businesses:

- eCommerce (online retail)

- Amazon Web Services (AWS)

- Digital devices and media (Kindle and eBooks)

The core online retailing business is almost evenly split between the US and the rest of the world. Through first mover advantage, Amazon has the number one market share worldwide, as well as in the US, Germany, and the UK. It leads the number two and three ranked players such as eBay and Alibaba by a considerable amount. In Japan, it is second behind Rakuten, but not by much.

Amazon's eCommerce business has grown at a 27% compound annual growth rate (CAGR) between 2010 and 2013. In contrast, the total core market has grown 16%. In the more mature markets of the developed world, Amazon is expected to maintain its leading position through a combination of faster fulfilment and better customer service as well as its popular Prime subscription services which offers free delivery and special offerings.

Source: Businesswire

There are currently 30 million Prime subscribers who pay $US99 per annum. Research has shown that prime members have a much higher spending per order and tend to be more active in the higher margin categories such as shoes, consumer electronics and clothing. The churn rate is low. 90% of subscribers renew.

Mobile eCommerce growth should also sustain growth rates and market share. Currently their sales are but 8% of the total. Some analysts see it expanding to 40% by 2018. Amazon is well prepared for this with heavy investment in compatible infrastructure and encourages mobile users with special deals that they can get only if they use their phone to order.

Products on Amazon's websites are also provided by third party (3P) providers. Amazon's fulfilment business for 3P accounted for 36% of all 3P merchant business in the US. Given Amazon's logistics skill and fulfilment power, that percentage is expected to increase.

AWS is Amazon's “cloud' platform and provides what is called in the industry IaaS or “Infrastructure as a service”. AWS or Amazon Web Services is growing revenues at 40% plus and has an operating margin of 10%.

Unlike its competitors, AWS has historically employed more of a “retail based” strategy emphasizing, lower costs and a “one stop shop” for all the cloud services. Some analysts have flagged a shift to winning and keeping business with value added services not just price. Given Amazon's high level of investment this would be a positive and pave the way to earlier than expected profitability.

Amazon has had to make large investments for data centres, headcount and related infrastructure. It is estimated that AWS has one million clients and two million servers online, giving it scale that competitors (Microsoft, Google, etc.) can't match. The business should be profitable by 2017 and generating revenues of $US18 billion by 2018. Amazon has a dominant share of the cloud IaaS market, estimated at over 50%.

End markets for “the cloud” and related services are extremely attractive. According to Gartner Group the IaaS market will grow from 9 billion in 2013 to 36 billion in 2018 at which time some 25% of all computing functions globally will be in the cloud.

Amazon's device business brought in millions of customers to the Amazon ecosystem but the proliferation of smartphones and tablets is pressuring Kindle sales and eReaders in general. Market research firm IDC predicts that the demand for eReaders will decline 27% between 2012 and 2017. Clearly this is not a growth business any longer and should be de-emphasised in Amazon's strategy going forward. The Kindle should be an App – not a device.

That being said, eBook revenues should still expand at a healthy rate as former Kindle users continue to order digital media products through Amazon for their phones and tablets. Amazon has a 60% share of the global eBook market and revenues could reach $US11 billion by the end of 2016.

Over the past five years Amazon has generated $US10 billion of free cash flow and only $US2.9 billion of net income. A critical observer might say founder Jeff Bezos doesn't care about profitability or the stock price. I think that conclusion is wrong.

No Amazon employee receives more than $US175,000 in annual cash compensation; any remuneration above that level is paid in company stock. Therefore, weak stock price performance could hurt employee morale and retention, and hinder the ability for to attract industry-leading talent. It's unlikely, in my opinion, that Mr. Bezos and Amazon's management don't care about the stock price.

Valuation

If that's the case, what is Amazon worth and should we buy the stock?

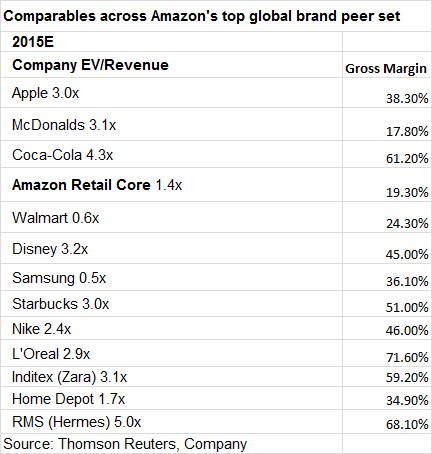

Amazon's retail business is cheap relative to a universe of global branded peers. Walmart is cheaper but isn't growing anywhere near 20% per annum. Amazon is estimated to have a market share of 12 times that of Walmart.

It is cheap relative to historical multiples of enterprise value to earnings before interest, tax, depreciation and amortisation (EV/EBITDA) and EV/sales as well.

We can arrive at a value for the core retail business alone using the EV/sales multiple and a figure representing “gross merchandise value” (GMV) which is the total value of merchandise sold over a given period of time through a customer to customer exchange site. It is a measure of the growth of the business or the use of the site to sell merchandise owned by others (that's Amazon products and the 3P sellers).

Amazon's current EV/GMV multiple is 1.4 times, which implies an equity value of $US180 billion just for the core retail business. When you add $US13 billion in net debt and divide by fully diluted shares outstanding (461 million), you get an implied value of $US419. Amazon is trading at $US305.00.

At that price it looks like we can get AWS for nothing! Assuming AWS becomes profitable by 2017 this business could be worth some $US30 billion after 2018 (EV/revenue of 4.8 times – similar to peers).

A conservative “sum of the parts” exercise whereby we assign a multiple derived from industry comparables to each of Amazon's businesses gets a similar value:

- 16xEV/EBITDA core US division

- 0.5xsales International

- 4xsales AWS

- 2xsales of other businesses (Kindle and Media)

The total comes to $US410.00, where 90% of Amazon's value is in the core US business and in AWS.

Recommendation

I'd be a buyer at current levels, with a target price of $US400. I expect the stock to play a bit of catch up early in 2015.

Amazon reports its fourth quarter 2014 results on January 30, 2015. I expect good numbers, at least on the top line. The fourth quarter is traditionally Amazon's strongest and seldom disappoints.

Anecdotally, post-Thanksgiving sales were very strong. Industry consultancy Channeladvisor just reported that Amazon's November same store sales were up 36%. It could also mark an inflection point for better stock performance.

Risks

- Price wars with IaaS competitors may lead Amazon to cut AWS prices further while Incremental AWS investment offsets cuts elsewhere (EM businesses).

- Weakness in core market retail sales could hurt growth.

- Write-downs from struggling investments (e.g. Fire phone and China business) could continue to be a margin drag.

- The timing of any material reduction in investment spend is unclear although it will happen. More losses and weakish sales could pressure the stock.

To see Amazon's forecasts and financial summary, click here.