Wesfarmers moves closer to value

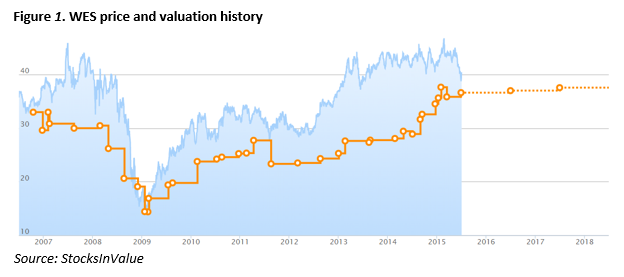

When we last updated in February Wesfarmers Ltd (WES) was overvalued and trading around the 12-month high of $46.95. The lofty price partly reflected strong demand for stocks with high earnings certainty and secure dividend growth, a product of Australia's ageing population and low interest rates. Investors were taking on capital loss risk for the high dividend.

We thought these forces might keep the price elevated, however WES is down about 15 per cent reflecting the broader market falls and possibly concerns over the trajectory of international discounters Aldi, Lidl and Cosco. It is now closer to our $36.58 valuation.

WES's performance is tied to broad domestic economic conditions (and New Zealand to a lesser extent). It is Australia's largest conglomerate with diversified operations in retail, resources and industrial products.

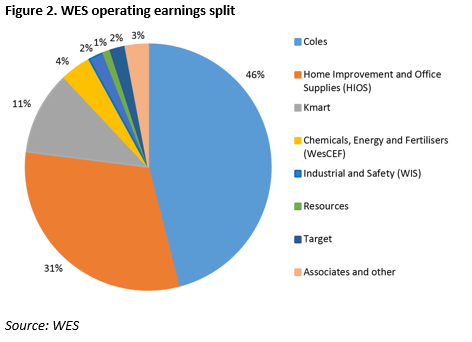

Retail is the company's primary business and includes some of Australia's major outlets - Coles, Bunnings, Officeworks, Target and Kmart. Coles accounts for close to 60 per cent of group sales and 46 per cent of group operating earnings and is the main determinant of value. Home improvement (Bunnings and Officeworks) and Kmart are another 31 per cent and 11 per cent of operating earnings, respectively.

Grocery, Bunnings, Officeworks and Kmart are all growing steadily despite the weak broader economy. Reduced confidence in the economic outlook, another tough May Budget and below-trend GDP growth at about 2.3 per cent contribute to weak consumer sentiment. WES's resilient performance reflects the non-discretionary component of its sales and its ability to drive lower prices with efficiency gains.

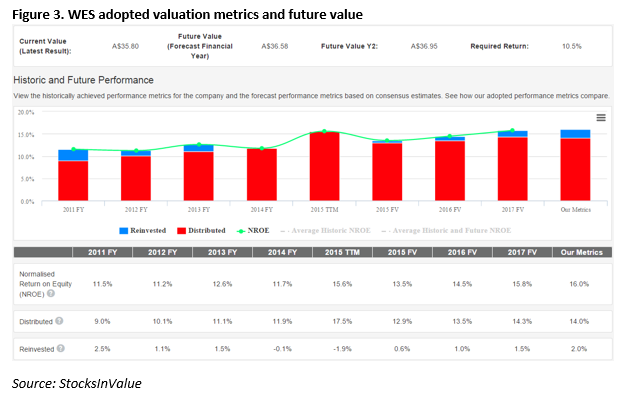

Our forecast normalised return on equity (NROE – where the “normalised” means the inclusion of franking credits) of 16 per cent is higher than the average of the last five years (FY10-FY14) of 11 per cent, reflecting our view profitability will continue marching upwards. The normalised return on incremental equity over the same period was about 40 per cent. The reason for the wide disrecrepancy between returns on total and incremental equity is WES overpaid for Coles in 2008, which diluted NROE. It is the main reason for the high proportion of goodwill on the balance sheet, which is about 59 per cent of equity.

Our NROE assumes mid-single-digit revenue growth at Coles, consistent with about 3-5 per cent industry growth and market share gains from continued reinvestment in prices and operational improvements. Coles has outperformed Woolworths on comparable store sales growth for a number of years. The NROE also assumes flat to slight increases in margins at Coles over the medium term.

Increasing competition in the Home Improvement (Bunnings) segment is unlikely to materially affect WES earnings or margins in the near term. WES has the largest market share at about 20 per cent. The industry is fragmented and there is room plenty of room for both WES and Woolworths (Master's) to grow. Home improvement continues to be the standout for the group, with improved sales momentum and growth in all regions and customer segments.

Kmart should also continue mid-single-digit growth over the medium term driven by store rollouts, improved ranges, strong inventory management and cost controls. Target is struggling with price deflation in its product mix and is WES's weakest retail segment.

Trading conditions for WES's Industrial segment remain challenging due low gas and coal prices. Eventual recovery of commodity prices will take time as the oil and gas and coal industries consolidate and reduce excess capacity.

Our low required return of 10.5 per cent reflects good financial health, with gearing at 19 per cent net debt-to-equity (on December 31) and consistent cash flows. WES has dominant market positions and scale in its main businesses, a strong management team, and a track record of growing earnings and widening profit margins.

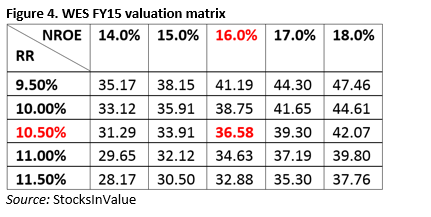

NROE is split 14 per cent/2 per cent between dividends and earnings reinvested. We derive an equity multiple of 1.6 times, which is multiplied by FY15 equity per share of $22.53 to produce an intrinsic value of $36.58, rising to $36.95 in FY16. These metrics imply value growth of about 2 per cent per annum. The valuation's sensitivity to different assumptions is:

The bullish case (right side) includes earnings upgrades from the core grocery and home improvement segments, and improving conditions in the Australian economy increasing earnings within the home improvement, office supplies and retail divisions, which are tied to discretionary consumer spending.

The bearish case (left side) includes increased competition, price deflation, a cyclical downturn affecting WES's home non-discretionary businesses, or possible expansion into markets outside WES's traditional areas of expertise given its flexible balance sheet and slowing revenue/operating income growth.

Lately market discussion has centred on the potential disruption posed by Aldi.

Since entering the Australian grocery market in 2001 Aldi has grown rapidly and now has about 5 per cent (UBS estimate) of the market, almost entirely at the expense of the Metcash and the independents, which collectively have about 32 per cent share.

WOW's share has remained flat in recent years at about 37 per cent, while Coles's share has slowly increased to about 26 per cent. We think Coles, Woolworths, Aldi and Costco can all gain share from the independents and specialists over the medium term.

The question is whether Aldi can force the majors' margins lower. The difference between Aldi and the majors is Aldi offers a limited product range and only one or two brands within each category. It pays lower prices to suppliers in return for higher and more secure volumes. It also targets much lower margins (less than half) than the majors.

Aldi and Lidl have set a precedent in Europe where the larger incumbents' margins have reduced significantly over time. However, the Australian market is far less fragmented, more geographically dispersed and hasn't experienced the same recessionary conditions that favour the discounters. The worst case scenario, which is not our base case and would not occur for several years, is Coles's margins compress by about 2 percentage points, resulting in about 20 per cent lower profits for WES. In this case NROE would be 2-3 ppts lower and WES would be worth $29-31, all else being equal.

Disclosure: Our fund partner Clime Asset Management owns shares in WES.