Retail Food Group stumbles

Retail Food Group is one of Australia's largest multi-food franchise operators, operating well-known brands such as Brumby's, Donut King, bb's café, Michel's Patisserie, Esquires Coffee, Pizza Capers, Crust Gourmet Pizza and the Coffee Guy.

The stock has been a star performer in the Australian small company's space, having increased in value by six times in the last six years.

Earlier this year we wrote about how RFG has recently undertaken a number of transformative acquisitions that will likely deliver two years of clearly defined earnings growth. We argued that despite strong growth in gross profit and dividends, the underlying performance of RFG's legacy businesses appears to have been somewhat mixed in recent years.

In early June management provided an update to the market, which (1) highlighted that a number of the legacy businesses are facing challenges (2) outlined a business restructuring to place greater emphasis on an international strategy and (3) provided a trading update.

Write down in traditional business units

In the last 12 months RFG has made three significant acquisitions along the coffee supply chain. Specifically, the company has acquired Café 2 U, Gloria Jeans Coffee and Di Bella Cofee.

While the combined acquisitions will make little contribution in FY15, they should add in excess of $30m earnings before interest and tax (EBIT) to the group's current earnings base from FY16.

RFG's traditional coffee businesses, however, have been underperfoming. As a result the company has announced an $18.5m non-cash impairment of bb's Café and Esquires. Where appropriate these businesses are to be converted to Gloria Jean's or Michel's Pastisserie stores.

With the integration of these legacy businesses into the recently acquired businesses resulting in the recognition of impairments, we would raise the question as to whether or not any of RFG's other legacy businesses are struggling.

Since listing, the company has acquired Brumby's Bakery, Michel's Patisserie Brand System, Esquires Coffee, Evolution Coffee Roasters, Crust Pizza and others. Such rapid growth via acquisition makes it difficult to analyse the true economics and performance of theses businesses. Accordingly, sometimes it is useful to step back and look at the economics of the group as a whole in order to draw inferences.

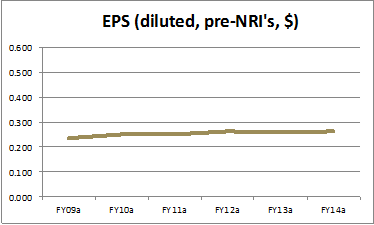

Accordingly, it is interesting to note that despite a six fold increase in share price since 2009, earnings per share has remained largely unchanged.

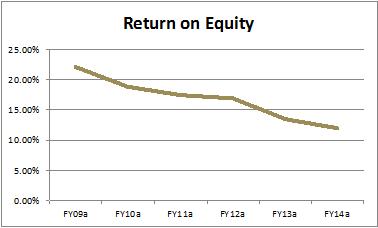

Equally as important, we note that RFG's return on capital has been consistently declining in recent years. In our view, both of these factors raise some questions marks over the productivity of the group's legacy businesses.

Business restructuring

Retail Food Group has announced a number of business restructuring initiatives. Key elements include:

- Management: separation of the chief executive and managing director function. Tony Alford will remain the MD. Retiring chief operating officer Andrew Neil has been appointed chief executive. Franchise while former Director of Franchise, Gary Alford, has been appointed chief executive Commercial.

- Board: Non-executive director Jessica Buchanan will resign from the board to assume the role of Chief Brand Officer. RFG is currently recruiting for two non-executive independent directors to strengthen the board.

- Additional synergies at additional cost: RFG has announced that its targeted efficiency gains to be delivered by FY17 have increased from $13m to $16m. These gains involve a cash commitment of $16.3 (previously $13m).

Many of these changes are being put in place in order to facilitate an expansion internationally. Following the acquisitions of Gloria Jeans, IAG, Café 2 U and Di Bella coffee, management believe that the company has established a sustainable international platform.

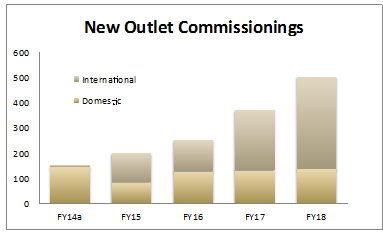

By FY18 the company expects international commissioning to represent 70 per cent of new store growth.

While it may be true that a strategy of regional licensing and entering into local joint ventures reduces the inherent international expansion risk, this is a new business venture for RFG management and remains, at this early stage, largely unproven. Clearly, this strategy adds additional risks to the investment case for RFG.

Trading update

The company reiterated FY15 earnings guidance and expects to report full year net profit after tax (NPAT) pre non-recurring items of $55m. Management continues to highlight that this is an increase of 50 per cent on that delivered in FY14. However, adjusting for additional capital raised results in an increase in earnings on a per share basis by roughly half this amount. Nevertheless we expect RFG to deliver robust EPS growth at 26 per cent.

Our thoughts

We have incorporated the recent announcement and trading update into our earnings forecasts for RFG.

The key question facing investors in Retail Food Group is this: What is the right price to pay for a business with two years of clearly defined acquisitions-based earnings growth that has some question marks around the growth outlook of a number of its legacy businesses?

On the basis that management achieve their integration and synergy targets of recent acquisitions, RFG is currently trading at around 13 times FY16 earnings. This suggests that the current share price is already discounting the much of the potential success of the recent acquisitions. Considering the increased risks associated with an international expansion strategy and that the successful integration of recent acquisition appears largely priced in, we retain a “hold” recommendation.

To see Retail Food Group's forecasts and financial summary, click here.