Qube's capital raising success

The retail demand for the Qube Logistics (QUB) capital raising was very strong, with 78.9 per cent of eligible shareholders taking up their one for 4.4 shares entitlement offer. There was also strong demand for additional shares beyond the entitlement offer amount. The final scale back was 62.12 per cent of additional new shares (beyond the entitlement).

The new shares commenced trading on April 11 and less than a month later the stock is at $2.50 - approximately 22 per cent higher than the $2.05 offer price.

The total amount raised in the retail offer was $244 million, combined with the $250m institutional raising for $494m additional funds as planned. As previously discussed on the March 16 – read more here: - the funds will be utilised for the consortium takeover bid of Asciano (AIO).

With adequate funds raised there are now two key remaining steps for a successful takeover of Asciano. The first one is the ACCC decision, due on May 26, and then the Asciano shareholder vote in early June.

The complex structure between Qube, Brookfield and other consortium partners was carefully designed in an attempt to ease prior regulatory competition issues. Previously when the ACCC assessed Brookfield's takeover offer, it was concerned with its plan to combine its WA rail track operations with Pacific National's rail haulage operations.

In early April, after initial assessment of the new offer between Qube, Brookfield, and six international investment funds, the regulator said it has concerns over the cross-ownership stakes between some of the consortium partners. It was stated: “The ACCC considers that these underlying commercial relationships may lead to a level of common financial interest within the consortium despite the division of the proposed acquisition of Asciano into three separate components. The ACCC will therefore take these commercial relationships into account in its review of each of the rail acquisition, the ports acquisition and the BAPS acquisition."

With industry submissions due to the ACCC by April 18, it appears – importantly – that the shipping industry is backing Qube in as a potential new owner. Ken Fitzpatrick, chairman of industry group Shipping Australia, which represents shipping lines and agents, said Qube would make a good owner of Patrick ports because it was already familiar with ports. “I think I'd feel more comfortable with Qube in there than some of the other potential buyers of Asciano because they know the business".

There are some locations where there could be market power concerns, but it is unlikely that any of these isolated concerns will block the deal all together. Qube would have been in communication with the ACCC for a long time now, and as such most of the deal blocking issues have likely been addressed.

If the Asciano deal is approved…

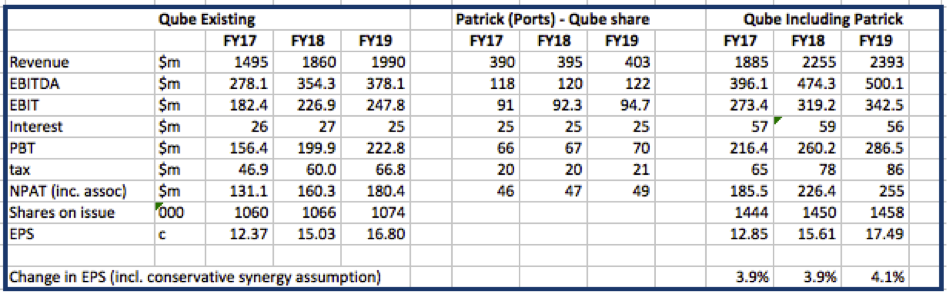

In the short term, on a worst case basis (ie. assuming low end of synergy guidance range), the deal is likely to be earnings per share neutral for Qube's FY17 earnings. That is, the positive earnings benefit from Asciano's ports business is equally matched by the debt and equity funding costs.

In the longer term after synergies are realised, the deal is likely to be earnings per share accretive and is also strategically very important.

The strategic positive is greater control of the container supply chain, where the benefits will increase as the Moorebank intermodal terminal volumes ramp up over the next decade.

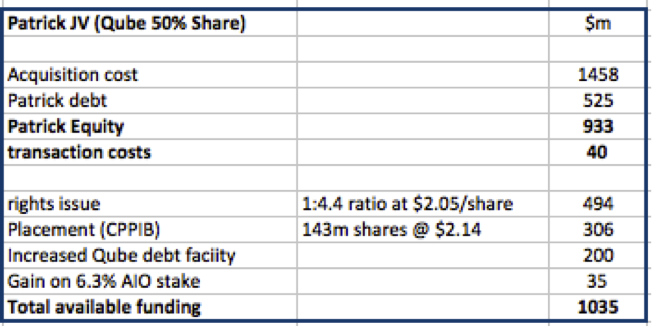

Qube is paying $1.46bn for its 50 per cent share in the Terminals joint venture. It is to be funded by $800m in new equity and debt of approximately $200m, on top of the $1.05bn debt from Patrick (Qube's share is $525m).

For the equity component, $306m is raised from CPPIB's agreement to acquire 143 million shares at $2.14 per share, and $494m from the previously mentioned retail and institutional non-renounceable entitlement offer. The CPPIB equity component is conditional on the transaction been approved.

The $1.05bn of Patrick non-recourse debt comes at a cost of 3.2 per cent. Transaction costs are estimated to be $40m, on top of the $160m debt Qube guided towards. A profit of around $35m will be achieved from Qube's 6.3 per cent stake in Asciano.

If the deal is completed in June, it provides the opportunity for one-off costs to be recorded in FY16, and a clean full FY17 year of the combined business.

Upside scenario

Management has guided towards $30-50m of synergies from the deal over a two to three year timeframe. The top end of this range would be equivalent of up to five per cent earnings per share accretive.

Over the longer term it is challenging to quantify the benefits of continued integration of the container supply chain, for example as Moorebank volumes increase, and warehousing customers build capacity on site at Moorebank. But there is little doubt that greater control of container movements will ultimately provide cost savings.

The cost of the import/export container supply chain is believed to be $1500 per TEU container - that is from ship to retail store. Qube management's long term view has been that it can reduce the costs of this supply chain through a more integrated service that reduces some of the unnecessary steps.

Summary

With the deal not yet approved, our Qube forecasts don't yet include the impacts from the potential transaction. However, as mentioned, on a pro-forma basis the worst case is for the deal to be EPS neutral for FY17, and accretive over the longer term. The deal is likely to create substantial value for Qube, and it de-risked the business model by owning a larger component of the container supply chain.

Short-term earnings multiples for Qube look inflated compared to Aurizon (AZJ), and the price Asciano (AIO) traded on prior to takeover bids, though in our view this is justified given current non-operating assets that will produce significant earnings in future years (eg. Moorebank, and Quattro grain).

We maintain our long term buy recommendation with a $2.65 valuation, and further upside if the Asciano deal is approved.