Proofpoint proves its worth

On August 11, 2014, I recommended that Eureka investors buy FireEye, a leading vendor of IT security solutions for the enterprise. In the published note, I chronicled the increasing threats of cybercrime:

“Cyber-security is a non-discretionary area of IT spending for any corporate or government entity, large or small. It is also the fastest-growing sub group of IT spending. The total addressable market has been estimated at more than $US30 billion. Recent corporate breaches that have been made public include eBay, Target, Neiman Marcus, Evernote, RSA (an IT security specialist!), the New York Times, Sony's play station network, and the “Heartbleed” bug, which caused Facebook, Amazon, Yahoo, and Google to urge users to change passwords.

Government agencies such as NATO, Canada's National Research Council, the Montana Department of Health, the Israeli “Iron Dome” contractors, and even the US Federal Reserve have been compromised recently. In 2012, two major US banks, Wells Fargo and Bank of America, suffered denial of service attacks; banks, brokers and financial institutions remain under threat on a daily basis.”

Since then FireEye, consistently one of my highest conviction stocks, has appreciated over 60 per cent and the outlook for IT spending on cybersecurity is as strong as ever with breach activity reaching epic proportions. The most recent security breach was a massive digital theft of millions of US federal workers' data (social security numbers, security clearances, health status, etc.) from the Office of Personnel Management.

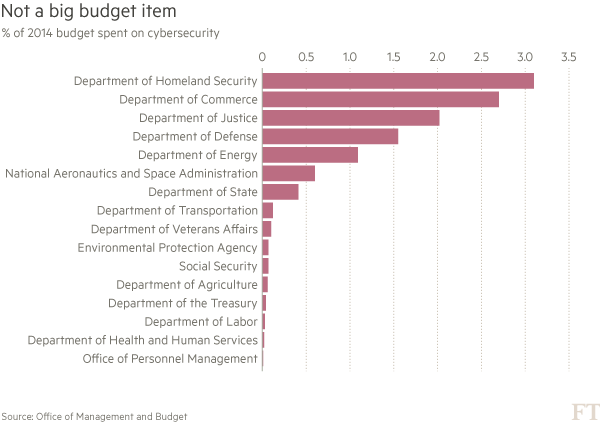

The US public sector is particularly vulnerable due to obsolete legacy IT from a lack of spending.

IT spending on security, which was very strong in 2014, is poised to accelerate in 2015/16. There is definitely room for more than one cybersecurity play- hence my interest in Proofpoint. The longer term outlook is truly astonishing. See “Postscript” at end of article.

Proofpoint

Proofpoint was founded in 2002 by Eric Hahn and is headquartered in Sunnyvale, California. It is a security-as-a-service provider (SaaS) focusing on cloud-based security solutions for the email gateway market. It also offers advanced threat protection (APT), compliance, archiving & governance, as well as secure communications.

The company has four “solution” lines: Proofpoint Enterprise Protection, Proofpoint Enterprise Privacy, Proofpoint Enterprise Archive and Proofpoint Enterprise Governance. It offers a ‘one-stop shop' for email gateway, with many add-on capabilities that allow it to upsell to existing customers.

Proofpoint is a third of the size as FireEye and operates almost exclusively in the email/messaging realm whereas FireEye looks at the entire enterprise. According to US telco Verizon's recent “Data Breach Report”, 95 per cent of targeted attacks begin with “spear-phishing” via email, requesting recipients to open or download a link. This gives Proofpoint direct access to the largest single avenue of attacks in the world of cyber-crime. The ultra-damaging Sony attack originated in emails retrieved from key personnel.

While market growth rates are important to all the players in IT security, the most important metric for Proofpoint going forward is gains in market share in the core email gateway market, especially with its relatively recent “Targeted Attack Protection' (TAP) product. This product has grown 100 per cent year-on-year over the past four quarters.

Proofpoint's TAP guards against what are called “zero-day threats” which simultaneously attack the enterprise via email gateways and exploit an unknown computer security vulnerability. The secure email gateway has traditionally been the realm of security giants Symantec and Cisco (Ironport) with market shares exceeding 25 per cent each. At present, Proofpoint owns but 8 per cent of the market but is gaining new customer acceptance as its products are lower cost and easier to deploy from the cloud as opposed to “on site”. Many analysts see a 19-20 per cent share by FY18.

The company has also recently extended this solution for social media given that many companies use social media to market their products and interact with customers via Facebook, Linkedin, and Twitter. All things being equal this should be an incremental source of additional revenue for its core products.

While Proofpoint has gained a reasonable foothold in the Fortune 100 market (49 per cent are customers), it has but 27 per cent of Fortune 500 companies so there is significant room to expand and gain market share.

Proofpoint is currently very US centric with over 81 per cent of revenues in North America. Management has flagged a greater European presence going forward, especially targeted at the large enterprise.

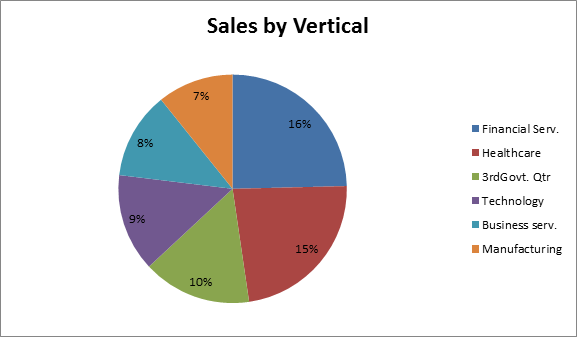

Proofpoint's customer base is well spread and diverse.

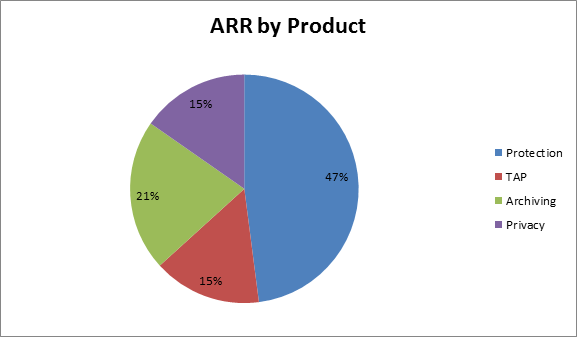

By product, Protection is almost half of annual recurring revenues and TAP introduced in 2012 now represents 15 per cent of ARR and is growing fast (100 per cent in 2014). Proofpoint has a strong track record in cross selling and “up” selling to the extent that more and more of the existing customer base (over 40 per cent at last count) is using multiple products.

Growth and revenue assumptions

Assuming Proofpoint reaches 400 million in revenues in 2017 (my estimate) the company will have grown sales at over 30 per cent per annum since 2012. Proofpoint is another “growth now, profits later” company, like other high growth companies we have recommended (FireEye, Splunk, Mobileye, etc.) The company believes it will be eventually reach $US1bn in revenues.

I have Proofpoint generating positive earnings per share (EPS) of $US0.30 by 2017. The company has been cash flow positive since 2013 and is estimated to deliver cash flow of $US1.00 per share in 2015 and $US0.51in free cash flow (FCF) per share share. These estimates could be understated if Proofpoint grows recurring revenues more than anticipated.

Recommendation

Proofpoint is a “buy” at current prices. A large addressable market, innovative products and the necessity for strong cybersecurity IT spending from both business and the public sector should underpin Proofpoint's growth going forward.

Our target price is $US80 which assumes that PFPT can trade at 7.5 times enterprise valuation (EV) to sales in 2016. Currently it's trading at 10.5 EV/Sales.

Risks

The company is on the verge of making a profit, which I believe it will do by 2017. However, if it cannot achieve the profitability forecast and within the time frame, FCF is likely to be harmed and thus the valuation.

The email gateway market, Proofpoint's core market, is a mature and highly competitive. If it is not able to gain meaningful share, growth is likely to slow sooner than expected, leaving the valuation in question. If customers view its technology as undifferentiated to peers, and thus not be able to replace its bigger competitors to create new opportunities, it could further slow growth.

Postscript

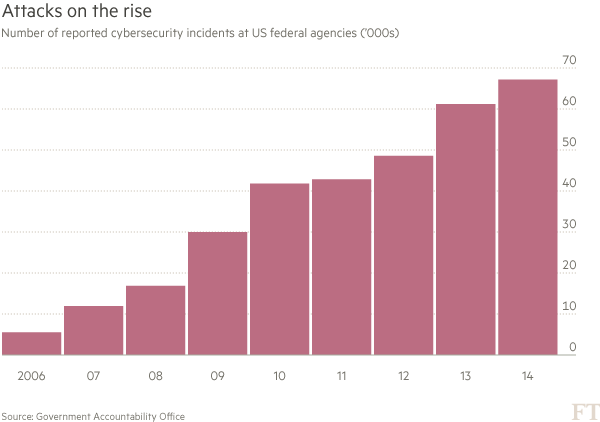

According to an analysis by the Financial Times of dozens of reports by agency inspectors general, “the Government Accountability Office and the Office of Management and Budget reveals that for years more than half of the 24 agencies required to report their cyber defences failed to take the most basic security steps”.

There is a lot of “catch up” spending from other US government agencies given the scope of the most recent attacks. What about other governments? I suspect they have underspent just as much as their US counterparts. The market opportunity for cybersecurity is well and truly vast!

To see Proofpoint's forecasts and financial summary, click here.