Moorebank will drive growth for Qube

We have 7 per cent of our “growth first” model in Qube Holdings (QUB). We started the model portfolio last week and you can see all the details here.

With the contract recently announced for the Moorebank intermodal project, we believe Qube provides exposure to a quality logistics operator and one of the best infrastructure assets in Australia.

The high level of global demand for Australian infrastructure assets can been seen via the recent combined cash and scrip offer for Asciano (AIO) by Canadian based Brookfield Infrastructure Partners. This follows Japan Post's $6.5 billion bid for Toll earlier this year.

Although the final confirmation of the Moorebank project in early June is one of the most significant moment in Qube's history, the share price has been weak due to the company announcing an FY16 earnings downgrade at the same time.

Given the long-term earnings security Moorebank provides, we view Qube as an excellent stock to BUY on weakness (e.g. when market is worried about Greece).

Moorebank – Deal structure

Qube announced that conditional contracts have been signed between the federal government owned Moorebank Intermodal Company (MIC) and Sydney Intermodal Terminal Alliance (SIMTA), a consortium comprising Qube (67 per cent) and Aurizon (33 per cent).

The two groups own land next to each other in Moorebank (South Western Sydney). The “whole of precinct” approach to develop Australia's largest intermodal terminal was decided as the most appropriate solution, and SIMTA has been granted a 99-year lease over the combined 243 hectares of land.

Qube will operate an import-export terminal (IMEX) and interstate freight terminal with capacity for 1.5 million 20-foot equivalent units (TEU) per annum when fully developed. A key factor in the whole of precinct approach is the ability to share warehousing and distribution facilities, with 100 per cent greater warehousing capacity than two separately managed sites.

The precinct will include up to 850,000sqm of warehousing fully integrated with port shuttle and interstate terminals.

Qube has development, property and asset management rights over the precinct for the 99-year term of the lease.

Why it makes sense:

In Summary:

- Removes congestion around Port Botany by transferring volumes from road to rail;

- Improves productivity by having more capabilities on site and reducing wasted steps in the supply chain;

- Reduced costs for customers;

- Reduced pollution with less trucks on the road;

- Pricing power for Qube in offering a more efficient solution than currently available.

Import and export containers through Port Botany are expected to increase from 1.7 million in FY17 to approximately 2.7 million in FY27. This 1 million increase could fill the IMEX without even transferring container volumes that currently go through other facilities.

Ideal location

The Qube management team (formerly Patrick) had identified Moorebank as a priority location for a freight terminal since 2004. Its direct rail link to Port Botany and freight markets around Australia, and its proximity to major motorways, make it ideal for an intermodal facility.

The site is adjacent to the Southern Sydney Freight Line (SSFL) where it currently operates container rail volumes.

Government funding

Rail to the terminal will be open-access for transport operators to increase competition in the freight market, and it will support federal and NSW targets to get more freight on rail, with a small cost to the government.

The Commonwealth is expected to invest around $370m in the development, including funding the rail connection between the terminal and the SSFL and land preparation works. The Commonwealth spending is lower than originally anticipated and will attract a low-risk return.

Capex requirements: (including partners)

SIMTA has agreed to build and operate the terminals and has development rights for associated warehousing at a total cost of approximately $1.5 billion over 10 years. This includes 850,000 sqm of integrated warehousing where a proportion will be funded by partners.

The direct capex for Qube (excluding warehousing) will be approximately $400-450m over the first five years.

Ramp-up in volumes

The import-export (IMEX) freight terminal will have final capacity of 1.05 million containers per year, and the interstate terminal will have capacity for 500,000 containers a year.

Stage 1 will see 250,000 containers per year through the IMEX facility, and will be completed by the end of 2017. The first stage of the interstate terminal will also have around 250,000 containers per year initial capacity but is not due for completion until the second half of 2019.

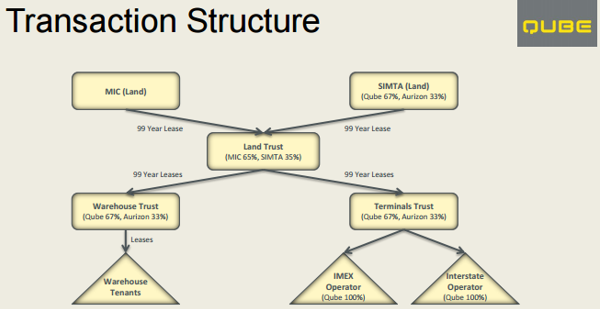

Land Trust

As displayed in the diagram above, the land will be combined under a land trust and leased to SIMTA for 99 years. SIMTA owns 35 per cent of this land trust and the federal government (MIC) owns 65 per cent. This is due to roughly two-thirds of the land being government owned.

Warehouse Trust

Qube (SIMTA) has the rights to develop warehousing on the Moorebank precinct. Management has said they are still considering what proportion they will develop themselves. It would make sense for them to sell at least part of the development rights to fund some of the capital requirements for the terminals. If they develop themselves then they would then be likely to lease it out.

Target tenants include importers and national distributors, who would benefit from the logistics efficiencies of the site. Similarly freight forwarders, express freight and high value exporters are also likely to be benefit.

In fine print on page 12 of the presentation announced to the ASX is a note that Qube has rights and obligations to acquire Aurizon's property development rights for each individual warehouse lot for the balance of the lease.

Ground rent

The Warehouse trust will pay ground rent to the Land Trust from each individual warehouse lease commencement. The terminals trust will pay ground rent to the land trust from year six on IMEX terminal land and year eight on Interstate Terminal Land.

Qube revenue streams

Terminal – 100 per cent of the IMEX and Interstate terminal operations, but only 67 per cent of the ownership (Aurizon 33 per cent).

Property Management – Development manager, property manager and asset manager.

MIC Funded Works – Construction manager

Property – Ground rent (23 per cent)

Warehousing (options include) – Develop and lease, develop and sell, Partner/JV with third parties to develop and lease/sell, sell development rights.

Logistics – Port shuttle rail services, regional rail services, 3PL warehousing and other container services.

The pricing power and competitive advantage is strong, considering the only area it faces competition is the port and regional rail services (“open access”).

The other area of competition that does place a cap on pricing is the cost and efficiency of road rather than rail transport. There is also competition for road-based container transport outside of Moorebank but that is not really a service Qube focuses on.

It needs to be highlighted that the only “open access” part of the facility is the rail containers to and from Moorebank, where Qube still receive an access fee.

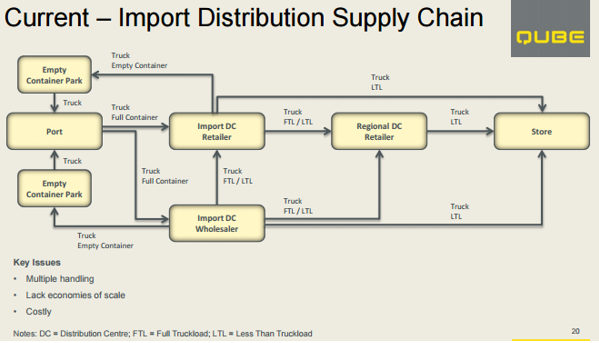

More Efficient Supply Chain

It can be seen above that the current supply chain includes multiple handling and wasted steps such as the movement of empty containers.

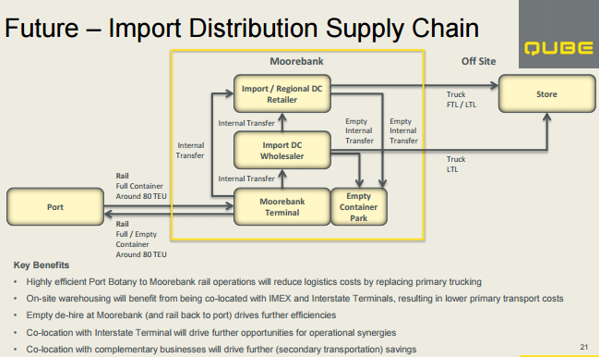

The plan for Moorebank with everything on site will improve productivity and cut costs out of the chain. There will also be large-scale benefits given the size of the site (largest in Australia).

Down the track there will also be an increased level of automation that will further improve productivity and save costs, particularly the transfer of containers from the rail terminal to customer warehouses.

There are six other main intermodal terminals in Sydney but none of them go close to having the same capabilities as Moorebank due to a lack of size, design initiatives and in some cases inferior locations.

The current cost of the import container supply chain to retail store is about $1,500 per container. Qube management believe they can reduce this by 20-25 per cent, and at the same time capture about one-third of this revenue themselves (i.e. $400 per container).

Management

The core group of senior management at QUBE worked previously at Chris Corrigan-era Patrick Corporation. Moreover, Chris Corrigan is chairman of QUBE. However, it should be noted that Corrigan is playing a minor role in comparison to the impact he had as managing director of Patrick Stevedores in the 1990s, when the company dramatically improved productivity in Australian ports through a controversial overhaul of workplace practices.

The hostile takeover of Patrick by Toll in 2006 was a bitter and lengthy process that prevented several key Patrick executives from completing their strategic plans: Those executives are now having a second chance at QUBE.

Maurice James is chief executive, but the strength is the depth through all divisions.

Risks

The development of Moorebank is largely de-risked, but there are still a few approval requirements that need to be ticked off.

Further Moorebank risks include a blow-out to capex costs, poor rail reliability, and inefficient container stevedoring at Port Botany.

For Moorebank and general Qube logistics operations, earnings are certainly sensitive to general economic conditions. However the company now has enough diversification that it can get through weak markets without too much trouble.

FY16 outlook

At the same time as the Moorebank announcement management also downgraded earnings expected due to weak operating conditions, particularly with iron ore.

Management's expectation is that trading and economic conditions are not expected to improve in FY16, and as such they are expecting “Port and Bulk” earnings to be lower in FY16.

Despite downgraded earnings expectations for FY16 and FY17, in our view the Moorebank details outweigh the negative earnings revision.

Management will continue to pursue strategic growth across core markets and will continue to invest and build scale and efficiencies, and continue the trend of developing new innovative logistics solutions.

Earnings / valuation

Although there is still uncertainty about some of the required details for Moorebank, there was enough information to increase our base case valuation.

There was no real negative surprises and the project looks to be managed very well.

We are assuming Qube capture one-third of the more efficient $1,200 supply chain (currently $1,500). Assuming 15 per cent EBITDA margins and then a gradual ramp up to full volume capacity by 2030.

The above market PE (20 ) for FY15-FY17 needs to be adjusted for the non-operating Moorebank asset which other than a rental yield won't start contributing to earnings until FY18.

We have a combined valuation of $3.05, which includes slight downgrades for FY16 and FY17 forecasts.

The 25 per cent discount to valuation may not look that appealing, but it is the type of stock that is likely to have multiple valuation upgrades as management continue to successfully execute their strategy.

We have upgraded our recommendation from HOLD to BUY.

Click here to view Qube's financial statements.