Consolidating AMA's future

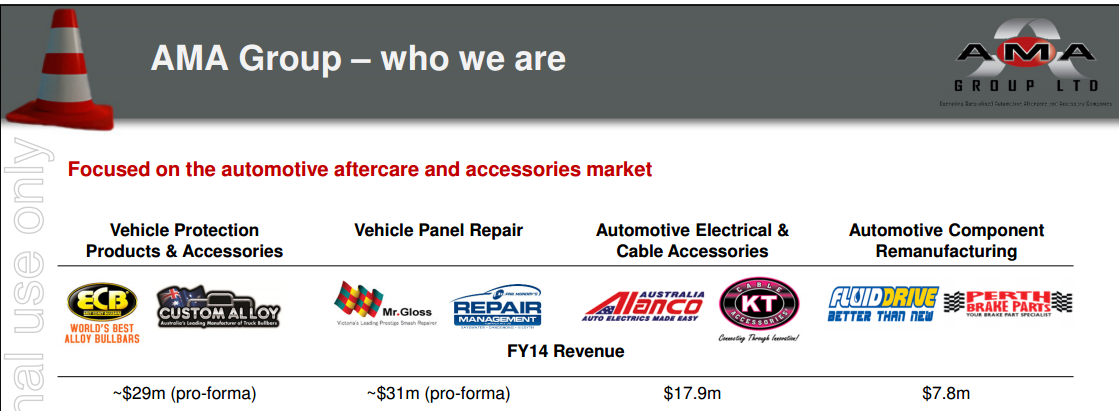

AMA Group is focused on leveraging its experience in the automotive aftercare and accessories market. Recent acquisitions in its two key divisions of vehicle protection products (bull bars) and panel repairs have been successfully integrated. Chief executive, Ray Malone, is working hard to benefit from a “tsunami of change” in the panel repair industry.

After the company nearly collapsed due to a stretched balance sheet in 2009, it appears that Malone has placed the company on a more secure path to growth. Although he aims to double earnings over the next three to four years, he won't let too much risk compromise his goals. Specifically, he hates shareholder dilution with a passion, and won't rush through acquisitions until he is sure they can be seamlessly integrated. His interests are also aligned with shareholders due to his 25% ownership of AMA.

Malone also has a succession plan to step down in three years' time and hand over the role to current chief operating officer Ray Smith Roberts. Malone has had a long history in the auto repair industry, and since taking over as chief in 2009 he has lifted the share price by a multiple of seven times. Our earnings forecasts don't assume he doubles earnings, and that is partly due to the fact that some of the growth will come from acquisitions.

There is no shortage of targets in the fragmented panel repair industry and there are also some opportunities in the vehicle protection market. Although the stock is not expensive at around 30 cents, our “buy” recommendation is based around the opportunity to benefit from the consolidating panel repairs industry.

The “tsunami of change”

Malone's opinion is that the panel repairs market will reduce from 6000 operators down to 500 with AMA Group to be one of five or six main players. This shift is being driven by the large amount of small sub-scale providers and the insurer's strategic shift to deal with fewer repair shops, as well as operate some of their own. Malone estimates that 40% of the consolidation will be from acquisitions and 60% will be companies exiting the industry.

The motivation for the insurers to deal with a smaller amount of operators is to cut costs, and also only deal with companies they have confidence in. It effectively means the “colourful” or “dodgy” side of the industry is being stamped out. AMA's workshops are certified by all the major insurers except Suncorp Group.

There is the opportunity for insurers to save about 25% of costs whilst doing about 80% of the work. Part of the way this is achieved is a faster cost model, which may mean panel repair shops have to be flexible and be willing to take a loss on some work whilst benefiting on other jobs. The end result is a more efficient process, and if AMA can work with the insurers then it improves the opportunity to grow together.

In panel repairs, AMA is targeting revenues of $180 to 200 million versus current levels of around $30 million over the long term. Repair Management Australia (RMA) was recently acquired and it is crucial to the model of working with the insurers. It mainly deals with in-scope work – that is, jobs under four hours.

The integration has been successful and Malone has high confidence in his ability to achieve synergies and make all his acquisitions instantly earnings accretive.

Another key to AMA's strategy is spreading its risks across various parts of the automotive industry, and benefiting from scale and synergies across the group. As well as the boost in “in-scope” capabilities, AMA is well regarded in the prestige market.

Other divisions

Across the business the shutting down of domestic auto manufacturing is expected to have less than a 1% net impact on earnings. The reason for this is a majority of AMA's earnings exposure is with the after-care market rather than the initial manufacturing.

The vehicle protection division is currently at roughly the same revenue as the panel division due to the acquisition of Custom Alloy which operates primarily out of Queensland. Revenue from this business is generated mainly after market from automobiles up to light trucks, with the remaining 10% coming from sales to original equipment manufacturers (OEM). Custom alloy operates in the four to 14 tonne light truck range. All manufacturing and fabrication is done locally in Queensland, enabling a much faster turnaround when compared with competitors.

Other operations in Queensland include KT Cables, which is a wholesaler with over 2000 products, and a licensing operating for LED trailer products.

In Victoria there is Fluid Drive which operates in transmission manufacturing.

In Western Australia there is Allanco which is a small auto-electrician hardware business. Perth brakes has had a tough time due to the slow-down in mining work, but it remains profitable and a core part of the business.

Summary

There is no change to our “buy” recommendation, prior earnings forecasts or $0.36 valuation. However, it is worth noting that if Malone gets anywhere near his targets, our valuation will be upgraded multiple times over the next few years.

To see AMA Group's forecasts and financial summary, click here.