CAJ surfs a regulation change

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Start your free 15 day trial now' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

The large amount of regulatory uncertainty for the radiology sector played a major part in a weak half-year result for CAJ. This uncertainty began in April 2015, when the government established a Medicare Benefits Schedule (MBS) Review Taskforce, with the purpose of reviewing the 5,500 services listed on the MBS Schedule across all medical disciplines.

For radiology, GPs have been warned about referrals for unnecessary scans, particularly some high quality MRI and CT scans, with government doubts around the cost effectiveness of utilising the highest quality and most expensive scans. Although the results of the Medicare review are not expected until late 2016, GPs have acted in advance with immediate declines in referrals. GPs are cautious as that they want to avoid government scrutiny, sometimes at the expense of patient outcomes. Over time this system decline is expected to normalise, but uncertainty is likely remain for much of 2016.

Historically, diagnostic imaging (radiology) has grown volumes at four to six per cent per year. For the five years to June 2014, diagnostic imaging achieved a compound annual growth rate of 7.8 per cent. For Capitol Health (CAJ) it is the MRI and CT scans that are most profitable and some stability and growth in these high value scans is required before CAJ will return to growth.

Separately, in mid-December 2015 the government announced changes to bulk bill rebates for radiology services to commence in July 2016. This still needs to pass through the Senate, and the full details and path for regulatory process are unclear. At worst, the bulk-billing reimbursement rate is expected to be cut from 95 per cent to 85 per cent. Bulk billing incentives for concession card holders and children will remain unchanged.

Although not confirmed, MRIs are expected to have a relatively smaller 5 per cent cut to the bulk billing incentive. Twenty per cent of CAJ revenues are from MRIs (and a higher percentage of profit), and about 80 per cent is bulk-billed, and will therefore be exposed to the five per cent price cut. Of the non-MRI revenue (80 per cent), about half is non-concession or children – this means it is exposed to the 10 per cent price cut. With the changes due to go through from July 1, the CAJ revenue impact for FY17 is expected to be 5 to 7 per cent. Given the fixed cost nature of the business, this revenue cut will have a much larger impact on profit. But at the current share price, the worst case of this outcome is most likely already priced in.

Assuming this pricing cut does go ahead, there is uncertainty around how the industry will react. The rational response would be a co-payment, where the reduction in government revenue for service providers is effectively passed onto the customer. CAJ and its major competitors in I-Med, Sonic, Primary, and Integral have all publicly stated that they would charge a co-payment but whether they actually do will remain an uncertainty until July 1.

A major risk for CAJ is a price war, with the objective of acquiring smaller scale companies or forcing them out of the industry. If this pricing war scenario did play out, it would likely be a short term (six months) issue rather than long-term structural issue.

The combined regulatory uncertainty is not likely to go away anytime soon, but despite this there has been anecdotal evidence of referral volumes picking up in Victoria for January.

Half year result

The Capitol Health (CAJ) half-year result was below expectations at the profit line due to a larger than expected volume decline in the most profitable scans (MRI and CT). Earnings before interest, tax, depreciation and amortisation (EBITDA) of $10.9 million was below expectations of approximately $12m.

Revenue was in line with expectations at $77.4m (up 57 per cent on H1FY15), with a majority of the increase due to four acquisitions.

Underlying Net Profit Before Tax (NPBT) of $5.2m was down from $7.3m in H1FY15, reflecting higher interest and depreciation costs flowing from acquisitions. There were significant one-off acquisition and restructuring costs (i.e. stamp duty, transaction costs) of $1.7m.

The interim dividend was suspended pending capital management activities. The main positives from the result included details of a very supportive banking relationship, and no write-down of intangible assets. Further management expects the previous trend of higher second half revenue to continue for this financial year.

Fixed cost leverage

A key take-out from this result is the very high level of fixed-costs, limiting management's ability to adjust costs to match revenue declines. This fixed cost leverage obviously works both ways, and means even a very small rebound in volumes will have a large impact on profitability.

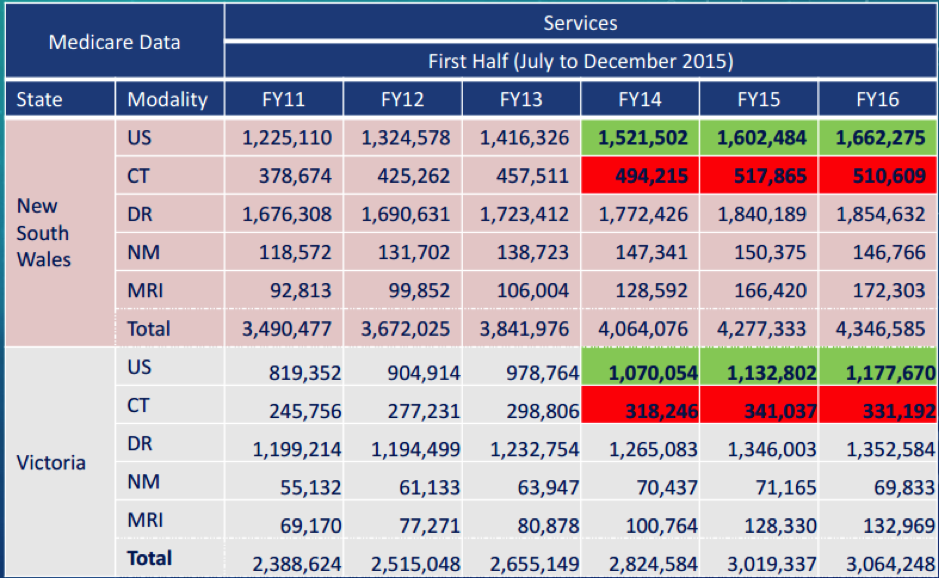

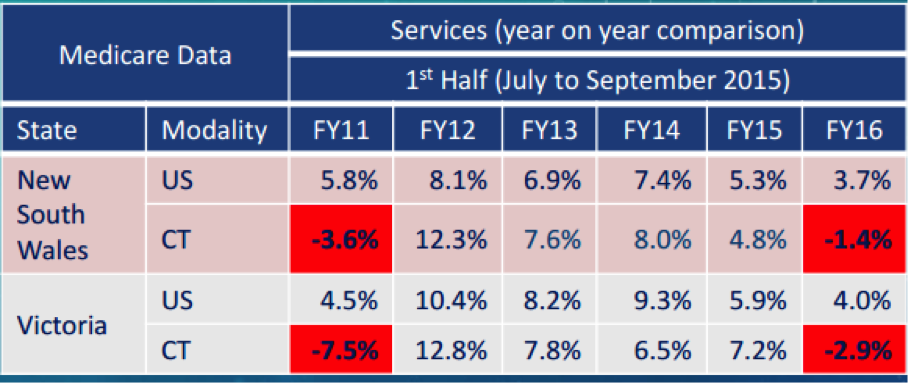

About 64 per cent of Capitol's revenue is currently Victorian based, and 36 per cent is from NSW. The Medicare stats below display negative growth for CT and lower growth in MRI in both New South Wales and Victoria. In 2010, Medicare also pressured GPs on unnecessary CT scans, with the effect of lower volumes seen in FY11.

Balance sheet

A positive from the result was that the company's principle lender, NAB, has approved a revised banking facility to the group for a total of $140m with normal key covenants including net debt to EBITDA of no more than 4x through to December 2016, dropping to 3.5x by the end of June 2017.

The market most likely misread the confusing details around a potential bond issue as meaning it was looking to materially increase its net debt of $77.1m. It was stated that the company has received initial approval for a senior unsecured bond up to $50m, which it may or may not utilise.

We understand the funding cost on the standard debt is 5.5 per cent and the bond will be 8 per cent, if utilised. The purpose of the bond issue would be to reduce existing debt, as the bond debt is not included in the covenant ratio calculations. Current net debt for covenant purposes could be reduced from $77.1m to $27.1m after issuing the bond. This means the company is well within covenant limits and is very little chance of been forced into a dilutive capital raising.

Executive option issue

After an external review on executive remuneration packages it has been determined that managing director John Conidi will be issued 15 million options, with the price based on a 50 per cent premium to the 5 day VWAP ending on the February 12. After the significant share price decline, it is extraordinary to think that the MD will be able to increase his already significant 6.5 per cent position in CAJ.

Enlitic partnership

CAJ has completed the acquisition of $US10m of shares in MRI 'smart technology' provider Enlitic. Although it is difficult to quantify the potential impact and when it will have an effect, this investment provides an opportunity for CAJ to improve accuracy and speed of scans, reducing costs and enabling the potential for greater market share.

An initial $5m was paid on February 10, with two further payments of $2.5m on April 15 2016, and August 15 2016.

The downside scenarios

Although there is significant uncertainty likely to remain in place throughout 2016, this needs to be weighed up against what is already priced in. At 14c, or a $73m market cap, CAJ is trading on a FY17 PE of 7.8, and EV/EBITDA of 6.5. (FY17 EPS of 1.7 cents, and EBITDA of $23m).

1. The outcome of the Medicare review is not likely to take effect until the start of FY18, but the recent decline in GP referrals has likely already over-compensated for any Medicare changes.

2. Despite details not been confirmed, the cut to bulk-billing incentives from July 1 has been priced into our forecast with a 7 per cent revenue impact for FY17. The potential downside risk here is to what extend there is a pricing war if the changes go ahead as currently expected.

3. Assuming the company has access to the $50m bond issue, we are comfortable that they will remain well within debt covenants and therefore will not be forced into a dilutive equity raising.

4. In terms of the radiology industry, it is worth considering that the Medicare review scenario is not unprecedented. A similar review saw sharp declines in GP referrals in FY11, followed up by a sharp increase in FY12. More generally, the ageing population and savings to the overall health system from early diagnosis is likely to see diagnostic imaging volumes continue to grow over the medium term.

5. Management had been very successful in consolidating the Victorian non-hospital radiology clinics, and made early progress with NSW. With the current uncertainty to growth expectations, and lower earnings multiples it will be much more difficult for CAJ to continue with its consolidation strategy.

Earnings revisions

Despite the regulatory uncertainty, we believe the worst case has been priced into the CAJ share price, and also our earnings forecasts. The one disclaimer with that assumption is the event of a major industry pricing war where the larger players aggressively drive the smaller companies out of the industry.

Capitol Health is also better placed than many smaller competitors to win market share, especially as it focuses on increasing its competitive edge through cost saving initiatives such as Enlitic.

Our forecasts assume no recovery through FY16-FY18, with EBITDA in the range of $23m-$25m and NPAT in the range of $9-$9.5m.

This places the company on a PE of 7.8 times FY17, and therefore leaves significant room for upside if regulatory uncertainty is resolved and volumes stabilise and/or increase.

Our valuation is reduced to $0.22c and we maintain our hold recommendation.

To view Capitol Health's forecasts and financial summary, click here.