Time to sell Melbourne housing?

MacroBusiness

Melbourne has long been considered one of Australia's best property bets – it lured my wife and I, among many other buyers – but the city's increasingly costly housing market is now showing signs of weakness that are hard to ignore.

In mid-2006, my wife and I bought our first home in Melbourne – a brick house in the city's inner east. At the time, we considered the Melbourne housing market to be expensive, but not excessively so. We'd been married for a year and planned to start a family, and therefore wanted to lay down some roots in an area near where we had both grown up.

We purchased the house via private sale at just below the suburb's median house price. Below is the five year REIV price chart pertaining to the suburb. Note that I have blocked out the suburb's name for privacy reasons.

As you can see, we were fortuitous in our timing – our suburb's median house price has nearly doubled in the five years since we bought. And despite earning significantly more income than in 2006, valuations have become so stretched that we would now struggle to purchase the same home.

Now I realise that my experience in one suburb is not indicative of the overall Melbourne housing market. However, the macro data also suggests that Melbourne property valuations have become stretched, and that the market is now in a precarious position.

Consider the following indicators.

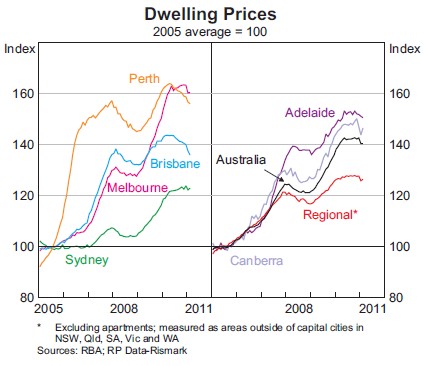

Firstly, Melbourne's house price performance has exceeded other capital cities. As shown by the below RBA chart, Melbourne's home prices have risen higher than the other capitals since 2005.

Secondly, according to the latest Demographia Housing Affordability Survey, Melbourne's Median Multiple (median house price divided by median household income) is the third highest in the nation, just behind Sydney and Coffs Harbour (see below chart).

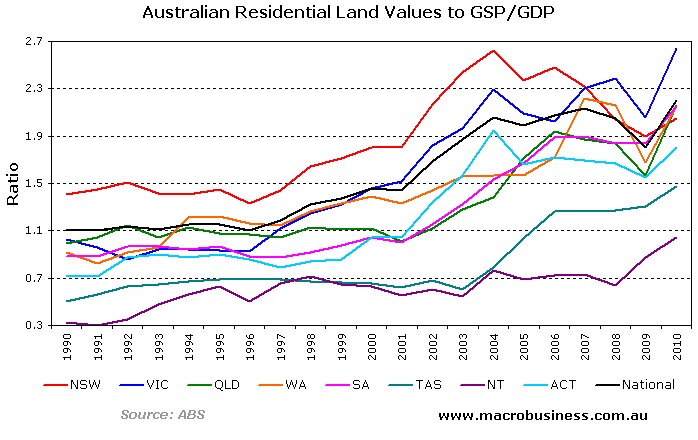

Thirdly, the ratio of Victoria's residential land values to Gross State Product (GSP) is the highest in the nation (2.6 times), indicating severe overvaluation (see below chart).

First, consider RP Data's latest release. It shows that investors aren't getting anywhere near as much bang for their buck in Melbourne, with rental yields in the so-called property hot spot well beneath the Australian Capitals average. The fact that you can reap higher rental yields in every other capital city won't go unnoticed by many investors.

APM's latest release also shows Melbourne rental yields not just lagging other capital cities – which alone would be enough to consider investing in new growth areas, Brisbane, Canberra and Hobart – but it was the only city measured to see a deterioration in gross rental yields for houses or units.

You can see here that the growth rates for both stepped backwards. It's one thing for a city to have lower rental yield growth rates – there are other strategic factors to take into account when selecting property – but it's quite another for it to be the only city where growth rates are declining.

According to SQM Research's latest newsletter, Melbourne has recorded the equal largest increase in stock coming onto market, registering a whopping 60.9 per cent increase from this time last year. Melbourne's increase in stock is well above the national average increase of 47.6 per cent.

It is also fair to say that Victoria, read Melbourne, built its way through the GFC. Some of that was school halls. But most of it was dwellings, adding to supply.

Melbourne's housing market certainly appears to be in a precarious position, due to a combination of stretched valuations, very low rental returns, and increasing numbers of homes for sale.

Of course, there is the mitigating factor of strong population growth over the last decade

But we know immigration is slowing significantly nationally and supply is already overwhelming it in Melbourne anyway.

While this certainly does not mean that a housing crash is on the way, there is little potential for solid house price growth going forward.

Accordingly, prospective first-time buyers should think twice before gearing-up to buy into the Melbourne housing market, particularly given the relatively cheap rents on offer. Likewise, investors might wish to consider taking profits, since superior investment opportunities are available elsewhere.

Disclosure: I own my own Melbourne home, have a small mortgage (LVR~25 per cent), and am not planning to sell. The above article is not financial advice. Please undertake your own research and/or obtain independent expert advice before making an investment decision, including buying/selling property.

This article first appeared on the MacroBusiness website. Republished with permission.

{kind=link}

{kind=link}

{kind=link}

{kind=link}