The technology dividend is the one that matters in 2015

Summary: The David Murray-chaired FSI report says that the Australian banking system avoided the GFC because we encountered a funding crisis, not an asset value crisis. In order to keep the banking system strong, banks could allocate more equity to home lending, but this would lower profit. The other option is for banks to further use technology to drive efficiency. Medibank Private's future profits will also depend on the current CEO's push into technology. |

Key take out: Banks, health insurers, retailers, manufacturers and almost every other type of business must use technology to transform their companies for growth. |

Key beneficiaries: General Investors. Category: Bank stocks. |

Let me explain two dimensions of a remarkable story which will shape our banking system, the newly-listed Medibank Private and many other companies.

First, to the banks. We will strip this week's David Murray-chaired Financial System Inquiry report down to its essence – which is a sobering message.

When Murray was chief executive of the Commonwealth Bank for 13 years between 1992 and 2005 he ran a very different ship to the current CEO Ian Narev.

There were different weightings on the various types of loans which meant that much more equity was required to fund housing than is currently the case, and it was more attractive to lend to small business.

Without going into the history of how it happened, the recent money making system of Australian banks has been to lend on home mortgages and take advantage of the low required equity backing. To put it crudely they are geared to the eyeballs on home lending and business lending has suffered.

Murray wants to change that and make the banks put more equity behind their home loans and be encouraged to lend more to business – we go back closer to the Murray era of banking.

Be very clear this is a major change but nothing will happen unless both the ALP and the Government agree on what should happen next.

Murray's argument is very powerful. He says that the Australian banking system avoided the global financial crisis because, unlike many other countries, our asset prices did not collapse. What we encountered in the global financial crisis was a funding crisis not an asset value crisis. That funding crisis was relatively easy to fix via government guarantees.

But next time around we might face an asset crisis, just as happened in the US and Europe.

Murray is not predicting a dramatic fall in dwelling prices (nor am I) but if we want a strong banking system we must be able to stand a big fall in dwelling prices.

Given that the current level of dwelling prices is boosted by massive Chinese investment there is an embedded degree of instability that our country has not seen before.

Of course the converse argument is that we have seen nothing yet in terms of Chinese investment.

There will be a pullback in the next few months but the Chinese are planning major investments into Australia – particularly into Melbourne and Sydney. Murray wants the high dwelling gearing of our banks to be reversed over time, but what the global institutions really want is for our banks to face up to the situation and lower leverage over a shorter period.

The problem that our banks and their CEOs face is that if they put more equity behind home lending, it will lower their profit and dividends per share.

And if they issue a lot more equity it will suck money out of the market. Australian banks have locked themselves into a high dividend policy based on the returns created by over gearing – certainly that is Murray's view. (To read more on the dividend patterns in today's market see today's piece by Scott Francis: Are we paying too much for dividends?)

So what is required to fix it? The bank PR machines warn that if Murray's recommendations are accepted it will mean higher interest rates for housing loans and even lower returns for depositors. My guess is that if interest rates fall next year banks will lift their margins and retain the extra profits to lift equity. And as equity rises so they will be able to borrow overseas at better rates further lifting margins. This will limit extra direct equity via issues.

In addition there is also another way: Banks have been one of the main beneficiaries of technology and this has enabled them to become more and more efficient and a big slice of the rewards of that efficiency has gone to shareholders. But there is a lot more to do and the real impact of the Murray report is likely to be a considerable increase in the use of technology by banks. And they are also going to need to fix up their wealth businesses which have been poorly managed and forced many Australian to go into self-managed funds.

So listen carefully to what bank CEOs say in the next reporting season when they have had time to digest the Murray report. Those banks that say they are going to fix the problem and make themselves far more innovative in the process will be the shares that win.

But don't believe the market conclusion that the banks really don't need to do anything. And also don't miss the footnote I have at the bottom of this commentary.*

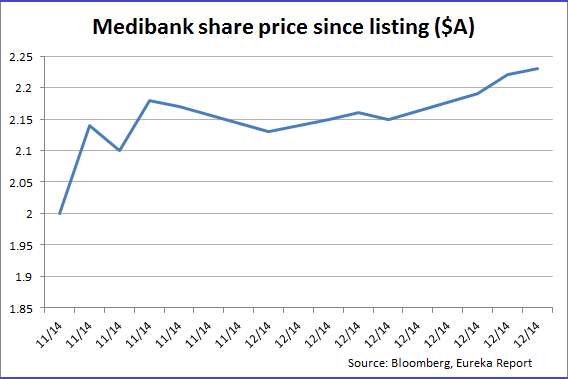

The second dimension of our story about technology is typical of what a great many enterprises must do. Medibank Private, under government ownership, could see that it had achieved most of what it could do by normal efficiency methods. What it needed to do was to have a much greater knowledge of its customer base and here we are talking about the people who make big insurance claims.

CEO George Savvides installed massive computer systems that now enable Medibank to know which hospitals are not performing well and exactly where they are slipping up. And Medibank also knows exactly which customers are making the most claims. Working with the individual customers will not always change the level of claims. But working on a case by case basis will reveal situations where greater use of primary or preventative care can save Medibank a lot of money.

About 2% of the Medibank customer base is responsible for about a third of the claims so it is not an impossible task because relatively few people are involved.

The level of Medibank profits in future years will depend to a large extent on the success of this Savvides push into technology. As you can see it is not that different to the banking story but there is no Murray whip.

As I explained to Eureka Report readers at the time of the prospectus (see Medibank IPO first impressions: Low yielding and not cheap) the Medibank yield of 4.2% based on a $2 share price was misleading. To obtain that yield Medibank had to pay out 89% of its expected profits in the year ended June 30 2015. That will happen but 2015-16 is a different story.

The company believes it can only pay 75% of its profit on a sustainable basis and if profits do not rise sharply in 2015-2016 dividends will need to be reduced. While this was made clear in the prospectus you had to read the small print. That is why Medibank shares have not performed as well as many thought would happen. But if the technology transforms the company it will enter into a new growth path. And that Medibank/banking type story must extend to retailing, manufacturing and almost every other type of business.

*Footnote: The fall in the oil price is going to cause enormous ramifications in the global finance market.

There will be sizeable losses in derivatives and in the funding of oil ventures. Global banks are going to lose a lot of money. I think – but I am not sure – that Australian LNG projects will be able to pay their debts but there is no certainty because they borrowed too much.

It is a space to keep watching. And it underlines how surprising events can change the game which is why you need a strong banking system.