The great Australian lie

Readers will already be aware that Australia is now gripped by an income recession. What's interesting about this is the fact that we're actually not in such a recession at all.

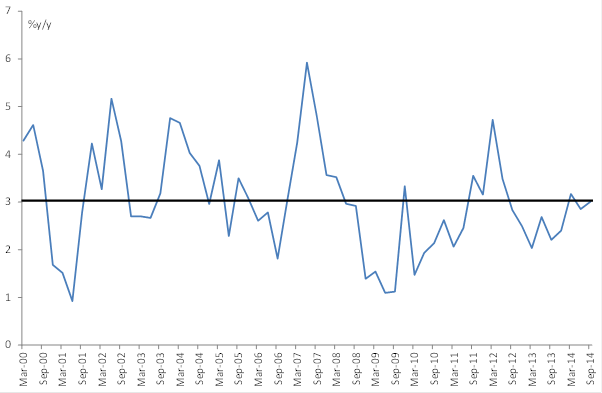

The chart below shows Australia's national income growth over the last 14 years and as you can see, it is very much around trend. Indeed, the idea that we're in some sort of income recession is, quite simply, a lie.

Don't forget that the recession call has gone out, in one form or another, in each and every year since the global financial crisis. In each case, those claims have been fraudulent.

Chart 1: National income growth is at trend

The reason is simple. The measures widely used to point to recession don't actually measure income. The one shown in the chart above does though, as it's the sum of what business and households etc actually earn. That is, what their income is, in real terms.

More generally, the idea that the Australian economy is somehow suffering from below trend growth also looks to be quite fanciful. For a start, and in addition to solid income growth, GDP on an expenditure basis is also growing at a trend pace. That's two of the three measures that are used to calculate the headline number at trend. What's even better is that these trend growth rates lift to an above trend pace on the unadjusted figures, abstracting from the ABS' dubious data tampering -- more on that in a moment.

First though, it may surprise some readers to learn that the key area of disappointment in the Australian economy is actually on the production side -- nothing to do with the terms of trade or the end of the mining boom I might add. Specifically, two sectors present some very serious problems: construction and public administration. Together, these sectors have taken off about 0.3 percentage points from growth, a key reason why the production side of the economy looks so weak.

Yet how would anyone measure the output of public administrators with any accuracy? By the number of forms produced? It's absurd, as is the idea that the construction industry slumped over the last six months.

Other data produced by the ABS shows the construction industry surging, while private sector surveys show both confidence and conditions remain high in that sector. Making matters worse, the figures not manipulated by the ABS show much stronger construction activity. Correcting for those two sectors alone would bring Australian production back up to trend growth rates, just like we see in the income and expenditure space -- you can see the problem.

That brings me to the issue of the ABS' data adjustments. Remember that the ABS seasonally adjusts the data to strip out what it thinks are seasonal patterns. The problem of course, is that this procedure is highly subjective and can be heavily influenced by institutional bias. As we already know, the ABS has had some grave issues making adjustments to the labour force survey. Indeed the problems at the ABS are so serious, that the monthly labour force figures are simply unusable for serious policy analysis.

Unfortunately, it's not clear that the national accounts are much better. Consider that the year-on-year growth rates for the unadjusted GDP figures are much stronger than the adjusted figures. They should be the same, or at least very close. Yet on this basis, annual GDP rises to nearly 3 per cent from the adjusted 2.7 per cent year-on-year growth rate -- a marked difference.

It's the same looking at the quarterly growth rates. On adjusted figures, average GDP growth has been below trend these last four quarters while on the figures that haven't been tampered with, growth spikes to an above pace in both cases.

Seeing this, I'm not convinced that we can trust the ABS. As I discussed following the horrific errors made in the labour force survey, the ABS is going to want to fly under the radar for a while. This makes them more amenable in producing statistics that simply reflect the current consensus (of weakness). In my view, this is exactly what the latest GDP figures represent. There is little chance the economy was actually as weak as reported in that quarter.

I should mention that the apparently weak consumer spending figures are also quite fanciful. To see this, consider that the ABS figures show food consumption hasn't changed over the last year, it hasn't grown at all. This is despite the population lifting by an estimated 500,000 people (roughly 2 per cent). It's obviously an absurd proposition, yet this is the key reason why spending looks so soft.

The bottom line? Well, noting all the issues above, it is implausible that the Australian economy was as weak as the ABS made out. It is just one more example of how Australia's key economic institutions have failed the country -- are failing the country -- and I'd throw the RBA and Treasury into that as well. We appear to be a nation without hope or purpose, drivelling on year after year about recessions that we never even get close to. The reality is that underlying economic growth is probably still rising at an above trend pace.

Don't fret! The RBA will still likely cut rates. Panic merchants the lot of them. But don't be concerned about economic weakness -- it is simply untrue. Just as it has been for years.