Eureka's Week: Banks and real estate, Chinese money, deflation

Last night | Banks and real estate | Chinese money | Deflation! | Readings & viewings | Last week | Next week

Last night

Dow Jones, down 0.32%

S&P 500, down 0.51%

Nasdaq, down 0.62%

Aust. Dollar, US76c

Banks and real estate

I was part of a panel at an event called the “Developers and Dealers Forum” on Thursday night. In fact it was a networking dinner for property developers organised by Pitcher Partners and a non-bank lender named MaxCap Group. Designer stubble galore.

As with a lot of these things, it turned into a bit of whinge-fest, apart from when everyone was laughing at the comedian, Vince Sorrenti. (The only gag I can remember is that he had a fight in a car park with a disabled guy: “he was trying to park in one of our spots!”)

What were they all whinging about? Mainly planning ministers (plot ratios), banks and the meeja – for which I was the designated representative – for peddling the lie that there is an oversupply of apartments and that blessed negative gearing is a bad thing. The banks were in the firing line for no longer lending to developers.

Huh? The banks are out of property development? I didn't realise that.

Apparently pressure from APRA on the banks to keep themselves nice has resulted in bank funding for high-rise apartments completely drying up.

This is the reason MaxCap, which I had never heard of before this event, is doing so well. This partnership of four men led by Vincent Rusciano takes money from Australian Super and a few high net worth people and family offices, and lends it to property developers on terms that are very favourable (to its funders).

They told me about a recent deal where they lent to an apartment developer on 60 per cent loan to value ratio (that is, a 40 per cent buffer), secured on first mortgage, at 13 per cent interest. MaxCap gets 0.5 per cent, as well as a two per cent upfront fee, and Australian Super and the other suppliers of the cash, get 12.5 per cent yield.

That is a very sweet deal. So why aren't the banks getting in on this and lending at 13 per cent on a 60 per cent LVR? Because they're not allowed to.

I find this extremely interesting, and an important development for those who have invested in the banks, as opposed to apartments.

To skip to the conclusion, it means the banks might miss the bust. I don't know whether there is an apartment oversupply and therefore an impending collapse, but I do know that when the property sector has a party, a few people always do something stupid and it all gets messy.

It always happens. I watched it happen in the late 80s in Australia and in 2006-07 in the United States. Money intoxicates and injudicious behaviour sets in.

The best bank to invest in during the late 80s was NAB, because Don Argus and Nobby Clark had had an early bad experience and stood out of the madness. Westpac and ANZ, on the hand, were dancing on tables and wearing lampshades on their heads; as a result they nearly went broke in 1991-92 and their shareholders lost a lot of money.

Now it may be that this time around the banks find a way to dodge the regulator's strictures and climb aboard the Australian apartment Titanic before it hits the iceberg, but for the moment they are watching from a safe distance.

This is good news for investors. Certainly the banks are basically building societies these days, and are very, very exposed to real estate, but they might be pulling back at just the right time.

By the way, speaking of property developers and banks, also on Thursday a Parramatta lawyer named Hall Partners filed a statement of claim for a class action against CBA, on behalf of three developers, over the acquisition of BankWest in 2008.

According to my friend Ian Rogers at Banking Day, the statement of claim says, among other things: “"the final purchase price paid for Bankwest meant that CBA secured a net gain on acquisition of approximately $A983 million, with the result that it could write off and / or provision approximately $1,878 billion in impaired loans without any negative impact on its future profitability at the consolidated level."

I'm not sure what to make of it, but the claim is for a whopping sum and will be worth keeping an eye on.

Chinese money

Apart from the ritualized moaning about banks, plot ratios and the media, the developers in the room on Thursday night were pretty ebullient. The reason? The tsunami of Chinese cash that is waiting to invest in Australian real estate and make them rich. All conversations kept returning to this.

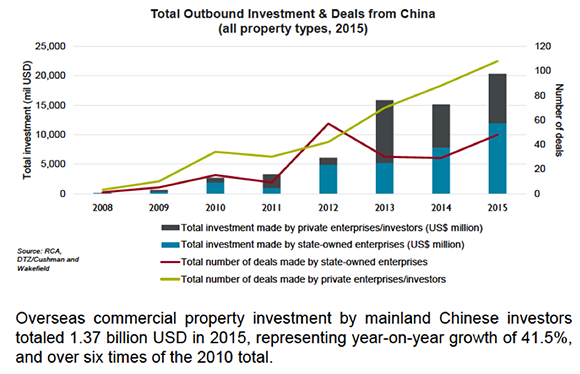

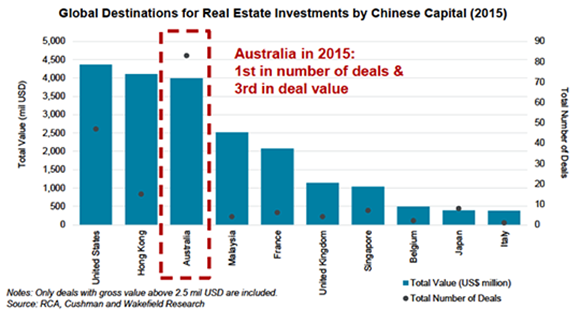

One of my fellow panel members, Daniel Grollo, showed me a presentation from a Chinese real estate services firm that summed up the basis of their optimism. Here are some of the charts in it, which are self-explanatory I think:

Daniel, who lives in New York City these days, told me: “We're entering a period where, for the first time in 600 years, Chinese investment will influence global culture. For the past 60 or so years, American money, and therefore American culture, has dominated the world, but from now it will be China.”

Someone else said: “The thing is that Chinese capital outflow will grow no matter what happens to the Chinese economy. If it goes well, they will invest offshore. If it goes pear-shaped at home, they will invest offshore.”

And another: “There are about four billion people in Asia, including China and India. Over the next 20 years that's going to grow by another billion or so. If even a fraction of one per cent of them decide to invest in Australia, that's hundreds of thousands of people trying to buy an apartment here.”

This is why they are so dismissive of talk of an oversupply of apartments: it's not Australia's faltering population growth that needs to mop it up, but the apparently endless supply of Chinese foreign investment. What's more the Government is stopping them from buying existing properties, only new ones.

And don't forget, they seem to be quite comfortable owning empty apartments – there are whole cities of them in China.

But look, I find it all a bit hard to assess. Direct foreign investment from China is clearly growing, as the charts above suggest, partly because of a natural desire by people there to diversify out of the over-heated Chinese property market, and partly to get ill-gotten gains out of the country. And clearly a lot of it is finding its way here, and will keep doing so.

It will therefore be a growing source of demand and is distorting a market that would otherwise be oversupplied, or in balance at best.

Will it provide a floor for Australian real estate prices, making it safe and profitable to invest?

Probably. I do think any investment portfolio should have some real estate in it – either direct, negatively geared, or through a REIT or perhaps one of the listed retirement village operations, or one of the geared property syndicates.

As for negative gearing, even if the Labor Party wins the election and brings in its policy of restricting negative gearing to new properties after July 1, 2017, don't forget that existing properties will be grandfathered. So anything you own before that date can still be negatively geared, old or new.

The time to buy is perhaps before the election, to beat the rush.

If Labor does actually win (against the odds, you'd have to say, even though Turnbull and Company are not travelling too well) there will no doubt be a buying spree and price spike as investors look to get set before July 1 next year.

And if the Coalition wins, negative gearing continues untouched, so no loss.

Deflation!

The bottom line for the minus 0.2 per cent CPI number for the March quarter, revealed by the ABS on Wednesday, is that it will exert downward pressure on the dollar. That's especially so after the US Fed's FOMC hinted at a June rate hike in its statement on Thursday.

The market odds on an RBA rate cut are about 50/50 and I don't have much to add to that. On balance I'm in the “no cut” camp, but only because Tuesday is also Budget day so they might wait till June.

A simultaneous cut in Australia and hike in the US in June would, you would think, see the Aussie head south at a rate of knots, although it's not as if such a result would be a surprise.

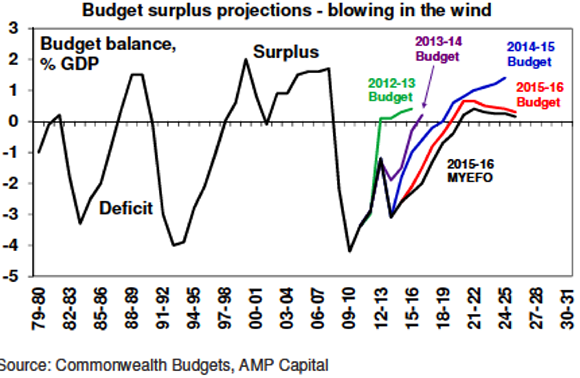

By the way, here is a nice chart from Shane Oliver of the changing budget surplus forecasts. It just keeps getting further out: will Tuesday's be a bit further again?

Readings & viewings

(A few things I've been reading watching this week)

There's a real paradox around next week's federal budget: it's the most important for years, but the build up is sanguine and low key.

Morrison's knock-back of the Kidman sale to a Chinese consortium redefines the national interest.

You're never more than 30 minutes away from the most exciting time to be an Australian.

Look, I know you're probably sick of reading about Donald Trump, but I can't get enough of him. This bloke is both fascinating and important. Here's a long transcribed interview with the five people who apparently know him the best.

And another interesting thing: Trump's outrage-fishing click baiting saves him 100's of millions of dollars for the main race.

Trump needs 43% of remaining delegates to win the nomination.

But 86% of campaign reporters say Clinton will be the next President.

Billionaires are funding lots of grandiosity. That's great.

Today's science lesson: could you outrun a fart?

Carl Icahn sells out of Apple.

Pre-fab bathrooms: a game-changer in construction.

Yahoo is for sale on Craigslist: $8 billion, slightly used.

The trouble with yield stocks. Tim Hannon, Chief Investment Officer at Newgate Capital, thinks ‘yield' stocks present significant risks in the current environment.

Really interesting essay here by Timothy Garton Ash: what happened to “the west”? Is it a ghost?

One of the things I like about Uber is that you can't tip – the price is the price. And Uber says here that it's not going to change that. Good.

Warren Buffett once told investors not to buy what he was selling. But they didn't listen.

Millennials are much more optimistic than baby boomers.

Interesting: Is humanity evolving into a hive? (because of modern connectivity). (A 4 minute video)

Bjorn Lomborg says the Paris climate accord will make almost no difference to global temperatures.

Who is Xi Jinping – a review of four books about him.

What China's food safety challenges mean for consumers, regulators, and the global economy.

Tara Brown's exclusive interview with … Tara Brown!

John Daley of Grattan Institute and Simon Cowan of CIS, on video discussing negative gearing.

Speaking of which here are the Tax Office's statistics on negative gearing.

Last Week

Shane Oliver, AMP

Shares pulled back a bit over the last week not helped by some disappointing earnings results from US tech stocks and surprise inaction by the Bank of Japan. Shares had become overbought so were due a bit of a pause or pull back.

This wrapped up a mostly positive month for shares with good gains in Europe, Australia and the US, but falls in Japanese and Chinese shares. Bond yields were mixed over the last week: up in the Eurozone, but down in the US and Australia. The oil price continued to recover as the $US fell, but the $A got hit by heightened RBA rate cut expectations following lower than expected March quarter inflation.

The big surprise over the last week was the decision by the Bank of Japan to not undertake more monetary easing despite soft economic data, inflation well below target, strength in the Yen and the earthquakes. Maybe the BoJ is waiting to assess a fiscal response from the Japanese Government and get the May 26-27 G7 summit to be held in Japan out of the way. Our assessment is that more BoJ easing is just a matter of time. Failure to do more soon though risks unwinding all the progress on inflation expectations seen under Abenomics, particularly with the Yen breaking to ever higher levels.

By contrast the Fed's April meeting delivered no surprises, with the Fed remaining gradual. A June rate hike is unlikely as US data probably won't have improved enough by then and markets may be nervous given the Brexit vote on June 23. The US money market's assessment of just a 26 per cent probability of a July hike appears a bit low though – I would think it's around 50 per cent. The key message from the Fed is that it will not do anything that upsets the outlook for global and US growth.

Australian inflation (or deflation) has set the RBA up for a rate cut on Tuesday, or at least it should have. While it would be wrong to conclude that Australia is on the brink of sustained deflation – as falls in petrol and fruit prices won't be repeated – the big surprise in the March quarter inflation data was that price weakness was broad based with underlying inflation running at its lowest annual rate on record. Both headline and underlying inflation are now running well below the RBA's 2-3 per cent inflation target. The risk is that thanks to a combination of deflationary pressures globally, soft demand domestically and very weak wages growth, inflation could remain well below target for an extended period. This is a risk the RBA cannot ignore and is best to address early before inflation expectations fall too far and under target inflation becomes entrenched. As a result, we think that the RBA should, and most likely will, cut the official cash rate by 0.25 per cent taking it to 1.75 per cent when it meets on Tuesday. But it's not just low inflation that justifies a rate cut. Other reasons include the risk of a soft spot in growth later in the year as housing slows, the still too strong $A and to offset upwards pressure on bank mortgage rates from higher bank funding costs. Will the banks pass a cut on in full? Probably not – “funding cost” arguments may see only 0.15 per cent or so of a 0.25 per cent cut passed on.

Major global economic events and implications

Here we go again - another weak start to the year for the US economy with March quarter GDP up just 0.5 per cent annualized with weakness in capex, inventories and trade. This was pretty much as expected and needs to be seen in perspective given that weak March quarter growth has been the norm over the last 20 or so years with average growth of 1 per cent annualised ahead of a rebound to average 3% growth in the June quarter. So far the evidence is mixed though as to whether growth in the current quarter is rebounding. In the past week we have seen weak readings for new home sales, durable goods orders and consumer confidence but solid readings for the services conditions PMI, pending home sales and the goods trade deficit and continued very low readings for jobless claims. At present though, it's all consistent with the Fed remaining very gradual.

US Q1 earnings have seen some mixed high profile results for tech stocks but have generally been better than expected. 58 per cent of S&P500 stocks have now reported with 77% beating on earnings and 57 per cent beating on sales.

Eurozone bank lending ticked up and economic sentiment rose both of which are consistent with ongoing modest growth. Japanese data was messy with strong labour market readings (although this may be due partly to a declining labour force) and a rebound in industrial production but a dip in inflation back into negative territory, a fall in core inflation to just 0.7% year on year, poor household spending and a fall in small business confidence. The impact from the Kumamoto earthquakes won't be helping and so further monetary easing is still needed.

Australian economic events and implications

Apart from the much lower than expected March quarter inflation data, export and import prices both fell more than expected pushing the terms of trade down yet again, producer price inflation remained low and credit growth remained moderate. In fact annual growth in credit to property investors is now less than that to owner occupiers.

Next Week

Craig James, CommSeec

Inflation takes centre stage

The Reserve Bank Board meeting and the handing down of the Federal Budget dominate proceedings in Australia over the week. The Reserve Bank's economic forecasts are released on Friday.

The week kicks off on Monday with the release of the State of the States report, the Melbourne Institute inflation gauge, the CoreLogic RP Data measure of home prices as well as the Performance of Manufacturing. Inflation is well contained; home prices have softened from highs; and manufacturing is currently in good shape.

On Tuesday data on consumer confidence is issued at 9.30am AEST. Meanwhile building approvals data is released by the Bureau of Statistics (ABS) at 11.30am AEST. Then the Reserve Bank hands down the rates decision at 2.30pm. And finally the Federal Budget is released to the public at 7.30pm.

After the surprise weakness of inflation, a rate cut will be discussed by Reserve Bank Board members. However with the economy in reasonable shape, the question is whether Board members believe there is a real need to cut rates and whether lower rates will actually be effective in lifting growth.

The Federal Budget is widely expected to focus on infrastructure spending while the Government may also unveil changes to address “bracket creep” and flag potential changes to the generosity of the tax treatment of superannuation.

On Wednesday the Federal Chamber of Automotive Industries releases industry data on new vehicle sales while the Performance of Services index is also expected.

On Thursday the ABS releases retail trade figures together with international trade (exports and imports). In addition the Housing Industry Association releases data on new home sales.

The retail trade data will attract most attention, especially as the real (inflation-adjusted) data for the December quarter is also issued. The key question is whether the early timing of Easter markedly affected analysis of the March figures. There are also signs that new construction has peaked and home sales data may shed more light on the speculation.

And on Friday, the Reserve Bank releases the quarterly Statement on Monetary Policy which includes the latest economic forecasts. In addition the ABS releases the “Overseas Arrivals and Departures” publication (mainly focuses on tourist arrivals and departures).

US jobs data hogs the limelight

The US jobs data is considered the most important of the monthly statistics. The data is released on Friday.

The week begins on Sunday when the National Bureau of Statistics releases the results of purchasing manager surveys for manufacturing and services. Australia and New Zealand will be the first markets to react to the data on Monday.

On Monday the US version of the purchasing managers manufacturing survey is released. In China the private sector Caixin manufacturing survey is released with the equivalent services gauge on Wednesday.

On Tuesday the April data on new vehicle and truck sales is released together with the usual weekly figures on chain store sales. New vehicle sales are expected to have lifted by 3.5 per cent to a 17.15 million annual rate.

On Wednesday, there is rash of US indicators for release. The usual weekly data on mortgage applications is released together with factory orders, purchasing manager surveys for services, international trade and the ADP national employment index.

On Thursday, the usual weekly data on claims for unemployment insurance is issued together with the Challenger job layoffs series.

On Friday, the US jobs report – non-farm payrolls – is released. And the focus will be on all the key measures – job growth, unemployment and wages. If jobs rise by 203,000 in April as expected with hourly earnings up 0.3 per cent, then the Federal Reserve should remain on track to lift interest rates in June. Consumer credit data is also released on Friday.

There will also be six speeches by US Federal Reserve officials to watch over the week.

Sharemarket, interest rates, currencies & commodities

The US earnings season hits its peak in the coming week. A total of 1,432 companies will issue earnings results according to Zacks Research, up from 957 companies the previous week. However there are fewer of the ‘household' names to report. Earnings of S&P 500 companies are expected to have fallen by 7.1 per cent in the first quarter (March quarter) compared with a year earlier. However earnings in the second quarter are expected to be down only 2.3 per cent according to Thomson Reuters.

In Australia, three of the Big Four banks are scheduled to report earnings in the coming week. Westpac is expected to issue results on Monday with ANZ to follow on Tuesday while National Australia Bank earnings are slated for Thursday.

According to current pricing in financial markets, there is now a 58 per cent chance of a rate cut on Tuesday. Looking further out, a rate cut is fully factored by August. In fact financial markets believe there is a real chance of a second rate cut by the end of the year.