Eureka stocks reporting season preview

Summary: Reporting season delivers a deluge of primary sources on the earnings and performance of ASX listed companies. This year's February half year results are predicted to see a decline in earnings per share of ASX200 companies of around 4.45 per cent, but there are many opportunities to watch out for. I believe the market will reward companies who perform well, while those who report lower than expected figures will be treated severely given current market conditions. |

Key take out: Watch out for mining, banks and insurance stocks, as I believe they will be reporting less than stellar numbers. The IT sector, including companies focused on data storage and internet security, appears to be on the rise. |

Key beneficiaries: General investors. Category: Shares. |

In February, the vast majority of our stock recommendations will report financial accounts to the market, for the period ending December 31 2015. For most, this is a half-year report, but some are providing annual results. Given it's February 1, what better time to look for key themes this reporting season, take stock of the importance of this time of year and provide a few stocks to watch as the month unfolds?

Get across what you need to know about this reporting season below - and don't forget to tune in to our reporting season primer webcast this Thursday February 4 from 12:30pm. You can register for a reminder email here: A reporting season preview. I'll join James Kirby, Simon Dumaresq and Tim Treadgold to take your questions live.

Why is reporting season so important

In Australia, listed businesses must provide audited accounts to the market twice a year. For most, this is in August and February (September and March for mining stocks).

During this time companies will release financial statements as well as strategy updates and management discussion on a company's progress. There is an overwhelming amount of fresh primary information that can be used to review portfolio holdings, and to generate and identify new investment opportunities.

Most companies are valued by the market on their fundamentals, and on the market's expectations for future fundamentals. So, when reports are provided with key financial information like profits for the period and cash generated, these will either meet, exceed or fall short of expectations. It is this event driven market sentiment that will likely determine a stock's share price reaction during reporting season (and in many cases, for the six months thereafter).

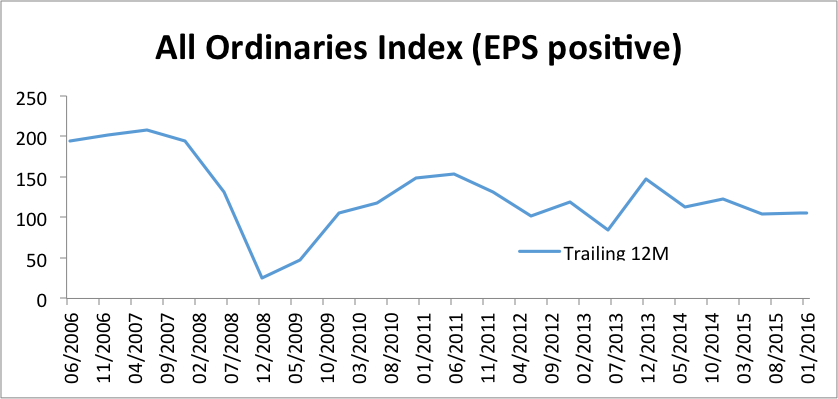

This reporting season expectations (according to Bloomberg) are for earnings per share declines of around 4.45 per cent overall (on the S&P/ASX200). Given the issues at some of the major contributors to the Australian market, it is no surprise that the market is soft, with growth not apparent at the larger end of town. Unsurprisingly, a look back at the trailing earnings per share of the All Ordinaries shows how volatile Australian earnings have been over the last ten years. It may seem obvious but the key thing to note about this chart is that the price of the market has a high correlation to earnings performance. Thus, earnings are likely to continue to be a key driver of market prices going forward:

Source: Bloomberg

What to expect this period

Expectations leading into this reporting season are, in a broad sense, quite subdued. The market has endured a weak six months, and is prepared for some pretty ugly numbers from the likes of our largest firms (BHP, RIO, CBA, WPL, etc). Sentiment is prepared for softness. That said, any results that disappoint this expectation will be dealt with by the market severely. We need to look no further than the earnings downgrade from Shine Lawyers (SHJ) recently to see that a share price can be savaged by more than 75 per cent in a day if the market receives bad news.

This is exactly what I expect this reporting season. Good reports will be rewarded, and are likely to be numerous due to low expectations. But, should a company disappoint, the downside risks are elevated in a skittish market.

Miners & banks are the backbone of the Australian market on a market cap weighted basis, and their relative underperformance has weighed on overall sentiment. Herein les the opportunity.

As prices are lower, and PE ratios have contracted, the bulk of the market has been re-rated lower, swept up with worries of oil, iron ore and mortgage lending ratios. The reality in reporting season is that these factors mean little to most businesses. Good businesses that are strong operations and deliver strong results should see rewards flow through to shareholders. For example, I highlighted Credit Corp as a strong business (one on my watchlist, read more: Searching for income outside the big bank stocks, December 14, 2015), and the company has already reported a very solid half upgrading earnings guidance for the full year. This was received with a more than 10 per cent share price lift from what would be described as subdued levels sold down with the broader market. These are the opportunities to look for: Stocks that have perhaps not performed as they should due to market performance, but have strong fundamentals that will shine through in earnings season.

Key positive themes

So, where should I look this reporting season? There is so much information in reporting season and an overload of stock reports. Keep an eye on Eureka Report as we will highlight new stocks and review reports through the months of February and March.

But, in anticipation of the fact that so many of you like to keep your finger on the pulse, I have identified a couple of themes to look for when seeking stocks of interest.

Small caps that are uncorrelated to macro problems. This is the crux of where I think outperformance will be generated again in 2016, after it was the key place to look in 2015. Identifying small caps that have profits, positive operating cash flow and a bright future will be key.

The rise of the Chinese consumer, and the export of consumer goods to China is a theme we have seen play out in 2015, with some very notable share price performances from Bellamy's (BAL) and Blackmores (BKL). The problem is that most of these companies are priced for perfection now. The Growth First model portfolio recently added Pental Limited (PTL) to its investments, and I think there might be more ideas and successes to emerge in small caps in this space. Investors should beware some of the eye watering prices, but also take note that beneath this is a strong theme that should be considered when creating a watchlist this reporting season.

Cyber Security, IT and telcos is another emerging space. IT has changed in the last five years. The way data is hosted and stored has moved IT and telco businesses away from the traditional, with emerging industries of infrastructure development, cyber security, data storage centres and hosted services starting to gain real traction and profitability. NTC performed well in 2015, and with a shiny new contract may have the ability to continue its performance through this reporting season. DWS is a more traditional IT services business, and EPD has had some issues of late, but this is very much a sector that appears on the rise and should uncover opportunities as reports are delivered.

Areas for caution

Mining, banks and insurance. It's that simple. Unfortunately, that is not an exclusive list, but it is in my mind the three most exposed areas of the market that Australian investors are probably struggling to manage. Many of us hold BHP and think it is too low to sell now, but we all thought that at $20 and probably $25. The banks are the backbone of many income investors' portfolios, but for the franking credit lovers among us, it's also hard to sell while it is paying eight per cent yields. But there is a problem. Resources prices are weak, and banks could cut their dividends.

Finally, I mention insurers as an area of caution. The reason is that I think insurance is seeing some cost pressure from rising interest rates and some issues in terms of claims. We saw Suncorp downgrade margins recently, and I think there might be industry wide pressures. Our preferred way to play the space is to look at the brokers who don't take any underwriting risk (more on Steadfast (SDF) below).

These are only a few of the potential mines this reporting season. Remember, a good company will provide strong profits, cash flow to go along with the profit and an outlook that shows future growth.

Three growth model highlights

AMA Group (AMA)

The AMA share price has languished following the company's merger with Gemini. This reporting season will provide a good chance to see the progress of the integrated group and may remind investors of the growth story in this industry leader.

Netcomm Wireless (NTC)

Netcomm posted a stellar 2015, culminating in its announcement that it had won a major contract for the supply of devices to the US rural broadband project. With more news likely to flow on this company-making contract win, NTC is well placed to provide a solid catalyst with its result this period.

Pental Limited (PTL)

Pental is a solid domestic manufacturer and supplier of domestic cleaning products in Australia. However, with the potential for a strategic expansion of sales into overseas markets, namely China, PTL has the potential to provide the market with some strategic news that may catalyse share price sentiment further.

Three income model highlights

Steadfast Group Limited (SDF)

SDF is expected to benefit from any increase in premiums in the insurance industry. While it may be a little premature to expect strong premium growth (the industry has been contracting in terms of pricing), there is some expectation that the cycle is turning. SDF is in good shape to provide a strong update and dividend.

G8 Education Limited (GEM)

GEM has been uncharacteristically quiet in terms of announcements of late. This is probably for the best, as the company needed to take time to put some runs on the board and digest the many years of acquisition-led growth. With expectations that the company will report a strong end of year cash position and strong profit growth, GEM is trading on a low PE with a gross dividend yield in excess of 10 per cent.

Arena REIT (ARF)

Property prices again posted a strong half to December 31, 2015. Revaluation will likely assist ARF's reported profit. However, with strong earnings visibility and a very clean outlook we expect a solid report from ARF later this month.

Pay attention and have a strategy

Ignoring reporting season is probably the worst strategy. The days of passive buy and hold investment are probably behind us, as the speed of information processing, business execution and market reaction means cycles are shorter and reactions are stronger. Anyone still holding BHP knows that strong early decisions are likely to benefit and protect your portfolio.

Reporting season is a key time for those trying to make the most of their equity portfolios. Decisions should be made based on rational analysis of information. The beauty of reporting season is that the information is fresh, and everyone is brought fully up to date with a company's fortunes.

Here are five tips to approaching reporting season:

Plan

Know your portfolio, and what you are looking for in order to either confirm or negate investment thesis in each stock you hold.

Develop a watchlist

Do some research and look for stocks that might fit your portfolio. Find out when these companies are likely to report and know what to expect.

Have information available

Eureka Report will be with you every step of the way, but you should look for company announcements, media and other sources of information to assist with your investing.

Understand your own risk tolerance

While some of us might be happy to continue to hold a stock that has dropped 50 per cent most of us shouldn't. The fact is that risks in a stock like this are too high, even if it is “cheap”. Decisions to buy, hold or sell should not be made in isolation, but in the context of your own goals and risk appetite.

Think portfolio

In the same breath that a stock might be considered risky when it falls 50 per cent, it might be considered a bearable risk if a small exposure within a portfolio of otherwise uncorrelated stocks. Risks, returns and goals should be evaluated in light of the overall portfolio. Remember if one stock is running hot, it might become a heavy weight in your portfolio and erode your diversification so selling a winner might be a good idea.

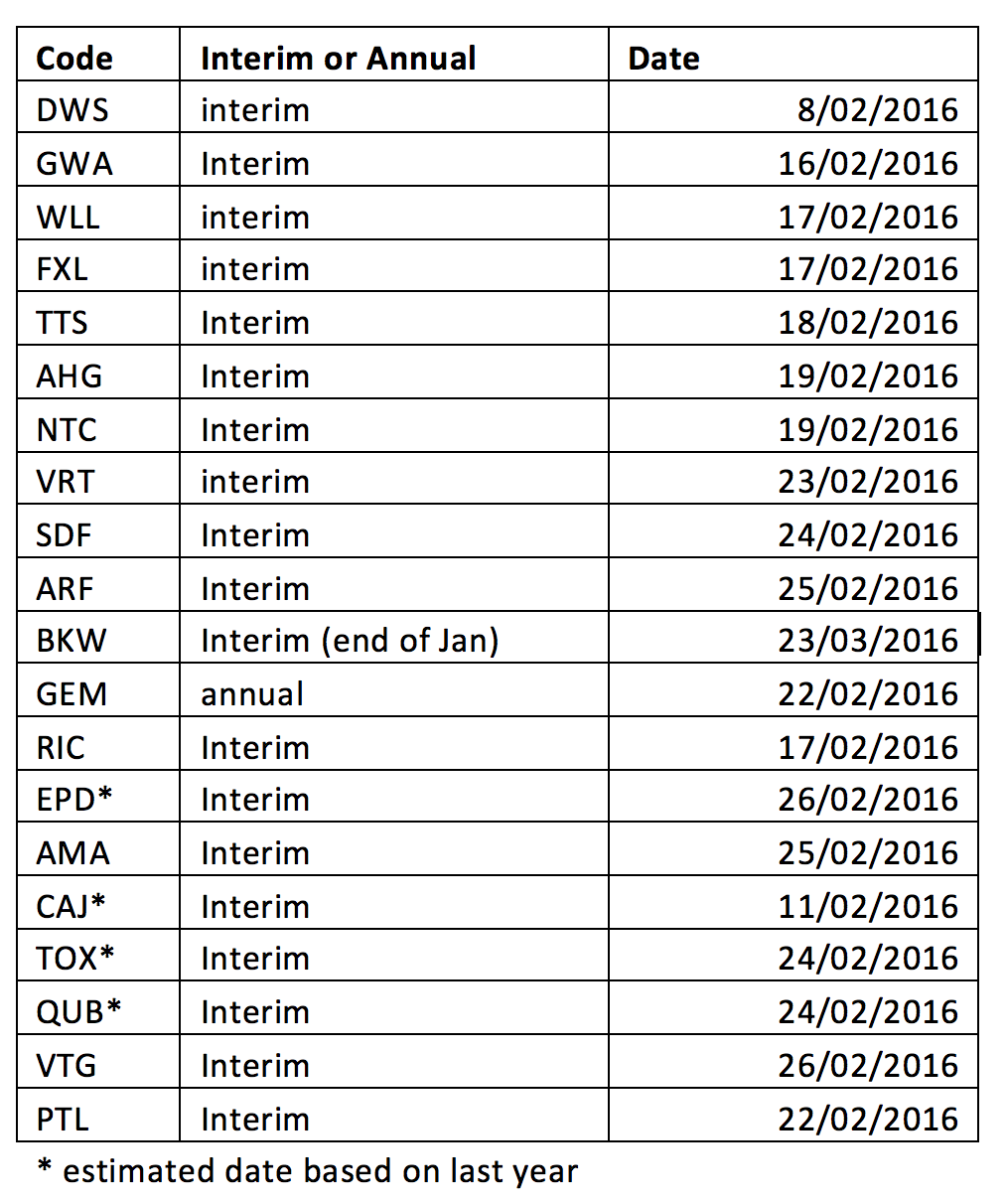

To assist those of you who follow the Eureka Report model portfolios, below is a list of the companies in both portfolios and their respective expected reporting dates this earnings season: