Earnings Season: Four trends supporting better numbers

Summary: Four factors are boosting earnings. Lower commodity prices are here to stay, and will support non-mining earnings. Lower crude oil prices also look structural. Wages are low, but as the population ages over coming decades, workers will be in short supply. Low interest rates are also structural. |

Key take-out: Lower input costs (other than low wages) are here to stay and should provide a tailwind to corporate earnings. |

Key beneficiaries: General investors. Category: Economy. |

Depending on who you ask, the upcoming earnings season, which comes into full swing this week, will either be dreadful or okay. Much of it depends on whether you're looking at earnings excluding the miners and whether you think those falls in commodity prices will go on in perpetuity, or not. Most of the larger brokers appear to look for earnings per share growth of about -1.5 per cent or 4 ½ per cent stripping out the miners – with much of the rhetoric describing such a result as reasonable but not spectacular.

We‘ll find out in due course – but until we get a little more clarity on this particular season, I thought it was worthwhile to look at some of the key tailwinds supporting the longer-term earnings outlook.

In looking at this, we have to distinguish between mining and non-mining earnings. Largely that's because what we're seeing in the mining space is a one off price hit to earnings. Prices won't fall forever which leaves volumes growth (which is strong) as the long-term story for resource companies. This short-term pain is more about price discovery.

Otherwise, and for the most part, there is little disagreement as to whether these tailwinds exist. Most analysts acknowledge them to some degree. The key question is whether these are secular trends and thus longer-term influences – or just cyclical swings (and thus shorter-term in nature). Let's go through each in turn.

Lower raw material costs

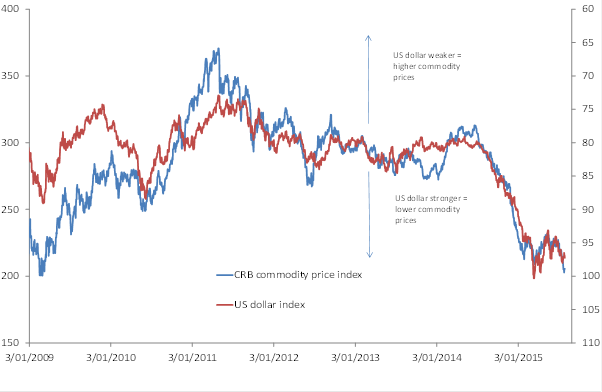

You name it, commodity prices are tumbling. In US dollar terms, commodity prices (CRB index) are down some 44 per cent from a peak in 2011. Most of that has actually occurred over the last year – since June 2014, commodity prices are down just over 30 per cent.

Chart 1: CRB Commodity price index

As to whether this is a secular or cyclical support for non-mining earnings, I think the answer is a bit of both and a lot depends on your view of the US dollar.

That's because the US dollar is the key influence driving prices down as you can see from the chart. So for instance, that 30 per cent slump in commodity prices was largely driven by a 22 per cent spike in the US dollar index. The US dollar for its part is at its highest level since 2003. Even on a longer time frame the importance of the US dollar can be seen: On a four year view, the USD is up 27 per cent, while commodity prices are down 37 per cent. The US dollar is not the only impact though – there is that 10 per cent that is specific to commodity markets.

Having said that, there is very little appetite in the US for a higher exchange rate – which in part is why the Fed keeps on delaying the first hike. It was initially to be 2010, then June 2015, then September, now the market looks for a 2016 hike.

More to the point, even when the Fed does hike, it has a few actions up its sleeve that will be dovish enough so that the market doesn't overreact. Like revising down the end-year rates forecast, or hiking by only 0.1 per cent instead of 0.25 per cent. Anything to try and moderate the inevitable knee-jerk market response. So that should limit any further US dollar upside.

While there may not be too much more upside to the US dollar, markets shouldn't expect too much downside either. The dollar index has had a hard run up, there's no doubting, but it's not too far away from its longer-term averages (since the 1990s). On that measure the US dollar may be only 7 per cent overvalued.

In that sense, the commodity price weakness that we're seeing now is here to stay. Not that there is likely to be much more downside. Longer-term scarcity is still the real issue. Neither does there look to be much upside – a gentle lift over many years is where the fundamental forces lie. That would suggest a new equilibrium will be found around current levels, and that cheaper commodity prices – relative to pre-GFC – are here to stay.

Cheaper energy

Obviously energy prices come under the commodity banner but they deserve special mention, mainly because crude does have some clear momentum of its own. Crude prices are down about 50 per cent just over the last year which suggests price action of more than 20 per cent over and above what US dollar influence would point to. The usual story is that this is driven by a supply glut of oil, but this isn't something borne out by the facts. There is no global glut of crude.

Instead there are a few factors at play operating to lower crude prices. First, the derivative market is shrinking. Pre-GFC it was an $8 trillion market – just in commodities – now it's more like $2 trillion. Second there is no positive growth narrative – like peak oil in 2008 which drove the derivatives market to push the pre-GFC crude bubble.

There is wide acceptance in policy circles now that the sharp rise in commodities pre-GFC was not driven by fundamentals, but was driven instead by speculative flows in the derivatives markets. It's the same now, only the direction is different.

That's because now days it's all about the ‘glut'. So the derivatives market that is left has no incentive to bid crude prices up – they have an incentive to sell.

Third, national governments are operating – through communications strategies etc – to lower the price in order to keep a cap on inflation. We saw this most clearly in 2011 when G7 nations used aggressive rhetoric and the threat of unleashing crude reserves onto global markets to push crude below the $100 mark.

None of these factors is likely to change any time soon which means that lower crude prices look structural. Again, scarcity is the real long-term challenge – prices will rise over time – but all of the above factors will act as a major headwind and moderate price growth.

Low wages

Low wages are an interesting one. Even in economies like the US and UK where the unemployment rate has declined sharply, wages growth remains weak. In Australia we are looking at the weakest wage growth in at least 20 years. This is likely a cyclical influence only however. Why? Because unemployment rates are so low! People whine about an unemployment rate of 6 per cent – it's likely lower – but that is historically a great outcome for Australia.

Wages growth is likely low due to all the fear that has been hitting the market since the GFC – fiscal cliff, Grexit, Chinese hard landing – Australian recession year in and year-out. People have been afraid so wage growth has been low. That will change and we are seeing modest signs of wage acceleration already in the US and UK.

Longer-term, the aging population problem means that workers will be in short supply over coming decades. Technology can only fill in some of the gap, but the broader problem remains: how to lift participation rates sufficiently to pay for an older population.

Low interest rates

On the issue of whether low interest rates are here to stay there is much debate. I've written before about the tendency of many in the finance industry to look at average rates since the 1970s, and assume that is the definition of normal. This is wrong.

Central banks have otherwise told us that rates aren't going to get to pre-GFC averages and the bond market is telling us that rates will remain low for many years to come. Low rates are very much structural.

In sum, lower input costs (other than low wages) are here to stay and this should provide a substantial tailwind to corporate earnings going forward.