Clouds set to clear

Summary: The US recovery is well underway. Once the speculation about Greece passes, it will become apparent that European stimulus is boosting European share prices. In China, actions to stabilise the share market seem to be working. In Australia, migration is beginning to fall, which would create a short-term surplus of dwellings – the RBA could cut rates without boosting dwelling prices, which would highlight high-yielding shares. |

Key take-out: If the Greek and Chinese crises can be contained, the world is in a much stronger position, which is good for share markets. I am concerned that the Iran nuclear peace deal will result in an increase in oil availability, weighing on prices for our LNG producers. |

Key beneficiaries: General investors Category: Economics and investment strategy. |

Because the severity of the deal with the Greeks was so unexpected, we are going to face speculation that it will fall over... I don't think that will happen.

The simple fact is that Greece has to choose between the European dictated settlement or running a country for four or five or six months with no money, no banks and therefore no jobs.

So while nothing is ever certain, the world is developing the way we expected a month or so ago (see A lesson from Bond and Metcash, June 10).

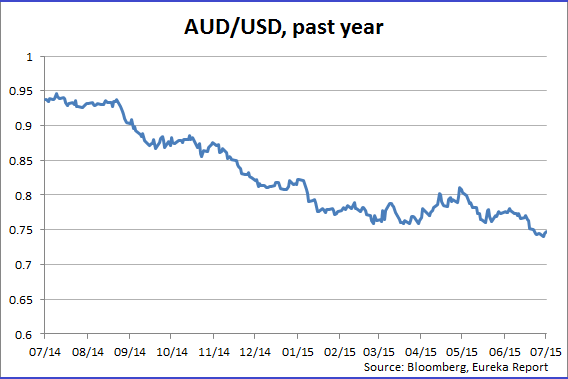

For Australia that means a likely fall in the dollar and the freedom for the Reserve Bank to further lower interest rates should that suit its book. Perhaps the most remarkable event to be obscured by the Greek and China crises was the fact that American consumer spending in May reached levels not seen since August 2009.

It has since come back but the levels are strong. In other words the US recovery is well underway and inflation is benign so that means that America is set to begin its increase in interest rates starting with a rise in September. I suspect that the increases in the US interest rates will be slower than many forecast but, given the pace of the US recovery is quickening, we will need to keep a close eye on the sentiments of the US Federal Reserve.

However the increased US interest rates and the speculation of further increases will suck money into the US and lift the American dollar. And as that happens the Australian dollar should fall. If the American dollar rises too quickly then Federal Reserve Chair Janet Yellen will moderate her interest rate increases because of the danger of hitting American exports and displacing local US industries and jobs.

In Europe once the next two weeks of Greek speculation have passed, it will become apparent that the European stimulation program is starting to have an effect on Europe starting with higher share prices. That is why we saw strong rises in European shares when it seemed likely that the Greek problem would be solved and after a deal was announced.

There is a lot of equity money now investing in the belief that, given the US is lifting interest rates, Europe has a real chance of performing better than was expected a year ago.

Certainly two points of clear market action in the next six months will be the US and Europe.

Over in China the Chinese actions to stabilise their share market seem to be working.

As I pointed out last week the aim of Chinese regulators is to maintain stability in the Chinese banking system and not to allow the share market fall to spread into consumer sentiment (see China is the danger, July 8). The fact that half the Shanghai stock exchange was suspended means that these twin goals – particularly the banking threat – were in jeopardy before China acted.

Having said that there are some signs coming out of China that property prices are beginning to creep up again and if those trends continue and the recent government induced stability in the share market can be maintained China's growth will not fall as low as was feared in the middle of the share crisis. But there is no doubt that China is one of the more dangerous parts of the world at this point and Australia is very dependent on China.

The Reserve Bank is desperate to get our currency down to US70 cents or lower so our iron ore, LNG and coal producers can get better revenue from their low US dollar commodity prices.

In addition a lower Australian dollar stimulates other export industries such as tourism and education. The Reserve Bank has been reluctant to lower Australian interest rates because it feared such an action would further fan residential dwelling prices in Sydney and to a lesser extent Melbourne.

However, it is now clear that the lending clamps introduced by the big banks have curbed housing finance to investors. At the same time while migration remains high it is beginning to fall and once a lower trend has been established we could see a sizable fall in migration.

If that happens then there will be a short-term surplus of dwellings. The massive Asian investment in new apartments in Melbourne and Sydney is predicated on the Australian population continuing to rise strongly; by that I mean people from overseas want to come here and they will find a way but the latest trends are a warning. The lower migration and the fall in dwelling finance now gives the Reserve Bank the opportunity to lower rates without further boosting dwelling prices. The only reason it will not lower rates is that our currency may fall to US70 cents simply because of what occurs in the US.

If Australian official rates are decreased it will highlight the high yields available in Australian shares including bank shares. And that attention to the share market will be enhanced by the fact that, while there will be some surprises, the Australian profit reporting season will be in line with expectations because companies have lowered their costs. Specifically, lower interest rates will tend to push bank profits higher. The banks want to increase their profits because they face the need to raise capital. In a lower interest rate environment they can further punish savers by reducing deposit rates and they may not be as aggressive in their discounts to new mortgages.

The danger to banks, and indeed to the Australian economy, is that with mining investment rapidly running down what is currently keeping the economy going is the investment in dwellings particularly with Melbourne and Sydney CBD and inner city apartments.

If the momentum of this dwelling activity is curbed then the Australian economic growth rate will fall further. In turn that is not good for the share market. But if that's the way it plays out then we will certainly see the Reserve Bank lower interest rates which will increase the value of yield stocks.

If the Greek and Chinese crises can be contained then the world is in a much stronger position, which is good for share markets. The two issues that most concern me is the increased militaristic attitude of Russia and the fact that the Iran nuclear peace deal in time will result in a big increase in oil availability and the consequent lower oil prices will make it really tough for our LNG producers particularly the newer ones where capital costs have accelerated much higher than originally expected.

I am taking a short break but will return in the last week of August.