A private banker's asset allocation for 2015

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Start your free 15 day trial now' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

Summary: Global market volatility is not a large surprise to Standard Chartered Private Bank, which is betting on atypical asset classes such as multi-asset income securities and local currency bonds issued by China and India. It also likes preferred stocks, convertible bonds and REITs. This year, its moderately aggressive portfolio allocates 60% to stocks, 19% to bonds, 13% to alternatives and 8% to commodities. |

Key take-out: Standard Chartered is recommending its clients consider long-short funds to brace for a rise in volatility. |

Key beneficiaries: General investors. Category: Investment portfolio construction. |

The volatility in global markets since the start of the year came a bit earlier than Standard Chartered Private Bank's investment strategists foresaw. That the market is a bit shaky isn't a big surprise, though, and the jitters don't change the bank's stand that the best bets will be in atypical asset classes in the year ahead.

Some of these less traditional strategies include “multi-asset” income securities and local currency bonds issued by China and India. For right now, the global instability, which has sent most stock markets down and bond markets up worldwide, may have nudged open a window to buy into stock markets the bank likes, including the US.

“We don't see this as a bad thing, but people should be aware that things could be a lot more volatile,” says Aditya Monappa, the private bank's head of asset allocation and portfolio construction.

Aditya Monappa, Head of Asset Allocation and Portfolio Construction, Standard Chartered Private Bank

Oil prices were tumbling before Standard Chartered Private Bank's investment strategists created its 2015 investment outlook, yet the strategists were surprised by the quick, steep drop since December. Nymex oil options for February delivery sank more than 13% in the last month alone. Low oil prices are likely to mean inflation will remain soft for a while, even in the US, which has offered one of the few rays of hope in global growth.

A soft inflation picture could give the US Federal Reserve a good reason to hold off raising rates until later in the year, Monappa says. The 15 officials on the private bank's investment committee had expected the Fed would begin raising rates in gradual fashion, in the second or third quarter with a slight bias to the third. The bank's strategy team is meeting soon to reassess whether the slide in oil prices, and a softening in the inflation outlook, will push a rate hike to later in the year, Monappa says.

At the end of last year Standard Chartered said the Fed's first policy squeeze since 2006 could prompt a short-term global stock nosedive of more than 10%. But a rate hike needs to be put in perspective. It's actually good news, a signal that the US economy, after more than eight years, is growing.

Still, short-term swings are likely. To smooth the volatility Standard Chartered is recommending clients consider investing in hedge funds that use “long-short” stock strategies, where a manager buys “long” positions in stocks that are expected to rise, and “short” positions in stocks that are expected to fall. These strategies have underperformed the last three years in a low-volatility world, “but if volatility does pick up, they should do better,” Monappa says.

It's the expectation of future short-term volatility that has also led the bank's strategists to recommend what it describes as “less traditional sources of return both across and within asset classes.”

Take bonds, for instance. Overall, the bank is recommending clients underweight the sector, especially government bonds issued in major developed markets – namely the US, Europe and Japan. With yields low and prices high and the prospect of a Fed rate hike still on the horizon, government debt prices could easily take a hit.

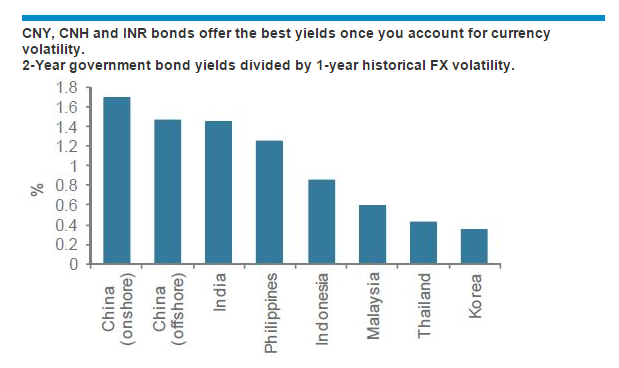

Source: Bloomberg, Standard Chartered Bank

But Standard Chartered likes what it calls “non-core” income, and suggests securities like preferred stocks, convertible bonds and REITs, could bring in additional income and protection from market swings since they don't tend to move in tandem with mainstream stocks and bonds.

“For someone looking for yield or income in their portfolio, in the past you could go to fixed-income for a 4% to 5% yield, but yields in fixed income are near historic lows,” Monappa says. “What we are suggesting is look beyond (bonds) to non-core income.”

The bank is also suggesting you can find extra income in select local currency bonds. Bonds denominated in Chinese renminbi can have yields to maturity at an attractive 4.8%, and little correlation with global stocks, while securities denominated in the Indian rupee also trade at attractive yields and could benefit if India's central bank continues to cut rates.

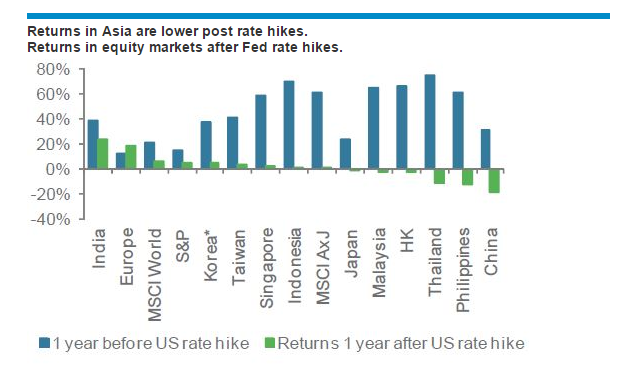

Source: Bloomberg, Standard Chartered, *excluded 1999 cycle

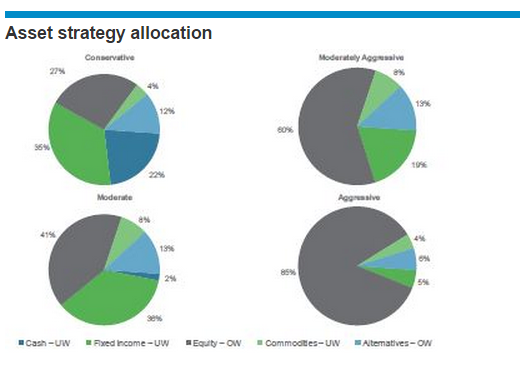

Standard Chartered has offered some of the recommendations outlined here, as well as plenty of others, to private clients along with suggested asset allocations depending on your level of risk. Most of the bank's customers fall in the “moderate” to “moderately aggressive” risk basket. Standard Chartered's moderate portfolio for 2015 allocates 41% to stocks, 36% to bonds, 13% to alternatives, 8% to commodities and 2% to cash, while a moderately aggressive portfolio allocates 60% to stocks, 19% to bonds, 13% to alternatives and 8% to commodities.

The portfolios, which also include conservative as well as aggressive strategies, are just a starting point that is based on the bank's overall view of the markets. “Every client will have a unique set of circumstances, and a unique set of preferences,” Monappa says. “Investment advisors work with a client to implement something specific to their situation.”

Only about 5% of the bank's assets under management are in so-called discretionary portfolios, which mean they are managed by the bank in line with your risk preferences. While low compared with other regions of the world, the figure is in sync with the 2013 industry average in Asia, according to the latest report on global private banking from the Boston Consulting Group.

This is an edited version of a story which first appeared in Barron's on January 16.