Why we're downgrading Brickworks

Brickworks' diversified model continues to deliver, and adds to the long history of outperforming the market. The three main divisions of Building products, Land & development, and Investments (cross-holding in SOL), provides exposure to industry cycles that usually don't move together. For example, the building materials division is currently very strong, but coal has been weak. BKW exposure to coal is through the cross-holding with Washington Soul Pattinson (BKW own 42.7 per cent of SOL), who own 59.7 per cent of New Hope Coal (NHC).

It is our view that an asset based valuation or a sum-of-parts look at BKW is more relevant than an earnings based valuation, due to the lumpiness of the property division, and the investment in SOL being approximately 60 percent of the company's value. The cross-holding means that both SOL and BKW usually trade at least with a 20 per cent discount to their respective sum-of-part valuations.

On an earnings basis, the first half result (January 31 period end) was strong, with the building products division benefiting from very strong demand in the half. Underlying NPAT rose 19.4 per cent to $75 million, excluding $1.9m of significant items. Earnings per share of 0.505 ( 19.1 per cent), and a fully franked dividend of $0.16 was announced.

Building products

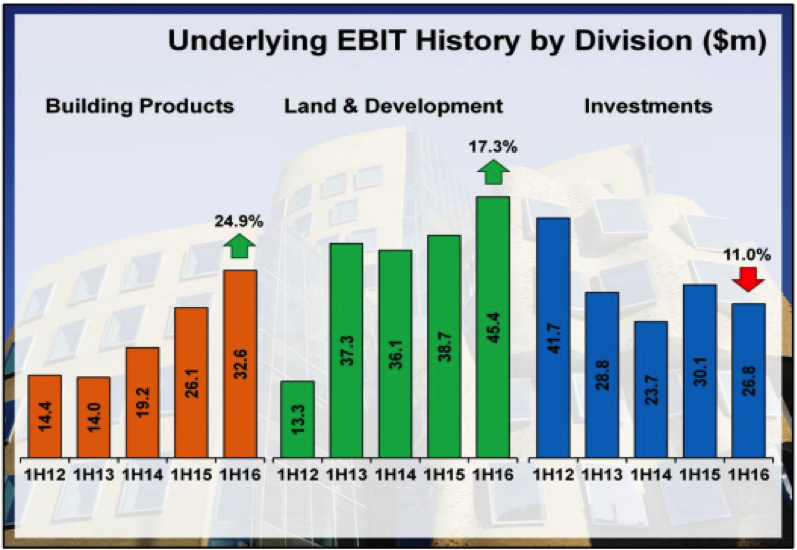

Building Products sales increased 5.1 per cent to $358m, with underlying EBIT up 24.9 per cent to $32.6m. Given the usual fixed cost leverage, EBIT margins increased by 140 basis points to 9.1 per cent, supported by higher volumes and prices.

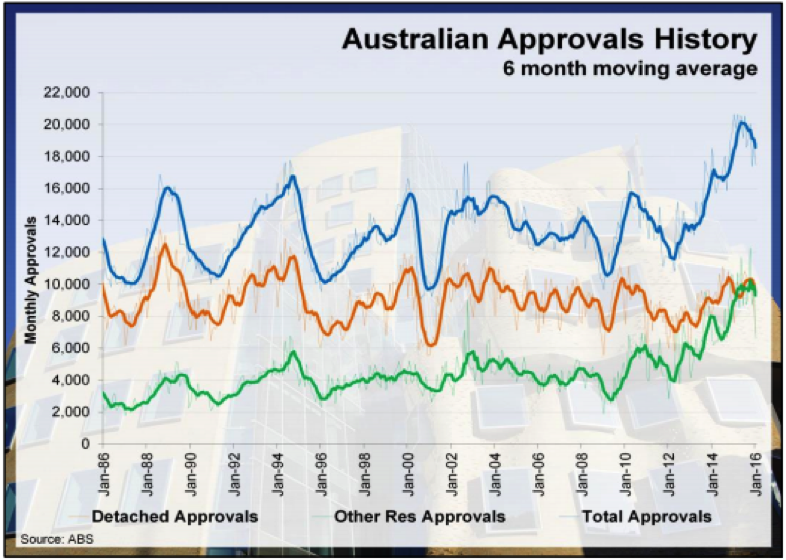

The strong building conditions are expected to continue in the second half. But as can be seen in the chart below, approvals have begun to decline from peak levels. Housing starts usually lag approvals by 6-12 months, suggesting FY17 may be the beginning of a building products cyclical decline. Industry forecasts are for housing starts to decline from 225,000 in calendar year 2015, to around 200,000 in 2016. Management commentary around supply shortages are consistent with the usual top of the cycle conditions.

Orange line = detached houses, Green line = residential, Blue Line = total approvals

Land & development

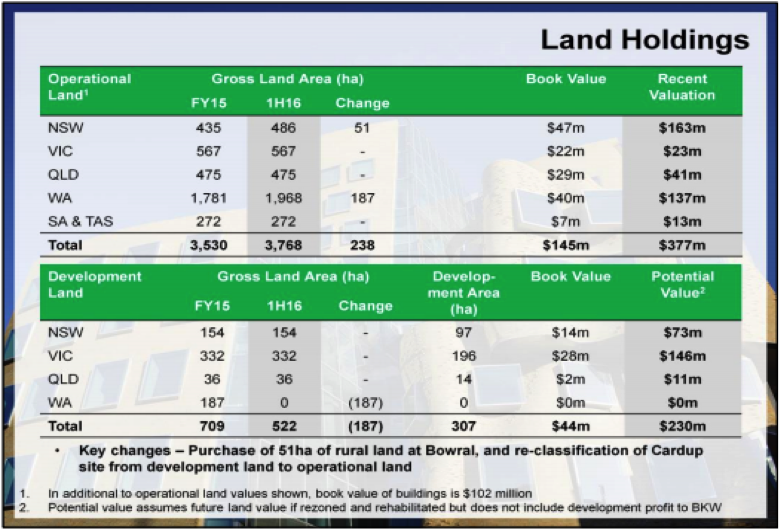

The sale and/or development of large land holdings which are surplus to operational brick manufacturing activities, will supplement earnings for the next decade as a minimum. Land that is zoned as residential is sold on an individual basis, whereas industrial land is sold into a joint venture property trust (with Goodman Group), which provides an annuity income. At the first half the market value of operational land was estimated at $377m, and development land $230m.

Investments (42.7 per cent stake in SOL)

BKW's 42.7 percent stake in Washington H Soul Pattinson (SOL) had a strong first half, supported by TPG Telecom performance. WHSP market value had increased to $1.7 billion as of January 31, despite an 11 per cent decline in EBIT to $26.6m. The driver of lower earnings was New Hope Corporation (NHC), with weak coal prices. But we are attracted to NHC due to excellent management and their consistent ability to sell coal assets at the top of the cycle and buy at the bottom.

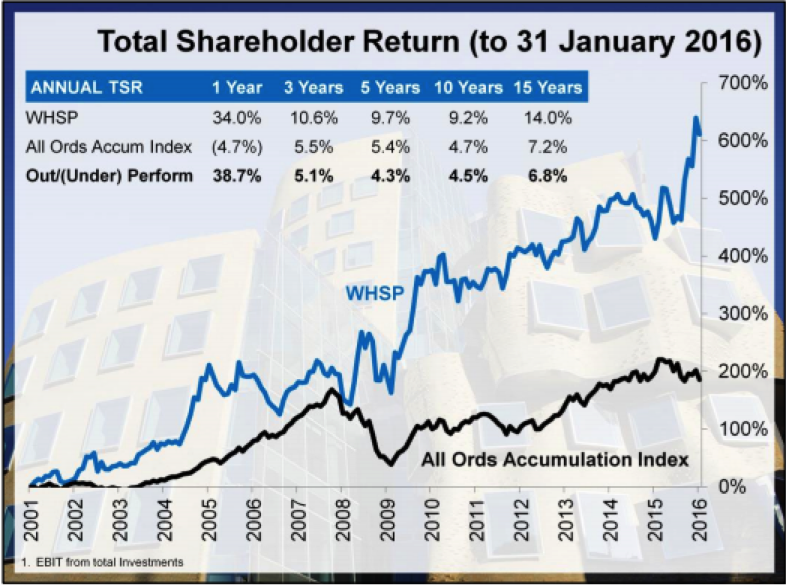

Given SOL's consistency of outperformance and ability to pay dividends, it could be argued that it should be treated as a Listed Investment Company (LIC). With annual returns of 14 per cent for the past 15 years, it compares very favourably to other ASX LIC's.

Sum-of-parts valuation

The table below displays how we get to a $16.48 valuation/target price.

Brickworks (BKW) Sum of Parts | Valuation | |

Building Products (8x mid-cycle EBIT) | $m | 480 |

Land (combined market book value) | $m | 450 |

Investments (market value of 42.7per cent SOL stake) | $m | 1695.2 |

Net Debt | $m | 264 |

Total | $m | 2889.2 |

Value per share | $ | 19.4 |

15per cent conglomerate discount | $ | 2.91 |

BKW Valuation | $ | 16.48 |

The $19.4 sum-of-parts includes the market value of SOL, the land asset value, and an 8 times mid-cycle EBIT building products valuation.

The current $16.0 BKW share price is at a 17.5 per cent discount to the $19.4 sum-of-parts. Typically, BKW trades at a minimum 15 per cent discount to this value, and is usually good buying when the discount gets closer to 30 percent.

For our $16.48 target price we have applied a 15 per cent discount mainly due to the SOL/BKW cross-holding.

We are downgrading our recommendation from BUY to HOLD given our view that the housing construction cycle is in the process of peaking, and the 17.5 percent discount to sum-of-parts is not enough to justify a buy.