Staying with GWA Group

Building fixtures and fittings supplier GWA Group (GWA) has disappointed the market with a revenue downgrade at its annual general meeting. The soft trading update prompted investors to knock GWA shares down by nearly 22 per cent over the first week of November.

The wave of selling flowed into last week, and after a slight bounce, GWA's stock price has settled around $1.83 – just off a three-year low.

It's easy to understand investors' frustration as the GWA story has played out beneath both our expectations and those of the market. Today I adjust my estimates, reaffirm my hold rating and remind readers that although this story remains intact, it will take some time to unfold.

Currency impact

GWA Group put considerable effort into restructuring ahead of the start of FY16. As we explained earlier this year (see Revamped GWA eyes growth, May 11), the firm has divested a range of underperforming businesses, closed manufacturing facilities and moved to import a range of products.

When GWA announced its FY15 result, it pointed to its success in implementing a strategy switch – a new focus on the Bathrooms and Kitchens (B&K) and Door and Access Systems (D&A) businesses. In short, this means GWA now primarily sells toilets, taps, doors and locks. Its brands are true household names – among them Caroma, Dorf, Gainsborough Hardware and API Locksmiths.

After a multi-year string of “one-off” restructuring charges, GWA led fatigued investors to expect that having made tough calls and “taken its medicine”, a simpler model would improve profitability and cash flow.

At the end of October, GWA revealed that this improvement is coming gradually. For the firm's continuing operations, the first three months of FY16 brought net sales growth of only three per cent. This is particularly concerning given the period one year earlier was the weakest quarter for sales in FY15.

GWA has sheeted most of the blame for this anaemic revenue growth to the currency markets. The firm clearly chose a poor moment to outsource its manufacturing overseas, as the past year's weakness in the Aussie dollar has pushed up GWA's cost of production. GWA is quite sensitive to currency movements – each cent the AUD weakens against the US dollar would hit GWA's earnings before interest and tax (EBIT) by around $2 million, absent any hedging or pricing.

GWA has tried to offset this drag on profitability by pushing through price increases. It did so on September 1 to the tune of five per cent for its larger B&K segment and on November 1 for the D&A business. There will be a lag before these price increases become effective as since their implementation, currency has continued to move against them.

The firm does enjoy a proud history of product innovation – after all, Caroma did invent the dual flush toilet – but apart from a new rimless toilet coming in early 2016, few new products are hitting the shelves. The net result is a weighting of FY16 earnings toward the second half of FY16.

Market share losses

GWA can't do much about currency movements beyond its hedging strategy, which at the moment has the firm 75 per cent covered through to June 2016. Of deeper concern to investors is GWA's competitive position, which seems to have slipped.

Customer and competitor Reece Australia (REH) grew sales by 9 per cent in the first quarter of FY16. GWA sells more to Tradelink than to Reece, and as Reece seems to have bolstered its own market position, GWA has suffered due to its customer mix. Decent growth with its other major customer Bunnings has mitigated GWA's market share losses.

The firm has identified some down-trading in the market – consumer aren't necessarily trimming their budgets, but they are shifting toward lower end product. If that shift persists, it will likely hurt GWA on both the top and bottom lines.

Homebuilders vs renovators

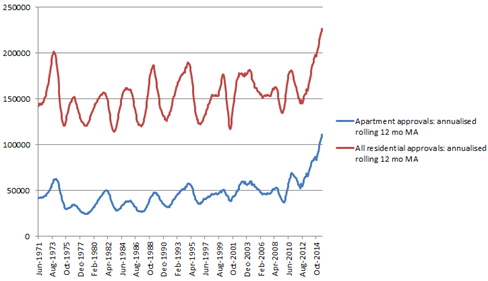

Part of investors' exasperation with GWA stems from industry conditions that should be supporting decent volume growth. Australian Bureau of Statistics (ABS) data show that building approvals were 21.4 per cent higher in September than they were a year earlier.

As you can see in the chart below, the data also reveal that the annualised rolling 12-month moving average of housing approvals has pushed through 227,000. That's more than 12.5 per cent higher than its previous peak in the early 1970s.

All those newly approved homes will eventually need locks, taps and toilets – so at face value, conditions would seem to support GWA. However, the picture is not so simple.

Apartments' share of housing starts has grown steadily, from less than a third historically to almost 50 per cent now. Apartments tend to bring lower volumes to GWA and put some pressure on margins.

At the same time, housing completions have started to lag behind approvals. It seems that homebuilder capacity constraints have caused this lag, as well as the higher contribution from apartment blocks, which take longer to build.

Taken together, these trends should extend the length of the housing cycle and spread GWA's earnings over a longer period. But investors should note that GWA is actually not as heavily exposed to dwelling completions as the headlines suggest.

Around 23 per cent of GWA's sales go to single detached dwellings. Multi residential developments (i.e. apartments) speak for 10 per cent, and about 15 per cent of sales are to commercial property. The remaining sales – around 52 per cent – are in the replacement and renovation market.

On that basis, GWA's prospects rest heavily on renovation activity. This part of the market seems to have been stubbornly flat over the past year.

A new hand at the helm

If elevated home prices entice more homeowners to renovate and sell in the next year, GWA stands to benefit. But a large part of how the firm performs and whether it can arrest its recent market share losses will depend on its managing director-in-waiting, Tim Salt.

Salt joined GWA in September and is formulating his strategy in consultation with customers and suppliers. He comes with a long record of accomplishment at consumer goods firms including Unilever, Pepsi, Arnott's and most recently drinks company Diageo, where he managed the Australia and New Zealand business. Running the alcohol business saw Salt deal with multiple distribution channels and he has experience in working out win-win strategies with key customers. For example, he grew Diageo's business with Woolworths (WOW), which was a competitor with its own brands as well as a key distribution channel.

This experience seems highly applicable to GWA as it negotiates its change from being a local manufacturing business to a distributor of branded products. Salt's appointment bodes well for GWA.

Retaining a hold recommendation

GWA is persevering in the face of economic headwinds and has taken internal steps to address its market share losses. However, its latest update shows our prior estimates of profit and revenue growth have been overly optimistic.

The firm retains a healthy balance sheet and has flexibility to boost shareholder returns, having reduced the capital intensity of the business. It's worth noting that GWA has just announced an on-market share buyback program worth up to $30m. This shows that management is confident in its cash flow position and potentially views the shares as undervalued. The scope for earnings per share growth through the buyback program puts a little upside risk to our estimates.

However, material share price appreciation from here – and a potential upgrade to a ‘Buy' rating – will depend on genuine revenue growth and tangible cost savings from restructuring. GWA has to prove itself to the market on both fronts.

In my view, the recent share price drop seems overdone relative to GWA's earnings potential –consensus expectations of which have dropped by around five per cent since its trading update. We continue to like the exposure this stock gives us to the late end of the housing cycle, but note that the recent developments make the stock look more like fair value than outright compellingly cheap. On that basis we retain our hold recommendation and update our financial forecasts to reflect its latest trading update. We now expect revenue growth of a little over six per cent this year and seven per cent next year, though slower growth in costs should see earnings grow faster.

GWA now trades at less than 10 times our estimates for FY17 earnings per share. Our new valuation of $2.34 reflects a below-market multiple of 12 times our FY17 net profit forecast.

To see GWA Group's forecasts and financial summary, click here.