Price is right at Pental

Consumer products maker and brand owner, Pental (PTL), is on the cusp of a return to meaningful growth. The group has weathered a difficult past four years, and for the first time in recent memory, it has the advantage of several potential profit drivers.

We are confident that Pental's capable management team, led by chief executive Charlie McLeish, can continue to execute well and regain investors' faith. Its balance sheet showed zero debt with more than $11 million of net cash at the end of FY15 and has strengthened through the first half of FY16. This places the group well to expand capacity and pursue exciting growth opportunities.

Pental's potential to grow earnings and attract a richer market valuation leads us to upgrade our recommendation to ‘buy'.

Costs down, margins up

After the group restructured in 2013, Pental's management rightly identified that its manufacturing equipment was too old and inefficient to let the group compete with its global peers. The $5.3m capital project it announced in February 2015 will start to rectify that by modernising equipment that in some cases is nearly 50 years old. As Pental upgrades its manufacturing and distribution facilities at Shepparton (pictured below), it will boost production capacity, reduce wastage and improve efficiency through process automation that will permit a reduction in labour costs.

Source: Google Street View

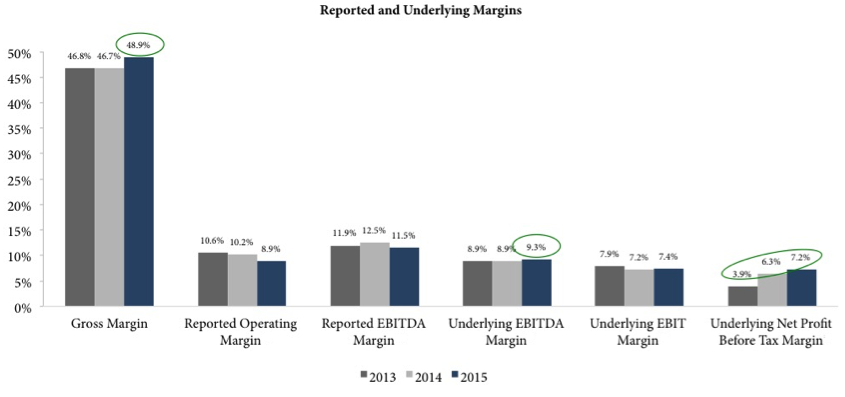

Pental is committed to bringing its facilities in line with best practice, and to that end, has recently hired new managers of production and operations at Shepparton. The company should continually improve its operational capabilities until it completes the first stage of its $5.3m capex program in the third quarter of FY16. That means Pental has plenty of cost savings still to drop out of its structure, the full impact of which investors should see in FY17. This bodes well for continual improvement in underlying margins, the recent expansion of which you can see in the chart below.

Source: Elevation Capital

In the highly competitive consumer goods sector, investors view margin expansion through productivity gains as a baseline expectation. The market is unlikely to grant Pental a higher valuation on cost-cutting alone, but investors will pay up for revenue growth.

If that happens, and if the stock hits our forecast 4.8 cents per share in FY17 - Pental shares - currently trading at 48 cents - will be worth 72 cents each.

Growth initiatives

Pental's brands hold strong market positions across household cleaning, personal care, dish wash, laundry and firelighters. Gross Australian brand sales grew by 5.7 per cent in FY15, and with the firm focused on maximising its return on trade rebates and promotional spend, we see a solid base for Pental's domestic operations.

With things ticking along on the home front, management has been freed up to pursue organic growth through a variety of channels: commercial & industrial, pharmacy, private label, and export.

Pental is planning the installation of a new bulk liquid filling line in Shepparton. This could let Pental sell any of its liquid products in packaging larger than the current norm of two litres — as much as five or 10 litres — and open a point of difference in ‘branded bulk'.

Pental is sounding out the likes of Costco, Officeworks and Mitre 10 (the former employer of CFO Albert Zago), with initial feedback positive. The firm will only proceed with the capital project if it gets commitments from these types of customers in the commercial channel.

Another new prospect Pental is exploring is the pharmacy channel. Pental has never sold its products through pharmacies with any scale, but the group has engaged a new marketing partner that could help it exploit opportunities in this channel. Success on this front could boost revenue and profit, though it will take time to develop.

We see a more immediate opportunity in private label manufacture. This has become an increasingly important driver of Pental's business since the firm resumed a partnership with Aldi around 12 months ago.

Pental supplies Aldi's private label liquid bleach and bar soap, and therefore stands to benefit as the German giant takes the fight to Coles and Woolworths. But as Pental modernises its plant, it will boost its private label production capabilities to support the growth of the grocery majors' own brands. This could see private label continue to grow its share of Pental's sales from its current level of around 15 per cent.

As these plans move from the drawing board to the income statement, we should see Pental spread its exposure away from the supermarket oligopolists and towards a balanced channel strategy.

Export to China

In our view, the most exciting opportunity lies abroad. At its recent annual general meeting, Pental highlighted its plan to accelerate its capability to grow in export markets. The firm is eyeing China and its unbridled enthusiasm for premium Australian wellness, health and beauty products.

To this end, Pental has developed a new range of soaps under the Country Life banner which it calls its ‘Australian series'. As you can in on the left side of the image below, the packaging features iconic Australian imagery and ingredients.

Source: Pental Ltd

Pental is also positioning a range of goat's milk beauty bars (pictured above right) with infusions like honey and green tea for potential export. Both products could ride the coattails of the success of the Australian dairy industry and its perception of quality among Asian consumers.

We understand Pental has discussed product ranging and supply contracting with at least one large Chinese retailer. While gaining orders will be a work in progress, the firm expects to gain approval to distribute through the Shanghai free-trade zone. Pental is also investigating contract manufacturing opportunities for Chinese companies.

The scale of the opportunity to sell premium soap to China makes it hard to forecast an eventual impact on Pental's revenue and profit. But if Pental gains just half of one per cent share of the Chinese market for bar soaps, it could boost the firm's revenue by around $7.5m.

Pental's capex program is positioning the group well to respond quickly to a pickup in demand for its products through any of the above channels. It has plenty of capacity to keep up with sales growth and could add a second daily shift to its Shepparton plant without any issues.

Although Pental's growth plans are still in their infancy, they are undeniably ambitious. In updating our valuation today, we assume a continual slight uplift in margins as Pental drives out costs, and give the firm a 50 per cent chance of gaining a small foothold in China.

If any of the firm's growth initiatives pay off over the next 12 months, it should make the stock look like a bargain on today's figures.

Upgrade to buy

Pental trades today at just under 12 times its FY15 earnings per share. It attracts roughly half the trading multiple of its larger ASX-listed peer Asaleo Care (AHY), despite boasting higher margins and lower financial leverage.

The market discounts Pental because, at a market cap of less than $70m, it is still quite small — and investors have not forgotten the firm's near-death experience in 2012.

Pental's larger global peers, like Unilever, Clorox and Colgate Palmolive, routinely attract price-earnings multiples in the 20s. If Pental can execute on its objectives of securing more meaningful growth opportunities in 2016, the stock will start to hit the radars of many more brokers and investors, and it would not seem a stretch to see this stock re-rate to 15 times earnings.

If that happens, and if the stock hits our forecast of 4.8 cents per share in FY17, Pental shares - currently trading at around 48 cents – will be worth 72 cents each.

We are happy to give McLeish and team the opportunity to execute their ambitious plan, and upgrade our recommendation to ‘buy'. At tomorrow's open we will initiate a 5 per cent position in PTL in the Growth First model portfolio.

To view Pental's forecasts and financial statements, click here.