Outlook stacks up for Brickworks

At the start of this year we recommended Brickworks (BKW), the $2 billion company best known for its building products division.

At the time the stock was trading at $12.32 with a projected price of $14.30. We felt BKW would benefit from favourable housing construction backdrop as well as structural improvements to the east coast brick industry.

Since this time investors have become entitled to a $0.15 fully franked dividend and the stock has appreciated to our $14.30 price target.

Pleasingly, the gap to valuation has closed in a relatively short space of time with the stock now trading around our price target. So the question is posed as to how BKW stands as investment today.

Importantly, a number of key events have occurred since we last wrote:

- The company has reported a strong 1H15 result.

- The Washington Soul Pattinson (SOL) shareholding has benefited from a strong operational result as well as the proposed acquisition of iiNet by TPG Telecom (of which SOL owns 27 per cent).

- The Carnegie/Perpetual shareholder activism case has reached its conclusion.

- The market, and specifically the building materials sector, has continued to re-rate.

While we will discuss the impact of these events below, we believe the favourable housing construction backdrop as well as structural improvements to the east coast brick industry will continue to support BKW's earnings. You can read about both of these drivers in greater detail here.

With the increase in valuation of the SOL investment, the strong 1H15 result and a broader re-rating of BKW's building material peer group, we have lifted our valuation to $16 and retain the “buy” recommendation.

A brief recap on BKW

Brickworks is a diversified business, run primarily by the Milner family who are substantial shareholders. The three main divisions are building products, land development and the cross-holding investment in SOL.

Robert Milner is chairman of both SOL and BKW while Lindsay Partridge is the managing director of BKW.

It appears that given the complexity of the SOL cross shareholding agreement and the nature of the products BKW produces, the company had been overlooked in recent years while its building material peer group (Boral, CSR, James Hardie, Fletcher Building) significantly re-rated.

Strong first-half result

Brickworks delivered a strong result for the six-month period to January 31, 2015. Key take outs from the result include:

- Normalised NPAT increased 17.6 per cent on the pcp to $62.8m.

- Building products EBIT increased 35.9 per cent.

- Land and development EBIT increased 7.2 per cent.

- Investment EBIT increased 27.0 per cent.

- An interim fully franked dividend was declared of $0.15.

Management provided robust outlook comments, giving us confidence in our earnings estimates. Specifically, management expects building products earnings to significantly exceed last year as well as an increase in earnings from investments. Land development earnings are expected to be broadly in line with last year, subject to the timing and value of property transactions.

SOL investments benefiting from strong result and TPG/IIN merger

In late March, SOL delivered a strong interim result with normalised profit after tax up 33.6 per cent to $84.8m.

The key drivers of the result were improved profit contributions from TPG Telecom (TPM), Brickworks and New Hope (NHC).

With record low interest rates and lazy corporate balance sheets across much of the developed world, mergers and acquisitions (M&A) is likely to be a strong theme in 2015. SOL, and by default BKW, have benefited from M&A activity in recent months through the proposed acquisition if iiNet by TPG, which has been positively received by the market.

SOL owns 27 per cent of TPG which recently made an acquisition offer for iiNet. Since we last wrote on Brickworks, TPG shares have increased by over 50 per cent to $9.40. This is part due to TPG delivering a strong first half result but largely due to the proposed iiNet acquisition which will materially increase TPG's scale and deliver significant revenue and cost synergies if it proceeds.

The increase in SOL's share price since we last wrote adds $0.86 to our sum-of-the-parts (SOTP) valuation.

Removal of cross shareholding off the table for now

Last year venture capitalist Mark Carnegie, and Perpetual's head of equities Matt Williams, launched a campaign to unwind the SOL/BKW cross-holding – presenting that it is in shareholders' interests to remove the complex structure. Carnegie and Perpetual owned 12.5 per cent of BKW and 11.7 per cent of SOL, with Perpetual being long-term shareholders of both.

Carnegie and Perpetual believed that unwinding the cross shareholding would result in a tax bill for BKW of $179-247 million, which would be far outweighed by the valuation uplift of this cross shareholding being removed.

However, in July 2014 an unfavorable tax ruling was received relating to the proposed transaction. During the rest of 2014, Perpetual and Carnegie appeared to be considering their position until February when Carnegie sold down its shareholding and cancelled the proposed shareholder meeting. Perpetual commenced selling its position in late March.

While unwinding the cross shareholding has the potential to be accretive to valuations, we hadn't ascribed any meaningful probability that the shareholders agitating for this change would be successful. As a result this doesn't change our fundamental investment view.

To some degree this saga being over should allow management allocate greater focus to running the business. Furthermore, with two significant shareholders exiting the stock, this event may provide additional liquidity and favourable entry points for investors.

Industry consolidation is yet to play out

One of the key reasons that we are attracted to Brickworks relates to the company's exposure to the consolidation of the east coast brick market.

Bricks has been a terrible business to be in in recent years with a decade long structural decline. CSR (CSR) and Boral (BLD) have recently received ACCC approval to combine their east coast brick operations which is the first meaningful improvements in industry structure in years.

We expect that this will result in over 5 per cent increase in brick prices in FY16 with BKW benefiting as the low-cost producer.

In the first-half-result briefing management noted that price rises had been implemented in a number of divisions within the building products business. The full impact of these price increases is yet to be reflected in the businesses earnings.

Importantly, Austral Bricks has announced price increases, which become effective July 1, 2015. As such, the benefits of these price increases won't be seen until FY16.

| Valuation: Despite reaching our price target it remains undemanding - both when compared to domestic building material peers and to its asset backing. |

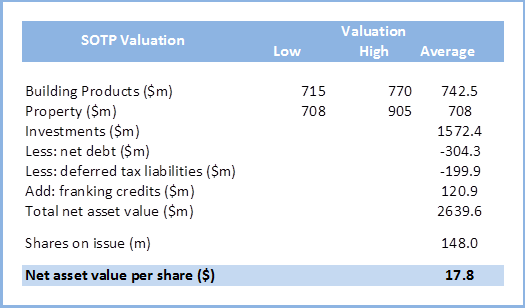

Considering the diverse nature of BKW's business segments we have adopted a sum-of-the-parts (SOTP) valuation methodology. We value the building products division in line with its building material peer group, the property division at net tangible assets (NTA) and the investment portfolio at market value. These are arguably a conservative set of assumptions.

As outlined below, this results in a SOTP valuation of $17.80. Considered another way, the current share price is ascribing an earnings before interest and tax (EBIT) multiple of less than 4 times FY16 earnings to BKW's building products division, other things held constant.

Given the complex nature of BKW's corporate structure, we prefer to use a SOTP valuation methodology as opposed to P/E or cash flow analysis. However, to account for the SOL/BKW cross shareholding we apply a 10 per cent discount to our SOTP valuation and arrive at a price target of $16.