Our top IT takeover targets

On Tuesday October 6, UXC (UXC) announced that it has received an indicative, non-binding and conditional proposal from Computer Sciences Corporation (NYSE:CSC) to acquire all of the shares of UXC. On the basis of this proposal, the company has entered into a process agreement with CSC for a potential acquisition, by way of a scheme of arrangement.

Under the terms of the indicative proposal, UXC shareholders would receive cash payments of $1.28 per share ($428 million), comprising $1.26 cash per share and the payment of a franked dividend of 2 cents per share for the half year ending December 31, 2015. The FY15 final dividend of 3.6 cents per share payable on October 6, 2015 is not affected by this potential transaction.

The proposal reflects a premium of 33.3 per cent to the 120 day volume weighted average of UXC shares. The stock is up 60 per cent this financial year from 76 cents. We have had a buy recommendation on the company with a $1.20 valuation and target price. We last recommended UXC on August 10 (see Upgrading UXC) with the price at $1.00.

At this stage, it is recommended for shareholders to wait and see what comes out of the five-week exclusive due diligence process. It is likely that the UXC board required a conditional proposal to grant this formal exclusive access, with the potential of a higher non-conditional bid when the process is completed. It was announced: “The board of UXC has determined that it is in the interests of its shareholders to engage further with CSC with a view to finalising an implementation agreement to implement the proposed transaction.”

The other factor is that the UXC announcement may promote a competing bid for the company. In the event of a superior proposal CSC will be given the opportunity to match such a proposal. CSC is a global giant with 70,000 employees and $US11.7 billion of revenue reported last year. Therefore they will have no issues if they need to lift their current $428m bid.

In The Australian Financial Review last week, MD Cris Nicolli revealed that the company had been fielding interest from at least one other suitor over about a four month period, but said CSC has firmed as the only serious bidder. Further: “It would be fair to say that we have had significant number of overtures, which led us to have a closer look at the process of what we should do,” Nicolli told the AFR. When asked what the chances are of a competing bid during the next five weeks of CSC due diligence, Mr Nicolli said: “There may be people that have spoken to us in the past that want to show interest, but also there may be people we have spoken to in the past that don't want to do anything, I really don't know.”

From a risk/reward perspective it makes sense to hold on for the five week waiting period to determine if there is further upside from either a sweetened CSC bid or alternate competing bid. The valuation is not stretched enough to suggest material downside if the CSC bid fails to become non-conditional. As such we recommend existing shareholders hold UXC.

Other sector targets?

The UXC bid follows the successful 2014 $171m acquisition of Australian service firm Oakton by global player Dimension Data.

We actually had the fortunate timing of writing about potential IT services acquisitions about a week before the Oakton (OKN) bid in August 2014. We wrote: “Another possibility that could provide a catalyst for the sector would be an opportunistic takeover bid for a deeply discounted company such as UXC, Oakton or SMS Management (SMX).”

With two out of the three from the last list receiving bids, maybe now it is time for SMS Management? Its share price has also been very strong in recent months, increasing from $3.31 to a high of $5.41 this financial year.

Given Mr Nicolli confirmed he has had a number of conversations about potential bids in recent months, as an investor it is certainly worth looking through the rest of the IT services list and deciding who is trading at a discount to valuation and who may be a takeover target?

Usually buying for takeover is a high-risk strategy that over time doesn't pay off. But in this case, there are supportive industry conditions with most companies having recently announced a material uptick in contract wins.

When we talk about the IT services sector we are referencing the companies that align themselves to an IT provider such as Microsoft, Oracle, SAP, Service Now and many others to win contracts on the back of their ability to implement these IT solutions.

In the past the sector has been very cyclical, with the need to replace ageing hardware being the driver of the next upswing. Today and moving forward this cyclical element is likely to be smoother due to the shift towards IT costs being an ongoing operating cost (“as-a-service”) rather than an upfront capital cost.

The case for mergers and acquisitions is to increase the skill base to service existing customers. Or in the case of UXC, CSC actually doesn't have much competitive crossover with UXC, and as such they are broadening their skill base and amount of key customer relationships.

Eureka Report IT services stocks

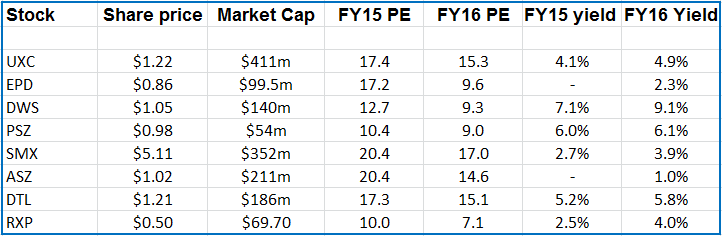

The IT services stocks that we have buy recommendations on are UXC, Empired (EPD), DWS (DWS), and PS&C (PSZ). All of these stocks have been strong recent performers, but so have just about all of the 10-15 stocks in the IT services space. EPD is in the Growth First model portfolio, and DWS is in both the Income First and Growth First portfolios.

Both Empired (EPD) and PS&C (PSZ) have recently said they are on the lookout for acquisitions. But at the same time they could just as easily be a target for a larger group.

James Samson recommended DWS (DWS) as a buy on September 14 (see DWS: Servicing a turnaround), mentioning that the company is on track to deliver a significant turnaround in FY16, with the staff numbers increasing for the first time in three years.

Empired (EPD) has had a particularly strong six months where a higher than expected amount of contracts have been announced and it is now up to the company to execute and hit its targets around decent margin growth and strong cash-flow results. If Empired can do this the stock will re-rate above $1.00 as the market re-rates its FY16 multiple in line with competitors.

PSZ is a smaller, less developed roll-up business that listed in December 2013. We recommended the stock because it has that unique mix of yield, growth and value. After the recent share price recovery the stock has a market cap of $56m at $1.00. It has actually increased 43 per cent since we recommended it in July at $0.70 after the market over-reacted to a slight downgrade (see PS&C: Take a second look).

The security business will drive the PSZ business, having far greater margins and growth prospects than the other divisions. Their earnings downgrades in the past have been due to the company having difficulties determining what work will drop in June or July and the effect on earnings with a June 30 end of financial year. Hopefully Julian Graham (chief financial officer) and Kevin McLaine (chief executive) have learnt to guide the market to a base level that they can hit irrespective of timing differences.

Sector comparison

With UXC having hit our target and now under a takeover bid, Empired (EPD) and DWS (DWS) probably provide the most value and potential upside through FY16. They are both on FY16 price-earnings ratios of less than 10 vs their competitors who are approaching 15 times on average.

Technology One (TNE) probably has the best business model, but it is expensive on a FY16 PE of 28.

Summary

In recent years the banks, corporate and government have been holding back on IT spend, which has resulted in unutilised capacity in the sector and contract pricing pressure. With the recent rate of contract announcements this industry dynamic of capacity and charge out rates should be improving for the IT services companies.

At the current price, the risk/reward stacks up to hold UXC through the CSC due diligence process in case there is a higher bid. If looking to switch into other IT services stocks we think Empired and DWS provide the most value, and SMS Management is the next likely takeover target.