Nickel rebound hopes fade for Mincor

Mincor, a junior nickel miner that operates in the Kambalda deposits in Western Australia, has spiked since our initial “buy” recommendation late last year.

Shares in the company have soared as much as 34 per cent to 75 cents, elevated by outstanding exploration results, strong production and apparently bullish conditions for nickel.

However, following our reiterated call early this year, Mincor hasn't been able to continue with its upward trajectory – slipping to 57.5 cents on Friday's close.

While nothing overt has changed at the company level – capable management continues to excel in exploration and operations are on track – worsening macroeconomic conditions for nickel have tarnished the outlook, with spot nickel prices diving to six-year lows.

Consequently, we downgrade our recommendation to “hold” from “buy” and reduce our target price to 55 cents.

Indeed, in our latest update we warned that Mincor's continued outperformance relied on nickel prices climbing higher in the short term. This outlook has changed.

Unlike several of its Australian nickel mining peers, Mincor is a high-cost producer and, at current depressed nickel spot prices of around $US12,800 per tonne, produces negative cash flows.

Nickel's outlook falls flat

The easiest way to explain the sharp fall in the price of nickel over the past eight months is to say that supply exceeded demand but that only touches the surface of a difficult metal which is being buffeted by multiple factors.

On the demand side there has been a slowing in the rate of growth in the production of stainless steel in China, the biggest single market for nickel, thanks to that country adjusting to slower growth targets set by the central government.

On the supply side there have been a series of destabilising events that range from the Philippines boosting production of low-grade nickel ore to fill a gap created by an Indonesian export ban, and the unwinding to corrupt Chinese financing deals which has seen metal previously stored in Shanghai make its way to the London Metal Exchange and then into an over-supplied market.

It is metal released from warehouses in China after a “double-booking” scandal which saw the same stocks of nickel used for multiple bank loans which has caused LME stocks to rocket up from around 280,000 tonnes at this time last year to 432,000 tonnes today.

In effect, “opaque metal” caught in Chinese financing deals has become visible at the LME.

The Philippines picking up where Indonesia left off is an equally important factor, as is continued strong production from traditional sources, especially Russia where Norilsk Nickel is enjoying bumper profits when US dollars earned from metal sales are converted to roubles.

The same currency effect is encouraging Australian nickel miners to pump out as much metal as possible, with the net effect being an over-supplied market which is estimated to have led to a worldwide over-supply of around 90,000 tonnes nickel last year, adding to the 180,000 tonne over-supply in 2013.

This year the nickel market could absorb some of the stockpiled material but it will not be until next year that the full effect is reflected in the price.

Encouragingly, the next big move in the nickel price should be substantial. Consensus forecasts are for it to rise above $8/lb in FY16 to almost $9/lb by FY18.

Indeed, while the replacement of missing Indonesia nickel by the Philippines minimised the effect of an expected “supply crunch”, the growth in overall nickel supply likely to be limited over coming years.

However, nickel has a habit of producing surprise results, which can be seen in its extreme cyclical price swings with supply and demand rarely in balance.

For miners the vagaries of the market for nickel means that the swing from financial feast to famine (and back again) can be rapid.

Operations

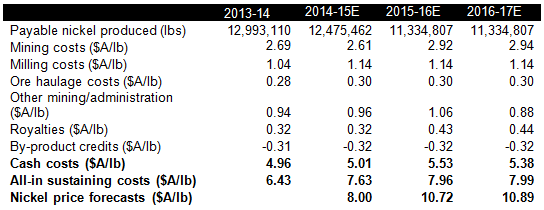

Chief executive David Moore has worked hard to cut costs in the face of declining nickel prices, with the company on track to beat cash cost guidance of $5.30/lb of payable nickel – averaging $5/lb in the first half.

While spot nickel prices are around $A7.5/lb at the moment, we forecast all-in sustaining costs – which include corporate costs such as depreciation – to be around $7.63 for FY15 (as shown in the table below).

Moore says not much scope exists to reduce costs further. The company has been focused on cutting them for the past four years and any further reductions would likely be incremental.

Based on revised nickel price forecasts for FY15, we expect Mincor to lose around $10m in cash for the year. Mincor ramped up capital expenditure by 40 per cent to $14m to pursue promising exploration initiatives, but we question whether they will now be wound back if weak spot prices persist.

Soft nickel prices and, to a lesser extent, lower grades from operations in the third quarter, have overshadowed Mincor's stellar successes in exploration over the past few months, such as at Cassini.

In the third-quarter production report last week (April 13, 2015), nickel production fell 22 per cent to 1,937 tonnes of nickel in ore. Lower-than-expected grades at Miitel and Mariners were responsible, at 2.29 per cent and 2.74 per cent respectively.

As we have said, our optimistic view on Mincor in small part rested on better-than-expected production. At the end of the first half the company only had to maintain the first half's 4,986 tonnes of nickel in ore to beat full-year guidance of between 8,000 and 9,000 tonnes.

At the end of the third quarter nickel-in-ore production stands at 6,923 tonnes – meaning a beat on for FY15 relies now on Mincor lifting production by around 10 per cent in the fourth quarter compared to the previous quarter.

This is now less certain, though Moore asserts that production in the fourth quarter should return to levels seen in the first two quarters.

We still expect Mincor to release a final dividend of 2 cents per share in FY15 – taking the full year dividend to 4 cents per share – given its unbroken track record and a positive outlook for nickel in the longer term.

Valuation

Mincor's share price doesn't currently reflect the heightened risks, with the company not making money at this year's nickel prices.

Based on our model's assumptions, Mincor requires an average nickel price of $US7.70/lb in FY15 to be profitable. While earnings have benefited from the fall in the $A (payment is made to Mincor in $US), they have been hit more by weak nickel prices that have only fallen further.

Our $A forecasts remain at US85 cents across FY15, but fall to 75US cents in the following years from our previous estimate of US80 cents. But even with the lower $A boosting earnings, particularly from FY16, Mincor appears overvalued.

The market currently factors in higher nickel prices into Mincor's share price – even after the stock fell. If we assume spot prices stay flat at around $US5.81/lb for the remainder FY15, our DCF valuation falls to 42 cents.

Recommendation

We downgrade our recommendation to “hold” from “buy” and reduce our target price to 55 cents.

Mincor, as a relatively high-cost producer, is more leveraged to the nickel price than its peers. Our initial “buy” recommendation was grounded on a short-term rise in the nickel price, but this hasn't eventuated.

Given the lack of a catalyst and Mincor being loss-making at current spot prices, we can no longer justify our bullish stance on the stock.

To see Mincor's forecasts and financial summary, click here.