New Relic's analytical prowess

New Relic, based in San Francisco, is a software analytics company that operates in the realm of “applications performance management” or APM. The company's products and technology are delivered from “the cloud” as “software as a service” or SaaS.

Essentially, it monitors web and mobile applications in real time, giving insights from the billions of metrics that a firm's software is producing, including user click streams, mobile activity, end user experiences and transactions. Not only does it give clients a quantitatively robust picture of application performance but it also provides analytic functions on the data produced in order to facilitate decision making.

New Relic actually operates in a market that is at the intersection of application development, IT operations, and business intelligence or BI. These markets have traditionally been owned by the so called “legacy” or established product vendors like CA, Computer Sciences, SAP and IBM.

The explosion of big data and the subsequent implementation of a number of new development languages like PHP, Python, Ruby, and others that have burst on the scene to help develop web/cloud applications is creating significant opportunities for disrupters like New Relic which can offer solutions that are cheaper, faster and easier to deploy.

New Relic's competitive advantage is its cloud based platform which can amass vast amounts of data no matter what programming language is used. Incredibly, it offers these services for as low as $US140 per month.

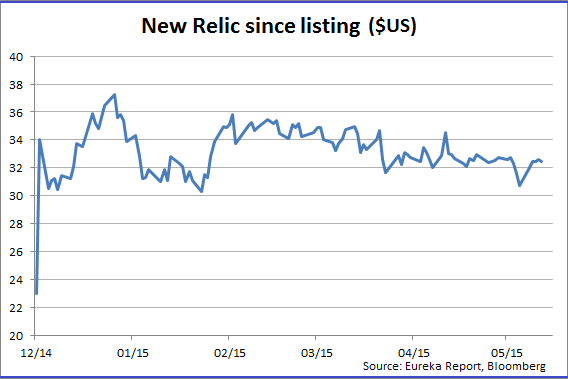

New Relic has only been a public company since December 12, 2014. On the first day of trading it gained 43 per cent.

In its first earnings report as a public company on February 12, New Relic handily beat consensus estimates for earnings per share and revenues. Billings accelerated to 93 per cent year-on-year and average revenue per user (ARPU) increased 26 per cent. The company has grown revenues 132 per cent per annum since 2012 and has over 11,000 customers of all sizes. Sales are estimated to grow at 50 per cent per annum to 2017.

On May 12, New Relic reported its fourth-quarter results. Earnings per share topped consensus, and the company guided for first-quarter and full-year results higher as well.

Revenue in the three months ended in March rose 68 per cent, year over year, to $US33.4 million, yielding a net loss of 22 cents, excluding some costs. Analysts had been modelling $US30 million and a US25 cent loss.

The quarter's results beat the company's own forecast for revenue and profit offered back in February.

For the current quarter, the company sees revenue of $US34.5 million to $US35.5 million, and a net loss of US23 cents to US26 cents, compared with consensus of $US32.5 million and US24 cents.

For the full year, the company sees revenue of $US155 million to $US159 million, and net loss in a range of US95 cents to $US1.03, compared to consensus for $US147 million and a $US1 loss per share.

The company also noted signing new customers such as Jet.com, Ladbrokes Digital Australia, Panasonic Europe and Weight Watchers International.

Why it's time to consider New Relic

So we have a recent IPO with two solid earnings reports and the stock trading some 20 per cent below its recent highs. As per our “seasoning” strategy (see The rise of the unicorns, May 18) whereby we see how the company performs as a public entity, I think it's time to seriously consider New Relic.

The total addressable markets for IT operations software, application development and business intelligence will exceed $US50bn by 2017. Legacy providers are not well placed to serve this market and New Relic has few real direct, pure play competitors.

New Relic has a rather innovative sales and marketing model in that some 70 per cent of revenues are coming from a low cost and aggressive inbound digital/telemarketing campaigns to drive growth and shorten sales cycles. The other 30 per cent comes from a more traditional enterprise focused approach which should increase penetration in the larger Enterprise environment.

Investing in high growth companies like New Relic (and Splunk and FireEye) requires more of a “venture capital” mindset since profitability may be years away. Focus on revenues, the size of addressable market and level of potential profitability – not earnings per share.

My long term growth and profitability assumptions for New Relic have revenues expanding at a 38 per cent at a compound annual growth rate (CAGR) to $US400M in 2019 with gross margins averaging 80 per cent. Margins of this magnitude are attainable since the cloud platform that New Relic has built that can capture, store, manage and analyse massive amounts of data with relatively low capital investment.

Long-term earnings forecasts can often be difficult, especially in hyper growth companies as management has the option to invest more aggressively to capture growth, or to begin focusing more on operating leverage and bottom-line profitability.

In my assumptions I have New Relic reaching both positive operating income and EBITDA by calendar 2019. There is, however, the potential for a couple upside scenarios that can dramatically decrease the time to profitability. It could be as early as late calendar 2016 or early calendar 2017 solely depending on levels of investment and upside to revenue.

As a guide, the company spent just over 70 per cent of revenue in the last quarter on sales and marketing as it continues to invest heavily to build out its direct sales for customers with over 1,000 employees and expand its international reach. This level of spending will decrease over time as the company reaches critical mass.

Valuation and recommendation

New Relic is a high risk “buy” at current prices on the basis of its potential growth, two quarters of good execution as a public company, the size of the addressable market, the lack of nimble competitors, its compelling value proposition and its innovative products.

My target price of $US45 is based on a calendar-year 2016 enterprise valuation to sales multiple of 13.5 times. That multiple is comparable to other high growth software names such as Splunk, FireEye and Workday and is below where it is trading today.

Risks

- Enterprise penetration stalls or falls short of expectations. New Relic needs large companies to embrace its product suite and eventually represent some 50 per cent of revenues for the company to maintain its growth trajectory.

- The 180 day lockup expiration will see 41 million shares eligible for sale in mid-June. The stock price could be pressured as a result.

- CA (formerly Computer Associates) is suing New Relic for patent infringement. This is the perennial problem of the successful disrupter where legacy providers try to protect their markets. Usually settled out of court, these lawsuits can take years to be resolved. Damages are usually unquantifiable and can cause share price volatility. Litigation expenses can of course squeeze cash flow but even if successful, it is unlikely to disrupt New Relic's already substantial businesses as the company and the market has already moved substantially beyond the original applications performance management patents which are now over seven years old and don't involve the new programming technologies.

To see New Relic's forecasts and financial summary, click here.