NetComm and Ridley surge ahead

NetComm Wireless (NTC)

It has been five months since we first flagged the potential for NetComm Wireless to win a large contract in rural broadband to expand on its successful work with the NBN (see NBN rolls out higher earnings for NetComm, June 29). Since then, the NTC share price has rocketed by more than 280 per cent.

Last week, we indicated that the market was hotly anticipating NetComm to make an announcement on this front (see NetComm flies as Capitol slips, November 23). On November 25, that announcement came — and it's a genuine game-changer.

NetComm has been successful in its tender to provide devices to telco giant AT&T's US rural broadband project. These devices will let up to 13 million households in rural areas across the US connect to a fixed wireless network that AT&T will build.

We broadly agree with managing director David Stewart's comments that this is “a key milestone in NetComm Wireless' global growth strategy for regional broadband… we see potential for this technology solution in many different countries”.

Earnings impact

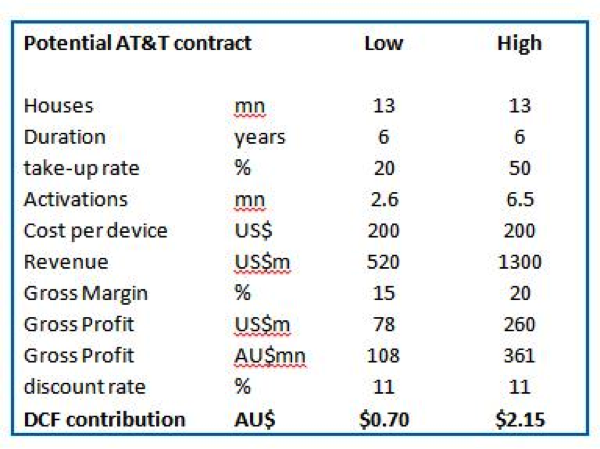

The value that NetComm extracts from this contract will depend on a variety of factors. Some are dependent on consumer behaviour, while others remain confidential. As a refresher, here are the variables — taken from a report AT&T lodged with US regulators.

It's worth noting that the US opportunity extends beyond these initial figures. To begin with, AT&T would likely extent the contract beyond its initial four to six year duration, assuming NetComm does as good a job in the US as it has for the NBN. That could see the take-up rate rise to as high as 90 per cent as late adopters grasp the value of the service.

Then there is the concept of technology refresh. As NetComm continues its investment in research and development, a service that might commence offering download speeds of 25 Mbps should develop over a few years into a faster service provided by a new device. If we assume this technology refresh to come over five years, it could boost NetComm's device sales by more than one million units per year, kicking off when the initial contract is winding down. This could give NetComm's program an ongoing lifecycle as its rollout peaks — giving its contract almost a perpetual quality.

Beyond the AT&T contract that should cover 13 million homes, there are another 20 million homes in the US that could become available in future through other telco providers.

From Australia, to America, to the world

The Boston Consulting Group values the rural broadband market at around $80 billion. NetComm is close to cementing the first-mover advantage in this sector.

In several places around the world, telco operators are replacing their copper delivery networks with fibre. They are trying to solve the problem of how to economically deliver good bandwidth to rural customers beyond the reach of a fibre rollout.

Having successfully demonstrated its capability in solving this problem for the NBN, and now having won the contract to do a larger project for AT&T, NetComm is in the box seat to win the next prize — a contract to cover 750,000 rural households in Ireland.

If NetComm wins that contract, it is unlikely that any competitor will have an in-field demonstration case of its capability for at least three years. That would put NetComm streets ahead to win more rural broadband work in Mexico, Latin America, Japan and across Asia.

At gross margins of around 20 per cent, this work does not attract super profits and therefore should not see competitors flocking to take away NetComm's work. The firm now has a golden opportunity to own the sector globally.

We have updated our model to account for the present value of the AT&T contract, which we forecast as $1.24 per share. We have added a premium for the likelihood of winning further contracts in rural broadband. Our valuation rises from $1.38 to $2.49 per share.

Today we reiterate our hold rating and point out that NetComm's strong price action has propelled the stock into “ten bagger” territory — up nearly 1,000 per cent at last week's peak from when we initiated on NTC with a buy rating at 34.5 cents (see Earnings season: Expect the unexpected, February 5, 2014).

We want to retain some exposure to NetComm's growth prospects but it would be prudent to take gains off the table here. On that basis, at tomorrow's open we will trim three percentage points from our portfolio holding in NTC. The way we see it, having bought low, we're now lightening up with the stock on a high — while its prospects remain rosy.

Ridley Corporation (RIC)

Fortunes are on the rise for Australia's leading animal nutrition provider, Ridley Corporation (RIC). Ridley's share price has rallied strongly through November after the firm cast a millstone from its neck in selling its Dry Creek property.

At its recent annual general meeting, managing director Tim Hart confirmed that Ridley's agribusiness is growing healthily across all lines. The firm retains two key drivers of potential growth: new feedmill projects in the medium term and property development plays further down the track. On that basis we reiterate our buy rating.

Dry Creek

The fate of Ridley's 5,000 hectare property at Dry Creek, 12 kilometres from Adelaide's CBD, has played on investors' minds for years. As it is a former salt field, Ridley has been spending around $3 million per year to meet the environmental requirements that come with ceasing salt production.

Earlier this month, Ridley achieved a $35 million headline sale price for the site. $19m of this is receivable before March 31, 2016, with the balance coming in tranches until the end of 2017. Ridley has monetised an illiquid asset at an attractive price and brought to an end the $3m annual cost of remediation.

Ridley plans to turn what had been a drag into a real driver by recycling that capital into development capex. Selling Dry Creek will fund Ridley's new feedmill in northeast Geelong.

Supply chain savings

The new feedmill should bring, as Hart told us, “huge supply chain advantages”. Until now, Ridley has been taking grain from the Western Districts on a 150 kilometre round trip for processing at Pakenham in Melbourne's southeast, then back to its rendering plant at Laverton in west Melbourne. The new location will save one of Ridley's key customers a material amount on logistics costs, the benefit of which the customer will split with Ridley.

The new feedmill should pay for itself through efficiency gains with the logistics savings an added bonus. These benefits won't flow for some time, as Ridley has only recently commenced the 18 to 24 month construction project, but should help to boost Ridley's return on funds employed (ROFE) through the cycle to a level consistently north of 15 per cent.

These returns should rise as additional newly planned feedmills boost capacity in aquafeed in southern Victoria or Tasmania, and poultry in central Victoria.

Diverse growth

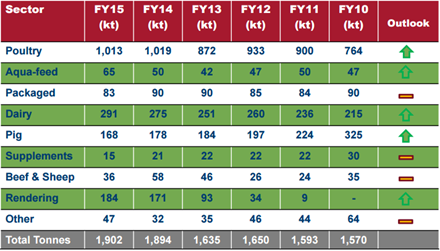

Ridley is planning to boost capacity at a time when its agribusiness is growing across all segments. Although poultry, which comprises more than half of Ridley's feed volumes, is growing at only around 2.5 per cent, this masks strong growth in layer poultry (for eggs) which are growing at around eight per cent.

The chart below shows how volumes have grown up to June 30, 2015 and Ridley's outlook for each segment.

Source: Ridley Corporation Ltd

Aquafeed remains an exciting play. This business feeds salmon, prawns, barramundi and kingfish, all of which are growing well. Although it makes up only three percentage points of Ridley's volume, it is growing at annual rates close to 10 per cent, and should benefit from Ridley's major research and development initiative — Novacq.

This is a product that CSIRO developed and patented that, when fed to prawns, grows them at 1.4x the rate of other feed. Ridley has the rights to produce and sell Novacq in Australia, Thailand, Indonesia and the Philippines — some of the world's biggest prawn markets. It will take another three years before Novacq is producible at a scale that generates earnings, but Ridley has moved toward securing a site that lets it start commercial scale-up within 12 months.

Property

Selling Dry Creek has liquidated 90 per cent of the value of Ridley's land bank. The firm retains property at Lara next to Avalon Airport and at Moolap close to Geelong's CBD. Neither site features any infrastructure and together they are carried in the books at a combined value of around $3m.

The Lara property could rise in value if Avalon Airport seeks to expand its operations. With no immediate need for cash, Ridley can afford to wait for favourable developments.

At Moolap, Ridley has proposed a $4bn marina development in a joint venture with Sanctuary Living. The approval process has been slowed by the new Victorian government undertaking a “strategic land use assessment” of the region. With the local state member, Lisa Neville, also the Minister for Environment in a swinging seat, the political crosscurrents don't seem conducive to a swift approval. On that basis, investors should not expect a breakthrough any time soon at Moolap — though if the planned residential development goes ahead, home sales could bring attractive annuity-type revenues to Ridley.

Earnings impact

We update our model to reflect Ridley's property sale and a slight uplift in agriproduct revenue. We note that the share price's strong recent run takes RIC to a valuation of nearly 20 times the consensus estimate for FY16 earnings per share. Although plenty of growth is now priced in, Ridley remains a buy for those seeking exposure to an agribusiness success story and a potentially valuable development at Moolap.

To see Ridley's forecasts and financial summary, click here.