Healthy consolidation for Capitol

We first identified Capitol Health (CAJ) in July 2014. At the time the stock had declined to $0.42 due to concerns over proposed changes to government healthcare funding after the 2014 May federal budget. Fast forward ten months, and the market again has the same concerns with the budget due to be released on Tuesday, May 12.

The budget risks are the likely driver behind the recent share price pull-back from $1.10 to $0.92. But these risks need to be balanced out against the positives of being able to more easily acquire smaller operators if there are any cuts – specifically in radiology and GP payments.

We don't see any short term impacts from potential radiology budget changes as the process of industry consultation is in its early stages. This is part of the government review of all Medicare funded processes. Further, with the proactive management team we believe Capitol Health is well placed to adjust to any potential changes.

General practitioners (GPs) are Capitol Health's largest referrers, and the likely budget outcomes for GPs are a freeze on the rebate for four years or a patient co-payment. If it is a rebate freeze, then not adjusting for inflation each year it is affectively a cut of $2-3 per year per patient visit to GP incomes. We don't expect the GP funding changes are likely to have a major impact on the company.

With radiology (diagnostic imaging), it is the non-hospital Medicare licensed MRI machines where Capitol Health has the most budget related exposure. Over the last couple of years the government made a strategic decision to enable greater accessibility to non-hospital MRIs. The way this has been done is allocating a fixed amount of Medicare licensed MRI machines, with GPs having the ability to refer patients at no cost.

In comparison to X-Rays, Ultrasound, and CTs, the MRI scan is the highest quality and at the greatest cost (when not Medicare funded). The benefits for the system in promoting greater MRI use are to remove unnecessary hospital visits and improve initial diagnosis.

Capitol Health has 9 of the 24 Medicare licensed MRI machines in Melbourne and now have 7 in Sydney with only another 10 due to be released in the next two years. Any reversal of this MRI government support would need strong evidence of unnecessary use that it is having a net negative cost impact.

If there are no changes to radiology funding, and it is only the relatively minor GP impact, then Capitol Health may have a positive share price response after the budget.

Consolidation – Victoria largely done, NSW gathering momentum

Along with the government funding increasing support for greater MRI access, the other large share price driver has been the accretive acquisitions of smaller radiology clinics in Victoria.

The smaller clinics are capital intensive in terms of both the cost of machines and labour. Therefore the synergy benefits of joining CAJ make it a relatively easy decision for many radiologists.

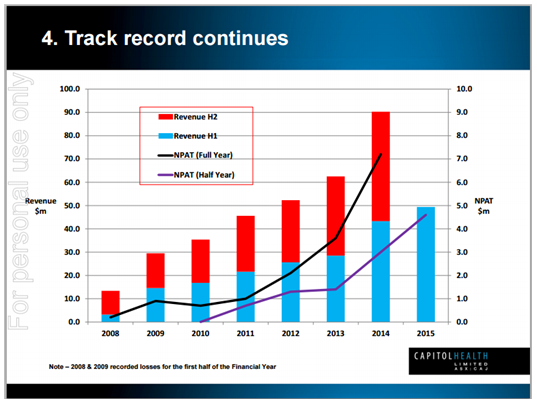

The revenue and profit growth in the chart below paints a very positive picture. The good news moving forward is that the opportunity in New South Wales is most likely greater than Victoria.

New South Wales is the largest and most fragmented radiology market in the country – with 35 percent of national radiology revenue.

Last week the company announced the acquisitions of Eastern Radiology Services and Sydney Radiology for a combined cost of $30 million. The acquisitions add to the existing NSW exposure from the Southern Radiology purchase.

The transactions are immediately earnings per share (EPS) accretive, and expected to provide further benefits from extended trading hours, synergies and more efficiently managing the workflow by integrating into the existing network.

The two acquisitions produced a combined 2014 revenue of $13m and earnings before interest, tax, depreciation and amortisation (EBITDA) of $3.75m. The enterprise value to EBITDA multiple of 8 is roughly inline with prior purchases, but this time funded purely from existing bank facilities and cash.

Management noted the company has also commenced commissioning a new clinical facility in Broken Hill.

With a strong under-geared balance sheet there is further capacity for cash/debt funded acquisitions. The current 15 per cent debt to equity ratio is more than manageable, as is the 12 times interest cover ratio (EBITDA/net interest).

Increasing non-medicare exposure

Although the company has been a large beneficiary of the Medicare funded MRI expansion, management also recognise the need to diversify.

The acquired non-Medicare MRI machines from last weeks announcement were highlighted as a key component of the transaction.

At the half year result Conidi discussed his intention to enter the high margin hospital radiology market and has identified several tenders that will come to market this calendar year.

Another opportunity may be collaborating with private healthcare participants such as the health insurers.

Valuation – why CAJ trades on high multiples

John Conidi and his team have built a strong track record of selecting appropriate acquisition targets and successfully integrating them.

Historically they have focused on quality radiologists with clinics that can be run more efficiently. The typical range of EBITDA multiples that they pay is from 7 to 9. However this becomes 5-6 times after improving utilisation of machines and also cutting costs from the more efficient operations of the broader group. The radiologists are incentivised to remain in the business and their access to the broader management capabilities is a major positive driver.

With CAJ trading on an EV/EBITDA multiple of 16 times FY16, it is relatively easy to achieve accretive acquisitions. Going forward to justify the current PE multiples we need to make the assumption that similar efficiency gains can be achieved from future purchases.

With the proven processes and successful integration track record, there is likely to be more and more radiologists enquiring about joining the broader group.

Our FY16 earnings per share forecast of 3.4 cents increases to 3.7 cents in FY17. Nine per cent earnings per share growth would not normally justify a price-earnings (PE) ratio of 27 times. It needs to be highlighted that this growth forecast does not include the further acquisitions that are almost certain to occur.

Given the balance sheet capacity and the apparent lack of constraints around multiple integrations at the same time, we would expect this FY17 growth rate will be significantly higher than our current forecast 9 per cent.

Further, if history is repeated, then our assumptions around efficiency benefits will be proven to be understated in our forecasts.

The two recent acquisitions have increased our prior FY16 and FY17 EPS assumptions by approximately 5 per cent.

Our DCF valuation has increased from $1.05 to $1.10. Although we haven't specifically forecast future acquisitions, our DCF valuation does assume higher than usual sustainable growth rates past FY17.

Summary

A conservative approach is to wait for the budget details around any healthcare cost cuts next Tuesday. Our view is that unless there are major cuts to licensed Medicare funded MRI machines then any budget related share price weakness should be seen as a buying opportunity. Regardless of the budget outcome, radiology remains a growing industry for the long term. We also believe that Capitol Health (CAJ) is better placed to react to any funding changes than its smaller competitors.

To see Capitol Health's forecasts and financial summary, click here.