Another look at G8 Education

There have been problems at G8 Education in recent months, as the company's takeover bid for rival Affinity Education (AFJ) was trumped by private equity group Anchorage Capital.

Additionally, the Takeovers Panel has made declarations as to the actions of Jenny Hutson. Hutson of course is G8's chairwoman, and has announced her resignation effective on October 15. Unfortunately, and despite her being adamant of the contrary, it seems that Hutson's involvement with the AFJ takeover has come under some scrutiny, making her position untenable.

This coupled with the ever lingering stigma left by the collapse of ABC Learning, has caused the GEM share price to fall foul of expectations.

At this stage, the company is going through significant change in terms of how it communicates with the market. We see this as an opportunity for managing director Chris Scott and the current leadership team to rebuild the company's reputation such that further value is unlocked for shareholders.

With respect to the underlying business, we remain confident that GEM will deliver strong profit growth. Thus my expectations for 24 cents of fully franked 2015 dividends remain unchanged, and again this implies a very attractive yield.

That said we are sticking with our current holdings in the Income First model portfolio, which was an initial 4 per cent weight. This lower weight (compared to some of our other holdings) is a result of my acknowledgment that risks exist in the sector, and the fact that I'd like to see GEM put a couple of years of solid growth and balance sheet conservatism before I take additional risk into the portfolio. I have removed the AFJ earnings from my numbers, noting that my valuation falls from $4.65 to $4.12.

AFJ, Jenny Hutson and the Takeovers Panel

On July 3, GEM announced a hostile takeover bid for AFJ, and followed that up with an all-cash offer. This bid was rejected by the AFJ board and eventually failed, with the company selling its assets to private equity firm Anchorage Capital.

Unfortunately, as a part of this process AFJ has alleged that GEM's chairwoman Jenny Hutson had a relationship with three parties that were holders of AFJ shares including JB Super Fund, Taxonomy Pty Ltd and West Bridge Holdings Pty Ltd. All of these companies bought AFJ shares after the initial GEM bid on July 3. The implied part of this is that the circumstances suggest these companies had links to Hutson (Hutson's sister is involved with JB Super, and there have been historical dealings and investment links between Hutson and the other two companies). I should note that Hutson also refutes the claims of the Takeovers Panel regarding that implying any ongoing relationship with respect to this recent transaction.

But, despite Hutson's view, the Takeovers Panel found on October 6 in its announcement to the market that the acceptances of the GEM bid for AFJ by these companies occurred in uncommercial circumstances. The Takeovers Panel has gone on to such an extent in its declaration of unacceptable circumstances that it suggests that GEM was deemed as acting in concert with these other investors, and as a result breached provisions of the Corporations Act. Specifically this relates to the 20 per cent ownership limit s606, the creep provisions under s671B and some other provisions that are related to the bidder's statement including the above mentioned relationships.

I spoke with both GEM's managing director Chris Scott, and then the Takeovers Panel, to ascertain the potential impacts of these findings. Essentially, ASIC will need to make allegations for the matter to proceed further. Scott's view was that this was likely to involve Hutson, and that the impact to GEM itself is likely to be immaterial from a financial perspective. When I spoke with the Takeovers Panel, it was noted that similar cases have resulted in the transactions being put in the hands of ASIC, but that there was not a lot of material or punitive action that the panel could take. Any further actions would be left to ASIC by either formal or informal referral for the Takeovers Panel.

As mentioned, the Takeovers Panel has described Huston as having “structural links” with the three parties to the transaction in question. Regardless of their true nature, the conservative option would be to disclose these relationships up front, and inform markets fully of the potential perception. The fact that best practice has not been followed in this regard is disappointing.

However, as suggested by both Scott and Takeovers Panel director Allan Bulman, the financial impact to GEM is likely to be immaterial from the Takeovers Panel. The real damage here is reputation, and any lingering potential action that could come as a result of ASIC investigations. I have contacted ASIC, but was told that at this stage it is too early for the regulator to comment on the matter.

The next steps will be for further information to be published by the Takeovers Panel including detailed reasons for the decision.

The G8 reaction: What will it take to rebuild trust

So, GEM is without a chair as of October 15, and the last chair has left in what could be termed ungraceful circumstances. Where to from here?

The stock is trading on a forward PE well below the broader industry, and the market has lost confidence and trust in the business. I posed this question to Scott, who mentioned that the focus for the very near term was to appoint a new chair. Once this is achieved the strategy can evolve, and the management team can address concerns regarding the financial performance of GEM. I note at this stage that GEM has avoided providing official profit guidance to the market until now, and that the provision of forecasts could provide the market with some clarity in the future. We will wait and see.

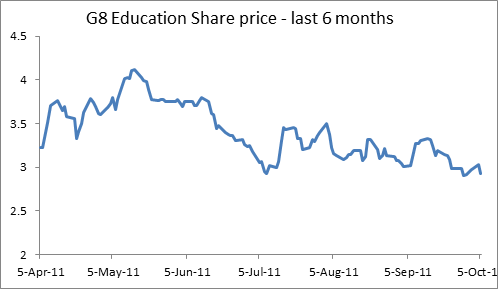

Unfortunately, I do believe that it will take some time for the market to recognise value here. Short selling in GEM is rife, as are rumours and discussions of the company's future potential. Our view remains largely unchanged: GEM is paying a 6 cent fully franked quarterly dividend, and in the longer run is worth more than the current share price suggests. The following graph shows that the GEM share price has been a little lacklustre in the last six months. However, in a market that has been falling heavily and in spite of the continuing stream of disappointing news the share price has been, and will continue to be, underpinned by the dividend.

Forecasts and dividends

I have revised my forecasts to adjust for the recent events. This has meant that I have removed the expected share issue, debt raising, and acquisition of AFJ. Additionally, I have removed the earnings uplift afforded by the potential AFJ acquisition. At present, this has reduced our expectations for FY15 and FY16 EBIT, though I note that GEM is likely to make additional acquisitions to contribute positively to these periods.

For now we are taking a conservative approach. Our expectations in terms of EBIT for FY15 are revised down to a little under $150 million. I note that this still represents almost 40 per cent EBIT growth on that achieved during FY14. Following on from this I have used highly conservative assumptions for FY16 and beyond, allowing me to build what I believe is a base case valuation.

Perhaps the most pertinent point to our numbers is the expectation that the dividend will be maintained into FY16, with expectations for marginal increases to flow through as and when the company makes and integrates further acquisitions. At the current 6 cents per quarter, and with a share price under $3, the yield is not an issue based on the current payout. In fact the cash yield is over 8 per cent, which is more than a whopping 11.4 per cent including franking credits. So investors are being rewarded for taking a risk here.

Given the strength of the yield, I believe that GEM does not need to push as hard at growing its dividends per share. Rather, the cash could be used to continue to strengthen the balance sheet, and the company's acquisition funding mix. Again, the use of cash to maintain this balance will be a key consideration as we monitor GEM into the future.

The investment case and portfolio strategy for GEM

GEM remains a compelling investment. The stock is yielding 8 per cent, plus franking value (11.4 per cent grossed up). Given that the income is paid quarterly, and the track record for dividend growth is very strong, I am surprised by the level of discounting that is occurring in the GEM share price. Yes there are risks, and investors should go into this stock with eyes wide open as to those risks.

So what are the risks? The GEM balance sheet does contain a reasonable level of gearing that will need to be serviced. In our view the FY16 net debt to EBITDA will come in around 2 times. This is high by normal standards, but not astronomical so as to ring any alarm bells. In fact net debt to shareholders' equity is expected to be a respectable 55 per cent (approximately). So, from an operating and financial perspective, GEM is still in good shape. As mentioned, forecast growth probably justifies a higher PE than the market is currently pricing, but the breakdown in trust for the company will take some time to repair.

At initiation we valued GEM at $4.65, but we have now adjusted this lower to account for the loss of AFJ, and a more permanent derating of the market multiple applied. Nonetheless, I am retaining a buy call on the stock, and remain cautiously optimistic that the business will be able to use this situation to refresh its relationship with investors for the better.