Woolworths' lesson from Packer. Rate roulette. Super rules.

Robert Gottliebsen

Why directors must mind their own business

Back in 2001 James Packer learned the hard way an investment lesson that has helped him boost the family fortunes over the last 15 years.

And it is one that the boards of both Woolworths and BHP Billiton could profit from. And later in this commentary we will see some remarkable interest rate predictions by the Commonwealth Bank, and I will point out that the daily press is now starting to wake up to what we have been saying in Eureka – that the government's superannuation plans are a disaster for the long-term health of the nation.

But first back to 2001. James Packer and Lachlan Murdoch were both investors in the emerging telephone company OneTel. The reports coming to the board were very favourable and it looked as though OneTel would emerge as a real winner. Then suddenly it all fell over and within a short space of time the company was broke. The problem for OneTel was that its telephone-bill collection system wasn't working properly, and the revenue that the board thought it was receiving simply couldn't materialise because the system wasn't working properly.

What James Packer needed to do was to walk down to the OneTel call centre and listen to the total frustration that those handling the calls were suffering. Fifteen minutes in the call centre and Packer would have known that the OneTel business was in deep trouble.

And if he had discovered that early enough, perhaps the business could have been rescued. Packer received one of the great verbal blasts from his father, the late Kerry Packer. James never forgot that mistake and realised how important hands-on checking is in making decisions. Maybe Kerry's choice of language was what we would call foul, but it was also effective. (Maybe as parents and grandparents we should transfer our knowledge more forcefully.) But the OneTel lesson goes wider than the Packers.

If you are investor in a particular company providing services and goods for you, and that company doesn't perform well, it is often the signal there is better place to invest your money – and, of course, the reverse applies. I don't know whether Woolworths directors walked around the Masters operations but certainly the people from Bunnings did and they concluded that Masters had no hope after studying the operation for about six months. Woolworths did not make such a study and just kept compounding the errors. But there is now a new test facing Woolworths and all the major retailers including Myer, Bunnings, etc. Almost all of them have agreements with their workforce that enable people working nine to five to get more than the award, but people working on weekends and shifts receive less than the high shift allowances and penalty rates prescribed in the retail awards. There is a very good chance that this will be overturned and, if it is, the cost of weekend trading by all the major retailers will rise sharply.

Very few of our major retailers have done enough work on preparing for that possible eventuality. In the case of Woolworths and Coles, there is a dangerous two-way squeeze taking place at the same time. Down at the low price segment of the market Aldi has an operation that is very efficient. Woolworths and Coles try to pitch their in-house brands at prices that match Aldi but in the overall business their blend of products are aimed at a more affluent consumer. Yet the drive to cut prices dominates the strategies. So into this melting pot comes David Jones, which is now owned by the South African retailer Woolworths Holdings (no relation to the Australian Woolworths). In South Africa about 22 per cent of Woolworths' turnover comes from upmarket food, and they plan to duplicate the strategy in David Jones. This means the majors are being attacked at both ends – by Aldi at the lower end and David Jones in the upmarket area. That is going to require some very careful strategic moves and Coles is probably better placed than Woolworths, which also has to revamp its supermarkets and extract itself from the Masters mess. These are diversions you do not need when life becomes more difficult.

Returning to the need for directors to get out there and see exactly what is going on in their operations, we saw this week that the Vale-BHP owned Samarco tailings dam had encountered cracks and leaks well before the actual dam burst. It would seem that these early cracks and leakages were not known by BHP. Had they, BHP, gone to the site and mixed with the engineers on the tailings dam site they would have realised that it was dangerous and that expanding the dam had an extra dimension of risk. Directors all too often rely on what the CEO tells them. It is OneTel all over again.

Rate guessing games

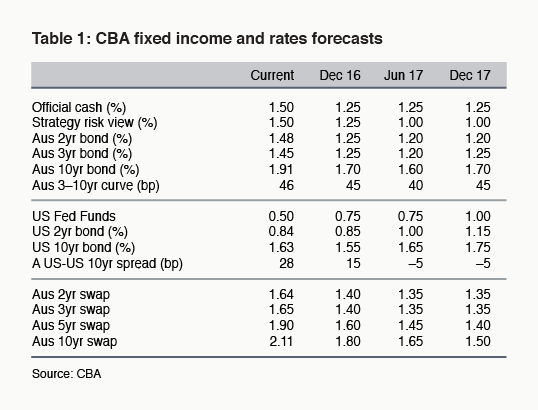

Right now the global share and bond markets are interest-rate guessing games. What caught my attention this week was a table put out by the Commonwealth Bank showing how it forecasts interest rates in Australia and the US over the next 15 months or so.

The bank will of course get it wrong but as you can see from the table below it is a useful guide to what might be ahead.

The bank expects one Australian interest-rate cut in the next 15 months, in December. Conversely, it expects two rate rises in the US over the next 15 months. Despite those US increases it expects the American 10-year bond rate to only edge up to 1.75 per cent by December 2017. That's not a big rise. The bank clearly expects money seeking safety to pour into American bonds.

The Australian 10-year bond rate is expected to fall from 1.9 per cent to 1.7 per cent over the 15-month period, which would actually make it lower than the US 10-year bond rate at that time, if the CBA is right. It means that the interest rate increases in the US will be restrained and our rates have further to fall. This is not a scenario for a high growth world. Indeed, the bank has put out a chart which shows that the consumer price index, nominal GDP, the Reserve Bank cash rate and the 10-year bond yield have all been headed in the same direction since 1955. The sharemarket is priced on the basis that there will be yield available from shares which is much higher than that available in debt securities given the continued fall of Australian interest rates.

_1.png)

There is not a lot of growth in major companies and if any corporation stumbles it is hammered in the market. UBS says that global markets are not pricing in a sufficient risk factor in fixing the value of shares, and they are fearful that global markets may fall 20 per cent as markets adjust to risk.

Australian superannuation portfolios are much more concentrated in equities than their counterparts overseas. That means we need the sharemarket to perform and not have a big setback – i.e. UBS to be wrong.

Make sure your long-term portfolio has an interest bearing securities component and is not totally dependent on equities.

Superannuation shortfall

Finally, here at Eureka we have been alerting people for many weeks that the proposed superannuation rules would prevent people gaining enough savings via superannuation to avoid the aged pension. While you might save a few dollars in immediate government income gains, longer term it will be very costly for Australia and it will swing a lot of capital into the housing market via upgrades of existing family homes and in negative gearing.

This is not good for overall productivity or for first-home buyers. But the current government simply did not understand that when they first announced the superannuation package and now that they do they don't have the courage to amend it. Malcolm Turnbull became Prime Minister thanks to the Victorian Government's CFA-volunteer bashing. I don't think Australians will forget what he and Scott Morrison did to their superannuation when the next election comes around.

Click here to read this week's Eureka Weekly Review PDF.

Readings & Viewings

US fund manager Vanguard started the low cost, index fund revolution in 1974, saving investors about $US1 trillion.

It's no secret that Uber, the world's biggest virtual taxi company, has been going places for a long time. The app-based business is worth a massive $US69 billion now, but who's in the driver's seat? Here's Uber's team of corporate chauffeurs.

Speaking of taxis, or taxi drivers, here's an ‘oldie but a goodie' video from the BBC that shows anyone can be an expert. (Here's a different camera view). It will make you think, the next time you watch a media interview.

Meanwhile, the US Securities and Exchange Commission has been busily rounding up suspects at the chemicals giant Monsanto. This week it awarded $US22 million to a former executive turned whistleblower.

Now, the Scots are known for being frugal with their money. But, hoots, the number of millionaires in the Highlands is falling, according to a Barclays report this week.

But don't worry – Scottish scientists have now discovered a way of extracting gold from mobile phones. With the gold price potentially heading higher, used phones could be an investment option.

As far as online bank heists go, the one that's just hit Bangladesh Bank is a doozy. Hackers using the SWIFT messaging system have stolen $US81m, but were close to getting $US1bn before a typo gave them away.

While the UK property market has taken a hit since the Brexit vote, the Bank of England's chief economist reckons real estate is better than a pension when it comes to generating long-term retirement income.

Dollar Shave Club, an online men's razor vendor, has just been purchased by Unilever for $US1bn. Their early success was in no small part due to this expletive-laden but amusing video.

Mitchell Sneddon's recipe of the week: “This one is a little hooter. It's easy as and as one of the comments says, ‘it's broccoli crack'. Just go a little easier on the oil than suggested.”

Lastly, it's not strictly business, but it's definitely show business. We leave you with a short video obituary of actor Gene Wilder, who died this week aged 83.

Last Week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

While Japanese shares rose solidly over the last week helped by talk of more monetary easing and a fall in the yen, US, eurozone and Chinese shares were little changed partly constrained by nervousness ahead of the release of potentially Fed moving August jobs data in the US along with falling prices and Australian shares fell. Bond yields were little changed in the US and Australia but rose in the UK and peripheral Europe. While a rising US dollar weighed on commodity prices, the Australian dollar was little changed.

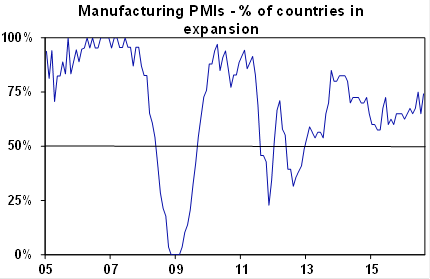

Global manufacturing conditions PMIs slipped a bit in August, but remain consistent with ongoing moderate global growth. While there were significant falls in the US and Australia, India and the UK saw good gains and nearly 75 per cent of countries have PMIs in so called expansion territory (i.e. above 50). The bottom line is that the global economy continues to muddle along.

Source: Bloomberg, AMP Capital

Source: Bloomberg, AMP Capital

Surprise surprise, Brazilian President Dilma Rousseff was impeached! Seven years ago when on holidays in Rio the day it was announced that Brazil would host the 2016 Olympics I was interviewed by Brazilian TV at the base of the Sugar Loaf cable car and managed to say "parabens Brasil" (maybe they liked my Hawaiian shirt). Since then it seems to have been downhill for Brazil! And the impeachment of Rousseff doesn't necessarily improve things. There are some signs that their recession is easing and a stabilisation in commodity prices will help. But former vice-president and now president until 2018 Michel Temer has his own problems which may deepen as austerity designed to control the budget deficit blow out kicks in and Brazil really needs a radical long term reform agenda to get back on track.

The final days of the Australian June half profit reporting season offered nothing new. Funny the way most companies with good results report early, but Harvey Norman invariably comes in with good news on the last day. The basic picture remains one of a tough 2015-16 with earnings down 8 per cent led by resources and aggregate dividends down about 10 per cent led again by resources (only a fruit cake could have believed that the super high resources dividends were sustainable). However, the median company did okay with earnings up 5 per cent or so, 62 per cent of companies seeing earnings up year on year, 86 per cent of companies raising or maintaining dividends and 54 per cent of companies seeing their share price outperform the market on release day. Overall, the results are consistent with a return to earnings growth of about 8 per cent this financial year.

Major global economic events and implications

US economic data was mostly good with solid consumer spending in July and a surge in consumer confidence in August adding to evidence that the consumer is in good shape, solid labour market indicators, solid construction activity, a stronger than expected rise in pending home sales and continued modest growth in home prices. Against this though manufacturing conditions softened according to the August ISM index which fell to 49.4 from 52.6. While the broader Markit PMI index held up better at 52, the fall in the ISM should at least give the Fed pause for thought at its September meeting and supports the case to wait till December before moving on rates again. Meanwhile the Fed's preferred inflation gauge – the core private consumption deflator – was stable at 1.6 per cent year on year where it's been for months indicating that upwards pressure on inflation remains weak.

Eurozone economic confidence fell slightly in August but remains at levels consistent with ongoing moderate economic growth. Meanwhile unemployment remained at 10.1 per cent in July (at least it's down from 12.1 per cent a few years ago) and core CPI inflation in August fell to 0.8 per cent year on year from 0.9 per cent indicating leaving it well below the ECB's 2 per cent target.

Japanese economic data was good (believe it or not). Unemployment fell to just 3 per cent, the jobs to applicants ratio remained at its lowest level since the early 1990s, real household spending and retail sales rose more than expected and housing starts are up nearly 9 per cent year-on-year (yoy). Against this though industrial production was soft and small business optimism fell.

While Chinese consumer confidence fell in August, business conditions PMIs were indicative of stable growth. The official manufacturing PMI rose to 50.4 (from 49.9), the non-manufacturing PMI fell but to a solid 53.5 (from 53.9) and the Caixin manufacturing PMI fell to 50 (from 50.6). Lots of noise but basically consistent with GDP growth stabilising around or slightly above 6.5 per cent.

Indian GDP growth slowed to 7.1 per cent yoy in the June quarter (from 7.9 per cent) on slower growth in investment and consumer spending. That said its way above virtually any other country including China and India's manufacturing PMI rose to a 13-month high. At least one of the BRICs is actually better than it used to be!

Australian economic events and implications

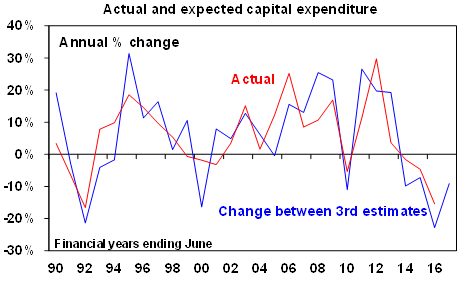

- Australian economic data was all over the place. Retail sales were flat in July adding to the loss of momentum here (which partly owes to weak price inflation but weakness in household goods looks odd given strong dwelling completions) and business investment fell again in the June quarter. However, the fall in capex was driven by buildings and structures and was consistent with the mining driven engineering construction slump already reported in June quarter construction data. Against this plant and equipment investment actually rose in the June quarter and investment plans for the current financial year improved more than expected suggesting that non-mining investment may be stabilising. Although mining investment looks like falling another 27 per cent this financial year, at 3 per cent of GDP now its negative impact on overall economic growth is starting to wane given that it has already fallen from around 7 per cent of GDP. The next chart shows that there has been a loss of downwards momentum when comparing expected capex plans for the year ahead.

Source: ABS, AMP Capital

- Meanwhile on the housing front, building approvals surged back to near record highs in July led by another spike in apartment projects and house price growth according to CoreLogic remains uncomfortably high in Sydney and Melbourne despite slowing rents and record low rental yields. That said, July new home sales resumed their downtrend according to the HIA in July, housing credit growth continued to lose momentum (led by investor finance) and I suspect that many of the apartment approvals won't proceed to construction given the emerging oversupply and weakening conditions in the apartment market in several cities. Nevertheless the case for more APRA intervention in the face of still too hot Sydney and Melbourne property markets remains.

Shane Oliver is head of investment strategy and chief economist at AMP Capital.

Next Week

Savanth Sebastian, CommSec

Data deluge: Economic growth in focus

After the tsunami of economic data over the past week, another round of top-tier economic indicators is expected in the coming week. In fact, at least another eight economic indicators are due for release in Australia, with a Reserve Bank board meeting also thrown in for good measure. In the US, the data releases will be more of a ‘second-tier' nature. And in China key economic figures will be released on Monday, Thursday and Friday covering services, trade and inflation.

The week kicks off on Monday with a raft of indicators. The Australian Bureau of Statistics (ABS) releases the Business Indicators publication covering profits, sales, stocks and wages. The Melbourne Institute releases the inflation gauge and ANZ issues the job advertisements series.

Job ads have less relevance as a leading employment indicator – given that more jobs are now posted on individual company websites and social media such as LinkedIn, Facebook and even Twitter. But the job ads data is still important in watching for turning points. The monthly inflation reading should continue to show that price pressures are subdued.

On Tuesday the ABS issues the Balance of Payments figures – quarterly reading on goods and services trade. In addition the weekly consumer confidence survey is issued by ANZ and Roy Morgan.

Also on Tuesday, the Reserve Bank Board meets to decide interest rate settings. But barring a complete surprise, no change in rate settings is likely. The statement accompanying the decision could be short, although there is scope for a few words on global central bank policy and the stubbornly high Australian dollar.

On Wednesday, the ABS issues the quarterly economic growth estimates in the National Accounts publication. At this early stage we are tipping growth of around 0.3 per cent in the quarter and 3.1 per cent growth for the year.

On Thursday, the ABS releases trade data (exports and imports) for July. We expect the trade deficit probably remained significant although it is likely to have narrowed from $3.2 billion in June to near $2.1bn in July.

Also on Thursday, Reserve Bank Deputy Governor, Philip Lowe, delivers introductory remarks at an International Conference, organised by the Asian Development Bank in collaboration with the Institute of Global Finance.

And on Friday, the ABS releases the July publication of Overseas Arrivals & Departures. The publication includes tourist movements as well as migration flows. China is well and truly now our largest source of tourists, with tourist numbers growing at a pace of over 20 per cent per annum.

Also on Friday, the July housing finance data is released – the data on new home loans. Based on figures from the Bankers Association we expect that the number of loans for owner-occupiers (people who are buying homes to live in them) rose by 2 per cent. In June the number of new owner-occupier housing loans (commitments) rose by 1.2 per cent. No doubt the interest rate cuts will continue to support home building.

Overseas: Chinese data to dominate attention

There are sparse helpings of ‘top shelf' US economic data in the coming week with the main interest likely to be the Federal Reserve Beige Book on Wednesday. Also Chinese trade and inflation data is issued during the week.

The week kicks off on Monday with the release of the Caixin China services sector index. Encouragingly the sector continues to show a modest expansion.

On Tuesday, the focus shifts to the US, where the ISM services index is released. In addition San Francisco Federal Reserve President John Williams is set to deliver a speak on the economic outlook. And while Williams does not have a vote on Fed policy, investors will pay particular attention to the speech. This is especially the case given that Williams has a longstanding relationship with Fed Chair Yellen and he recently signalled that waiting too long to hike rates could be costly.

On Wednesday, the Federal Reserve releases its Beige Book – a summary of economic conditions across 12 Federal Reserve districts. This survey of economic conditions well be a key input to the decision making at the September 21-22 Federal Reserve meeting. The JOLTS job openings index is also released on Wednesday together with the regular weekly figures on housing finance.

On Thursday, the focus shifts to the Chinese trade (exports and imports) figures for August. The trade surplus is significant at present at $US52.3bn, suggesting there are still healthy global markets for Chinese goods. At the same time imports continue to slow.

Also on Thursday, the weekly data on claims for unemployment insurance (jobless claims) is issued together with consumer credit figures for July. Analysts expect a lift in consumer credit from $US12.3 billion to $US15bn.

On Friday, the monthly US wholesale sales and inventories figures are released. Meanwhile in China, the National Bureau of Statistics issues inflation figures – the data on producer and consumer prices. Producer prices are still in decline, down 1.7 per cent over the year. And consumer prices are rising at a modest 1.8 per cent annual rate. Further tame inflation readings would leave the door open to another round of stimulatory measures.

Sharemarket, interest rates, currencies and commodities

The profit-reporting or earnings season is done and dusted. and CommSec has analysed all results from the 139 ASX200 companies reporting earnings for the full-year to June.

If all companies are included, aggregate earnings were down by 16.8 per cent. But there is the small matter of BHP Billiton that reported a loss of $US6.4bn. That result distorts the true picture. That is shown by the fact that almost 90 per cent of companies reported annual profits. If you strip out BHP Billiton, aggregate earnings were up by 6.8 per cent.

Aggregate cash levels haven't budged much from the last reporting period in December. But it is clear that companies are enthusiastic as they have ever been in paying out dividends. In fact an amazing 92 per cent of companies announced a final dividend for the year to June.

Savanth Sebastian is an economist at CommSec.