Why the Fed won't rush to raise rates

The US is creating jobs at its fastest pace since Bill Clinton was in office. But with oil prices collapsing and the US dollar shifting higher, there is good reason to believe that the Federal Reserve will take a cautious approach to policy normalisation.

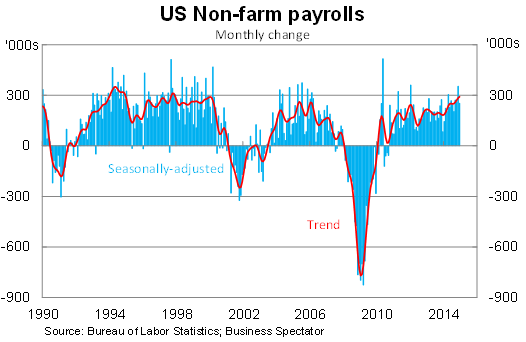

Non-farm payrolls rose by 252,000 in December, beating market expectations, to complete the strongest year for job creation since 1999. Payrolls were revised up in both November (up 353,000 compared with an earlier estimate of 321,000 and October (up 261,000 compared with 243,000).

The monthly trend is now rising at its fastest pace since November 1997. Over the past twelve months, the US economy has experienced a net increase of 2.95 million jobs. Non-farm payrolls are now 1.98 million above their pre-crisis peak.

Private non-farm payrolls rose by 240,000 in December, while government payrolls climbed by 12,000. State and local governments drove the rise in public sector jobs.

Local government payrolls climbed 87,000 during 2014; state government payrolls by 21,000; while federal government payrolls fell by 17,000. Government payrolls -- at all levels -- remain well below their peaks. In fact, federal government employment is at around its lowest level since 1966.

That should begin to change now that there is less pressure on the Obama administration to cut government spending. Federal payrolls should begin to pick up modestly in the remaining months of Barack Obama's presidency.

The services sector continues to be the engine behind the recovery, gaining a further 185,000 jobs in December. Over the past, year, the services industry has account for almost 85 per cent of total job growth.

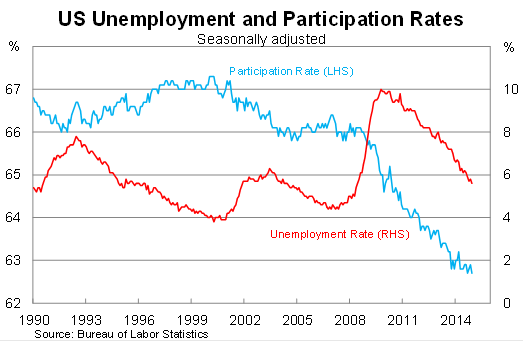

As a consequence of strong job growth, the unemployment rate fell to 5.6 per cent in December and is down by 1.1 percentage points over the past year. An important part of the narrative is that during that time, the unemployment rate was not driven down by the participation rate, which has remained broadly unchanged over the year.

Nevertheless, it is widely anticipated that the participation rate will decline further over the next decade. That's the nature of unfavourable demographics but there may be a short-term boost as strong employment numbers drag the long-term unemployed -- who may have stopped looking and are therefore no longer counted among the unemployed -- back into the market.

The recent run of strong employment numbers has some important implications. Obviously it brings an interest rate hike and policy normalisation closer. But there is still considerable uncertainty surrounding the timing of a rate hike.

Most of the major labour market indicators -- and the broader economic indicators -- point towards the need for policy normalisation. Except one.

Inflation remains surprising benign given the developments across the broader economy. The recent collapse in the oil price -- which presents a deflationary risk for Europe and will ease inflation in the US -- will surely keep inflation contained in the near term.

The net impact of a lower oil price should be positive -- a point recently noted by the Federal Reserve in their minutes. But it will also have a disruptive effect on certain sectors of the US economy; however, the boost to household incomes and the jobs created through retail and other spending should be sufficient to support the US economy through a volatile period.

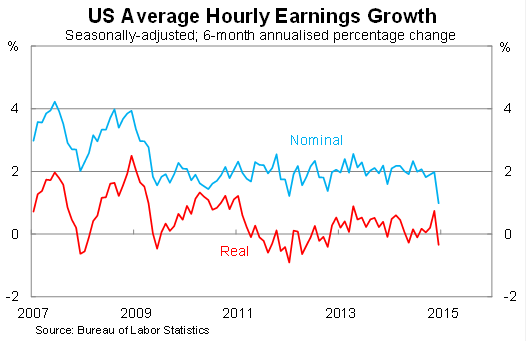

For mine, the most important labour market indicator in the next three-to-six months will be the average hourly wages. This will show the extent to which job creation is absorbing spare capacity and that will directly affect the domestic component of inflation.

Average hourly earnings collapsed in December -- it's not clear why -- but I expect that with hindsight we will view this months' outcome as a statistically quirk rather than a meaningful development. Strong jobs growth and softer wages are consistent in the presence of compositional change but such a sharp movement during normal times appears highly unlikely.

Oil prices and a higher exchange rate will weigh on inflation but stronger and more persistent wage growth should be sufficient for a forward-looking central back to begin the process of policy normalisation.

In previous articles I have argued that an unemployment rate of 5.5 per cent might be sufficient to get the Federal Reserve moving. Following a period of financial market volatility, I think the Fed will be more conservative than that, particularly if an unemployment rate of that nature if reached in the next month or two.

Regardless of how the timing unfolds, it is fair to say that the Fed will take a slow and cautious approach. Even if policy normalisation begins in the first half of this year, it is unlikely that the Fed will raise rates more than a few times, particularly with inflation remaining well contained.