Why the ASX has further to run

Summary: Australian shares have put on a magnificent run so far this year, with the All Ordinaries lifting seven per cent to reach its highest levels in almost seven years. In some respects, this rally is best viewed as a catch up, given the market's muted performance in 2014 in the face of falling commodity prices, a slump in the Australian dollar and regulatory threats to our banks. That none of these headwinds have actually dissipated this year – in some ways they've become worse – highlights how sentiment has been the main problem. |

Key take-out: The outlook for Australian equities is uncertain in the short term, with policy ineptitude continuing to help create a crisis in sentiment. However, in the current bond environment shares remain comparatively cheap – providing a strong reason for the rally to continue in the longer term. |

Key beneficiaries: General investors. Category: Economics and Investment Strategy. |

Aussie equities have put on a remarkable performance this year. At the time of writing, the All Ords was up seven per cent for the year so far to be at its highest level in nearly seven years. That's a move that outperforms even US stocks – and it's not too far behind those in Europe either.

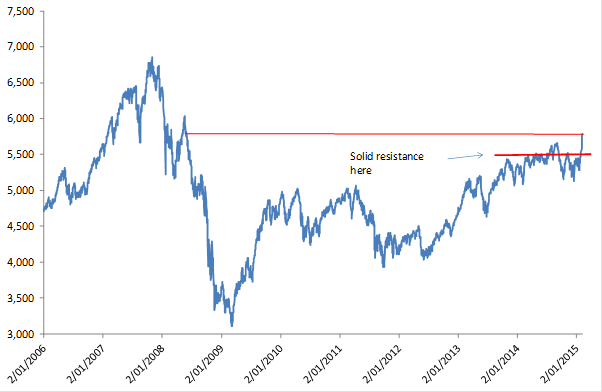

It's a great effort. To give you a sense of how good it is, for the S&P/ASX 200 it's the best run on record, not necessarily in terms of magnitude, but certainly in length. For the All Ords it's the best run since the mid-1980s, with the index has crashing through a fairly strong level of resistance around the 5500 mark.

Chart 1: All Ords at a 7 year high

In some respects the current rally is best viewed as a bit of catch up. The market ended 2014 having done little – up maybe one per cent when some of the US indexes had put on double digits. Yet, as I argued at the time, there was little to justify that performance. Australian stocks simply fell out of fashion, driven by:

- The commodity rout, which affected sentiment for the whole market;

- The slump in the Aussie dollar;

- Excessive threats of regulation against our large banks.

As you know none of these have dissipated – in fact in some ways they've become worse. So it's telling that the All Ords has staged such a strong rally when the notional causes of the previous rout are still there. Even BHP has managed to rally hard – perhaps on the view that the sell-off was overdone.

All this highlights my point last year that sentiment was the main problem and that at some point it would rebound and, with it, the Aussie market.

Now I can't sit here, hand on heart, and say this rally will continue. Nor can I say that it will fade though. Volatility is extreme and fashion and whim still dictate the market – at least in the short term. It is a hard run though and it would be remarkable if it continued at this pace with the sentiment headwinds our market has to endure.

It's not that such outcomes are without precedent. Indeed such price action is usually a very good omen for further prices gains over the year – and you've really got to go back to 1987 to have been misled by such a strong start to the year. That is, very strong rallies early in the year tend to be followed by a stronger market for the year as a whole – sizeably so, in many cases.

Moreover, as we go into 2015, this pricing action is backed by some very strong fundamentals. Jobs growth in Australia has strengthened considerably, credit growth is picking up and global growth itself remains solid.

What is different this time is this sentiment crisis, which is driven, in my view, by policy ineptitude – all of which makes the market prone to bouts of nerves. In previous episodes where the market has rallied strongly, sentiment hasn't been so poor.

Through it all and however we track into 2015, what investors need to keep in mind is that with little change in the economic or even earnings backdrop, this rally shows is there is an appetite for Aussie stocks.

Always keep that in mind, because the market may well pull back over the ensuing months. We don't really have a precedent to this price action under these conditions. But, if it does, we know such a pull-back presents a good time to buy. There is no sign the bull market is over yet.

A big reason for this is because, even with the All Ords at a seven-year high, Australian stocks are cheap – extremely cheap on some metrics. The price-earnings (PE) ratio on a trailing basis is 21.9 on Bloomberg figures. This is below the average of 23 and well down on cycle peaks. Using next year's earnings forecasts, the PE ratio drops to about 16.8!

Naturally, investing is relative and compared to cash or bonds the attractiveness of equities becomes even more crystal clear.

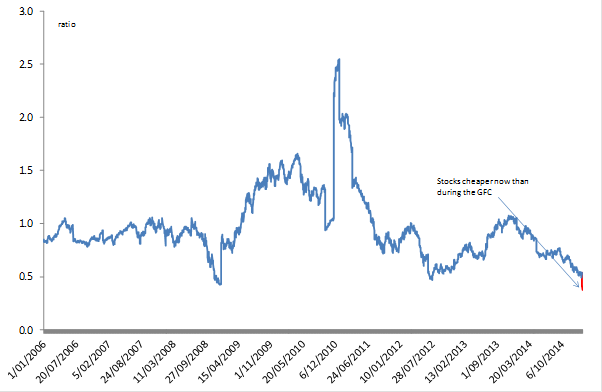

Chart 2 compares the earnings yield from the All Ords to the yield on the 10-year Australian government bond. There are various ways people can show this relationship – in the chart below I've just used the ratio of bond yield to earnings yield. That means that the higher the ratio, the less attractive equities are to bonds. The lower the ratio, the more attractive equities become.

Chart 2: Aussie stocks appear cheap compared to bond yields

What the chart shows is that equities are actually cheaper now than in the aftermath of the GFC and during the European debt crisis/US fiscal cliff saga. That's an incredible development and something at odds with the economic and earnings backdrop (which remain robust).

The comparative cheapness of the market is a very strong reason for the equity rally to continue. Indeed, it's worth noting that the surge in the market so far this year has been driven largely by yield stocks – the banks and Telstra. They've accounted for just over half the lift in the All Ords over the last month or so, which compares to their weight in the index of about 30 per cent.

While share prices have risen materially so far this year, these gains in most cases can only be justified if we assume current bond rates are sustainable through the cycle (see Simon Dumaresq and James Hannam's article in today's edition).

So have Aussie equities done their dash? In the short-term – who knows? As I've outlined before, I think it's going to be a very difficult year for sentiment. Longer term I think it's very unlikely that equities will trend lower (on a 12-to-18-month view).

What is clearer at this point is that the underlying pressure for stocks to push higher is strong – and the market will continue do so in the absence some serious sentiment headwinds.