Why bad news in China is good news for Australia.

Summary: Chinese shares are falling again, but the market is largely a state-run affair. We don't know when the stock market rout will end, but what matters more to Australian investors is the policy response from the Chinese authorities. The People's Bank of China will continue to cut rates and questions are even being raised as to whether a QE program is in store. |

Key take-out: The Chinese equity rout is positive for Australian equities, as we live in a world where quantitative easing is viewed positively. |

Key beneficiaries: General investors. Category: Economy. |

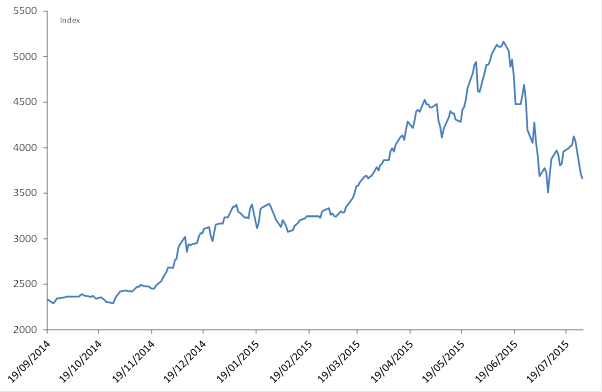

After a brief respite, where the Shanghai composite rebounded 16 per cent off the low, it looks like the market is once again getting hammered. Over the last three sessions, Shanghai stocks have slumped 11 per cent – 8½ per cent of that just on Monday, which is the biggest single drop since 2007.

Chart 1: Shanghai Composite getting smashed

To date then, Chinese equities are down 30 per cent in Shanghai, although that still leaves the market some 60 per cent higher over the last nine months.

The big question? What's the end game – where (and when) does the market hit a bottom? At the outset, no-one knows. Just as there was no real basis for the 150 per cent spike that we saw, there is no real basis for this slump. Indeed relative to historical price to earnings ratios, the Shanghai composite is still currently very cheap – trading at a substantial discount to average multiples.

Unfortunately, there's probably not too much we can garner from the technicals either. Notionally there is a bit of support at current levels, with another support level 10 per cent lower. The problem is price discovery though.

The fact is China's market is still comparatively opaque. By and large the ‘market' is a state-run affair. Yes, western media is full of articles on China's current rout – all of which invariably quote some equity mad citizen who quit their job to trade full time. The reality though, is that household participation in the stock market is low. Most estimates suggest around 8-9 per cent of the population are equity investors. This compares to the US at around 50 per cent and Australia at around 40 per cent.

So while the media try to make out that equity trading in China is this widespread cultural pastime, driven by margin financing for a household sector that is already highly indebted, this isn't true. The largest participants in the Chinese stock market are – by far – state-owned enterprises and the very rich. Pension funds, fund managers and finance corporations etc. Nearly all of the largest institutional participants are owned by the government. Indeed most of the companies listed, certainly the larger ones, are still state owned as well (90 per cent or more usually).

Which means that in effect, the Chinese stock market consists of companies that are state owned, bought and sold by companies that are state owned.

That's why this whole scenario is so bizarre – and why we simply do not know when the stock market rout will end. It's hard to explain why it's so difficult for state-owned companies to encourage other state-owned companies to buy their stock. As I've discussed before though, it probably doesn't really matter for the medium-long term outlook. Especially given the market is driven by the state on both the demand and supply side.

What does matter much more to Australia and domestic investors is the policy response taken by the Chinese authorities. This is the end game that really matters.

So far, the cumulative effect of announced policy changes appears to have been limited, as the ongoing slump attests. Think about the measures taken: the large state-owned fund managers have had a ban on selling put in place for the next six months, a market stabilisation fund has been established, trading halts have been issued and the People's Bank of China has cut rates. All seemingly for nothing as the market is only about 4 per cent off the low.

That's not what is important though. What's important is that the government that will take increasingly aggressive measures to shore up the market – and this is the end game. More stimulus.

Indeed the fact that measures to date haven't been particularly successful ensures only one thing. That more will be taken. Which means that in a low inflation environment, the People's Bank of China will continue to cut rates. They've already done it about four times so far over last year – most recently on June 27. With a key lending rate of 4.85 per cent, the PBOC's key lending rate is still high and they've got plenty of ammunition.

Questions are even being raised by global investors as to whether a Chinese quantitative easing program is in store. Western analysts like to berate China for the rapid pace of debt growth. To the extent that is true though – and if all the concerns about China having a debt bubble are accurate – then surely the logical response is for the PBOC to print money.

After all, debt monetisation programs are being used in Japan, America, Europe and Britain. Oh, and Zimbabwe. For Chinese policy makers, it must be a huge temptation to deal with their mounting debt in the same fashion as their peers. Print it away.

Some economists already think that the Chinese have engaged QE, well a more modest version, following a debt swap with local government agencies that converted short-term loans to longer term bonds (at lower cost).

While that's not technically QE, it does point to a government that is keen to reduce the nation's debt burden, if only to eliminate the perception that it's a problem. Similarly, the Bank of Japan already uses its QE program to buy equities, so it wouldn't be a unique or shocking proposal if the Chinese opted to do the same.

In a perverse way then, this Chinese equity rout is a positive development for Australia and Australian equities. It may not seem like that but think about the world we live in. We live in a world where quantitative easing is viewed positively. I think that's crazy but this is current thinking. Noting that the real economic effects of the equity rout will be zero (given that the government is the dominant player) that leaves only three things – lower national debt, more money to invest and more positive sentiment toward China.