Topsy-turvy world

The markets fell in the second week of November after a quiet start to the month. The main reason appears to have been some unexpectedly positive news about the US economy – go figure! In fact this has become a common theme in markets in recent months, and there is some logic to this behaviour.

The US Federal Reserve really wants to raise interest rates as they are starting to feel uncomfortable, with rates having been at 0.25% since the beginning of 2009. Apart from anything else (and there are a few other things) wouldn’t it be good to be able to lower rates again if something else bad happens?

Asset prices around the world have benefited from such low rates in the world’s most important market since the GFC and so it stands to reason that even the thought of slightly higher rates is going to make markets rethink if strong post-GFC gains that portfolios have benefitted from so far are going to continue.

If you think about it, you probably feel the same way about buying a house – if you think interest rates are going to be really low you could afford to spend more on a house but if you think you’re future interest rate payments are going to get bigger you might not be ready to borrow so much. This thought process is being repeated all around the world on a grand scale. So there you have it - we now live in a strange world where good news (for the economy) is bad news (for investors).

And of course when there was some more economic bad news from Europe, China and South America in the middle of the month - so markets breathed a sigh of relief, thinking maybe that rate rise might get put off a bit, and we ended up where we started the month.

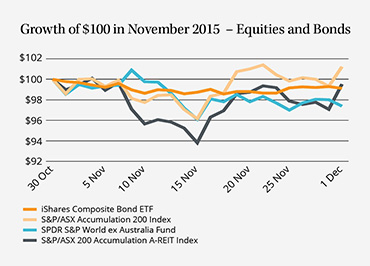

The Paris attacks didn’t really affect markets as so far there has been little indication that they might affect either interest rates or global growth. The following chart shows how the principle underlying assets in our diversified portfolios performed during the month.

As you can see the interest rate sensitive Australian Property Trusts (A-REITs) performed the worst in the second week of November and bonds didn’t help much either.

Bonds are often relied upon to perform well and provide diversification when equities struggle (they normally do best when economies are weak and interest rates are falling). So you can see why property and bonds might not be so useful if interest rates can’t fall much more. Which is why our portfolios don’t hold much of either.

So why still hold equities if they too are going to struggle if interest rates rise?

Firstly, current dividend yields and expected growth of those dividends mean that over the longer term we expect returns to be much better than cash (even if interest rates go up). However, you might have to wait awhile to see those underlying earnings come through and in the meantime markets will continue to worry about interest rates.

Secondly, we don’t really know what is going to happen next or what central banks will do, so it is not a foregone conclusion that equity markets will fall in the near future. Rather than trying to guess what is going to happen to equity markets around the world, it is much better to have a thoughtful allocation of your portfolio across multiple asset classes and geographic regions. Just because US equity markets drop does not mean Europe drops.

Different investors have different investment goals and our current opinion is that conservative investors need to hold a bit more cash (compared to fixed income) and more risk tolerant investors can afford to hold more equities (especially compared to property trusts) if they can put up with the short-term volatility. That is how our diversified portfolios are currently positioned for now and we’ll let you know if our view changes.

Next week we will go into a bit more detail about what sort of returns you should expect from each asset class in the future.

Frequently Asked Questions about this Article…

The markets fell in the second week of November due to unexpectedly positive news about the US economy, which led to concerns about potential interest rate hikes by the US Federal Reserve.

Interest rates impact asset prices because low rates have historically benefited asset prices since the GFC. When rates are low, investors are more willing to invest, but the prospect of rising rates can lead to market re-evaluation and potential declines.

Good economic news can be bad for investors because it may lead to interest rate hikes. Higher rates can increase borrowing costs and reduce the attractiveness of investments, causing market volatility.

The Paris attacks did not significantly affect the markets as there was little indication that they would impact interest rates or global economic growth.

Australian Property Trusts performed poorly in November because they are sensitive to interest rate changes, and the prospect of rising rates negatively impacted their performance.

Yes, investors should still consider holding equities because current dividend yields and expected growth suggest better long-term returns compared to cash, even if interest rates rise.

Conservative investors are advised to hold more cash compared to fixed income, as this provides a safer option amidst potential interest rate hikes and market volatility.

Risk-tolerant investors can afford to hold more equities compared to property trusts, as they can handle short-term volatility and potentially benefit from long-term growth.