The worst is over

Summary: The recent correction in the US share market was necessary – I believe it was neither the beginning of a bear market nor a signal of a coming recession. The US, Europe and Japan are in a prolonged period of slow growth, meaning a favourable environment for stock prices could continue for several years. Meanwhile in the Middle East, residents are troubled by the rise of ISIS, but more concerned about the oil price and the direction of the financial markets. |

Key take out: Although there may be further market declines, I believe the worst is over. One poll of sentiment is setting the stage for a rise in the market through year-end. |

Key beneficiaries: General Investors. Category: Economy. |

All through the summer the United States equity market made new highs in spite of increasing turbulence around the world. The economy was continuing to grow modestly, earnings were coming through and the geopolitical problems were a long way away. The Ned Davis Crowd Sentiment Poll, which includes transactional data like the put-call ratio, showed that investor mood was very optimistic. Historically, the market is vulnerable to a correction when optimism is extreme. You don't know what will cause the sell-off, but you have the uneasy feeling it's coming. The market had gone through two years without so much as a 10% correction and we were due for one.

Identifying the precipitating event is hard and probably unimportant. A few of the geopolitical problems had actually cooled somewhat, albeit temporarily. Russian troops had pulled back from the Ukraine border; there was a cease-fire in the Israel/Gaza conflict; the Iran nuclear talks weren't making much progress, but they were continuing; and in the South China Sea issues had quieted down for a while. However, the situation in Syria and Iraq, which had been invaded by the Islamic State of Iraq and Syria (ISIS), remained serious. The two threats that may have unsettled investors were the possibilities that the Ebola virus might spread to Europe and the United States and that the economic slowdown in Germany might abort Europe's weak recovery and bring the continent back into recession.

The decline in stocks gained intensity as it moved along, with many days down 1% or more on the Standard & Poor's 500. Rallies gave way to further declines and eventually the market fell almost 10% before prices stabilised. The correction did pound some of the optimism out of investors' minds. The Crowd Sentiment Poll dropped from optimistic into pessimistic territory, setting the stage for a rise in the market through year-end. There may be further declines, but in my opinion the worst is over. I believe that this was a necessary correction and not the beginning of a bear market.

Sometimes, the market is smarter than all of us participating investors and a sharp downturn precedes a recession by about seven months. I do not think that was the outcome signaled by the September/October correction. The US economy is actually doing quite well. Real growth is expected to be approaching 3% in the second half of 2014 and growth of 2.5% to 3% is expected to continue into 2015. The economy usually provides some warning signals before a recession occurs. According to an Omega Advisors study, danger is signaled when the yield curve is inverted, unemployment claims are rising, personal income is down, consumer confidence is falling, industrial production is declining, and/or inventories are increasing. Virtually none of these indicators are giving a warning signal now. There have been some notable earnings disappointments (including IBM, Amazon, AT&T, McDonald's and Coca-Cola), but Apple, Caterpillar, Microsoft and others did well. More worrisome is the shortfall in revenue growth, and because margins are no longer increasing, net profits have only improved modestly. Companies have continued their share buyback programs, however, and this has played an important role in earnings per share growth. That is expected to continue.

I believe we are in a prolonged period of slow growth in the United States, Europe and Japan. As a result I think a favourable environment for stock prices could continue for several more years. In my mind, valuations are not excessive and equities can appreciate in price in accordance with earnings increases. I do not expect much in the way of multiple expansion, except perhaps at the end of the cycle when everyone becomes comfortable that the good times are going to last forever and nothing is ever going to go wrong. That's when the “animal spirits” take over.

During the decline, there was wide suspicion that the end of Federal Reserve monetary accommodation in October had something to do with it. The balance sheet of the Fed was $US1 trillion in 2008. It is over $US4 trillion now. There is general agreement that easy money was a factor in the rise in the stock market over the past five years as well as the low level of interest rates. Accordingly, the end of the tapering process was pointed to as one of the causes of the decline. In addition, there was continued speculation about when the Fed was likely to start raising interest rates. The consensus had been that the first rate rise would occur in the middle of 2015, but the recent decline in the stock market, along with low inflation, some soft economic data and continuing high unemployment, has caused many analysts to think the Fed may act later rather than sooner. My view is that there is little reason for the Fed to raise rates anytime soon, and when they do finally act, they will do so very gradually. A Fed increase in rates has been so well advertised that it may not have the deleterious impact everyone seems to fear. In the period 1950–1980, an eccentric market analyst, Edson Gould, developed the “three steps and stumble” rule. This was based on the observation that it took three increases in Fed rates before the market impact became severe. A study by Omega Advisors showed that on average the market does not decline significantly until 29 months after the first rate hike.

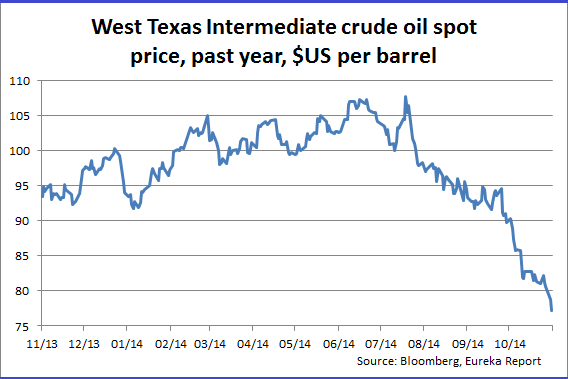

In October, I spent a week in the Middle East to visit clients and get some feeling for the mood there. It was not cool in terms of temperature – in the high 90s (Fahrenheit) minimum every day – but there was no sound of artillery in Qatar, Saudi Arabia, Dubai or Abu Dhabi. I would like to say there is a consensus on Israel/Gaza or Syria/ISIS/Iraq, but there is not. I did observe that the conflicts in the region are not a part of everyone's daily conversation in the places I visited. Most of those living there are focused on economic opportunity, and the price of oil is more important to them than the fighting in the western part of the region.

A range of opinion exists on what price is necessary for Saudi Arabia and others to finance their domestic activities. Some believe $US80 will do it and there are estimates as high as $US110. Oil is priced in US dollars and the strength of the American currency has obviously increased its purchasing power. The prevailing view is that the price of oil is generally influenced by cyclical factors. Since the economies of the United States, Europe and China are slowing, you would expect weaker demand to be reflected in the oil price. North America is also becoming more energy self-sufficient as a result of hydraulic fracking and conservation. The emerging markets, where the incremental demand is expected to come from, are not growing as fast as they were previously. On the other hand, the expanding middle class throughout the developing world will want motorised vehicles, and this will drive future prices higher. In the meantime the present price is sufficient to finance current operations in the producing countries. If some capital projects need to be deferred because of insufficient funds, it is not a great tragedy.

If there were any geopolitical issue that troubles those living in the Middle East, it is the rise of ISIS. This is a more formidable military force than has ever been seen in the region with the exception of Israel.

Even though descended from Al Qaeda and therefore Sunni-based, ISIS is viewed in the Middle East as a terrorist organisation. There is general agreement that it must be stopped and both Saudi Arabia and Iran (not often on the same side of an issue) are funding the opposition. Financial support for ISIS is reported to come from independent sources in Qatar, Saudi Arabia and Russia, as well as the oil wells in Syria that their troops have captured. The Syrian rebels are effective but have limited weaponry. Iraqi military forces are inexperienced and need more training. American advisers in the region believe it may take as long as two years to mount a fighting force strong enough to retake territory already gained by ISIS. The United States could accelerate this process by sending a fighting force, but President Obama has already ruled that out.

At this point, nobody expects ISIS to move beyond Syria, Iraq and possibly Afghanistan. In the places I visited there is concern but not fear. Observers in the region are disappointed that the United States has not played a broader role. They believe that the US is not willing to back up its “red lines” after witnessing its failure to act when Syria used chemical weapons against its own people and when Iran moved forward with its nuclear weapons development program. The foreign nationals and the local citizens in the Middle East have a fatalistic attitude. They are used to living in warlike conditions and general adversity is part of the way of life there. They know that ISIS is a threat, but believe it is not likely to affect them over the near term. Right now they are more concerned about the price of oil and the direction of the financial markets.

This is an edited version of Byron Wien's latest global economic commentary released on November 3.