The valuation debate: My call

Summary: In a world of uncertainty, no one can give a definitive answer to the question of the “correct” discount rate and thus the fair value of stocks. The bond yield is critical in valuation, and when looked at in their historical context, current low bond yields don't look that unusual. It's likely bond yields will rise from their current point, although there are good reasons to think they will be lower than what we saw prior to the GFC. |

Key take-out: Investors need to be careful before branding equities as expensive, especially as it is unlikely bond yields will rise to pre-GFC rates. |

Key beneficiaries: General investors. Category: Economics and investment strategy. |

For some years now, I have highlighted how ultra-low bond yields change the notion of value in the stock market. Just how this can impact valuations was discussed by Simon Dumaresq and James Hannam in a piece on February 9 (see Are we valuing stocks correctly?).

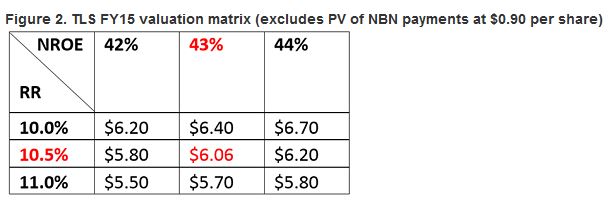

A stock specific example was highlighted perfectly in our most recent feature from Stocks in Value, on Telstra: Robust earnings for Telstra (February 23). Take a look at figure 2 in that piece. It shows how sensitive models are to changes in the underlying discount rate.

Source: StocksInValue

So for instance at a discount rate (or RR as it is referred to in figure 2) of 11%, Telstra has a fair value at $5.70 or nearly $1 lower than where it is now. Assuming a discount rate of 10% lifts that fair value price to $6.45 (Wednesday, February 25). But what if the correct discount rate is even lower than that? A 9 per cent RR means that Telstra is currently cheap – what about 7 per cent or 8 per cent?

Here's the crux of problem: What is the “correct” discount rate or more broadly the Weighted Average Cost of Capital (WACC)? Typically it's made up by the cost of equity – an equity risk premium to reflect the fact that stocks are risker than bonds – and the 10-year bond yield or risk free rate. By definition the correct rate is the opportunity cost of that capital – or the return that you could get elsewhere, that you are giving up to invest in a particular stock.

Yet in a world of uncertainty no one can give a definitive, table thumping answer to any of the above. So for instance, should investors even expect an equity risk premium in a bond bubble? In a bond bubble, stocks are less risky than bonds – or at worst, as risky. That being the case, the risk premium is zero and the bond yield is the required return.

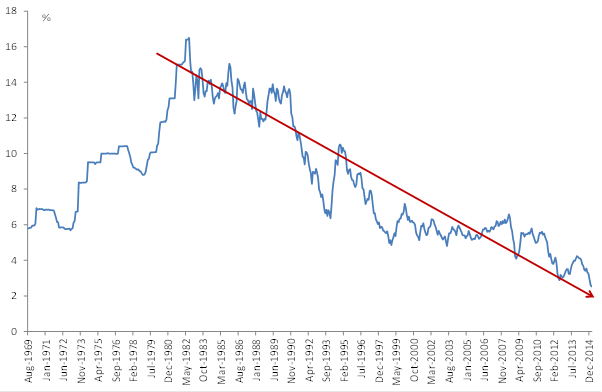

Even if people can't or won't accept that, the bond yield is critical in valuation – and chart 1 perhaps gives investors some perspective.

Chart 1: Australian 10-year bond yield

What is clear from the chart is that bond yields have been on a long-term downtrend since the 1980s. Why does that matter? Because historical experience doesn't necessarily support the idea that bond yields are set to rise to some sort of “normal” rate of 6 per cent, 7 per cent or 8 per cent.

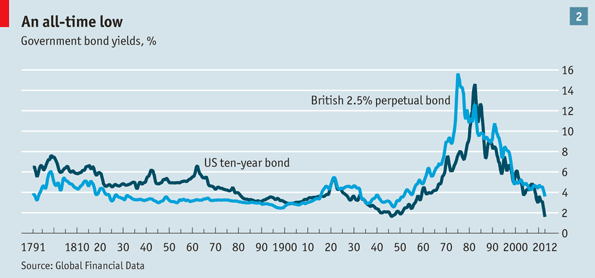

In fact if you look at a longer time period – the US 10 year bond yield from 1790 to 1970 – bond yields have actually spent most of their time below 5 per cent, and the vast majority of it – 130 years – between 2 per cent and 4 per cent. Only from 1970 to 2000, did bond yields rise well above 5% consistently – hitting a peak of over 15%. Looked at in that context, the current very low bond yields don't look that unusual. In fact what does look unusual is a bond yield above 5%. Although that that was sustained for 30 years!

Chart 2: US and UK bond yields since 1790

Unfortunately finance is a relatively recent study. It exploded from the 1970s onward and so you have an entire generation of analysts who may think that high bond yields are normal – when they're not. But it is these high bond yields which have typically fed into nearly all models of equity valuation, and it could perhaps explain the reluctance of many investors to use a lower, more historically normal, risk free rate. They're just not used to it.

In any case, I'm not arguing that we should revert to some even longer-term trend bond rate – 5 per cent by the way. But historical perspective is important when making long-term bond assumptions. What we can say, is that it wouldn't make sense to simply assume the very high yields experienced from the 1970s as some sort benchmark bond rate (8.5 per cent for the Australian 10-year government bond).

But noting that the 10-year bond rate is about 2.5 per cent currently, we do need to know the likelihood of yields rising from that point and the likely peak of the new cycle.

On the first point, it is highly likely that yields will rise from their current point. They are at their lowest since the 1960s and supported by quantitative easing programs in Europe, the US, the UK and Japan. At some point, the first three will end. That may be years from now and – let's be honest – it could be the wrong assumption but it is the best one.

What is harder to determine is how high yields will go in the post-GFC world, although I think there are very good reasons to think that they will be much lower than what we saw prior to the GFC. In the Australian context, the 10-year bond yield peaked in 2008 at 6.6 per cent – this was the highest rate since 2000.

Now think of the conditions that led to this 6.6 per cent growth rate. There was a global credit boom, a global housing boom, a stock market boom and a commodity boom. Global growth itself was booming and inflation was accelerating sharply.

We don't live in that world now and while global growth is robust and will continue to strengthen over the next few years, there are a couple of critical differences that should see bond yields remain lower than in the past.

The main one is that inflation is likely to remain lower now than pre-GFC. The lift that we saw in inflation over that period was largely driven by commodity prices. We don't have that now – commodity prices are falling and are very unlikely to surge to prior heights. The two main factors driving this are a lift in production capability but also a huge contraction in trading and investing activity in the commodity space. Since the GFC, the OTC derivative market has slumped by more than 75% (or about $6 trillion). That's why consumer price outcomes are so low now – and if it wasn't for the commodity surge through 2007-08, then inflation outcomes, and thus bond yields, would have been materially lower then as well.

Outside of that and longer term, technology is driving a broader disinflationary pulse and as we know, wages haven't driven inflation for decades. When you throw into that a glut of global savings and change to the capital requirements of financial institutions globally, bonds will remain well bid and therefore, yields low. It's unlikely in that environment that a 10-year bond yield would be sustained above 5 per cent for too long.

With that in mind, investors need to be very careful before they simply brand equities as expensive, especially as it is unlikely that bond yields will rise to pre-GFC rates.