The term deposits dilemma

Summary: Term deposit rates are nowhere near where they were five years ago, but searching beyond the big banks provides a relatively low-risk investment in uncertain times.

Key take out: Active management of term deposit accounts is key to ensuring returns stay above inflation.

The last week has seen volatility return to equity markets, while residential property price growth is slowing down. Investors looking for stable, low-risk returns might once again be looking at term deposits, but it's worth having a look at the performance of term deposits over the last five years.

Back in February 2013, if someone had invested $25,000 in a five-year term deposit, they could expect an average interest rate of 4.45 per cent, paid annually, and they would now have $31,080.09. Between March 2013 and the December 2017 quarters, annual inflation averaged 1.9 per cent.

That means the original deposit increased by an average of 2.55 per cent in real terms each year, or by $3711.93.

What if, instead of locking funds away for a five-year period, you instead decided to stick to one-year term deposits, looking to roll over the deposit each year for five years? Would that have made any difference?

The initial amount of $25,000 would have eventually become $29,880, when the last one-year term deposit matured. In real terms, that's a $2511.84 increase.

.PNG)

Source: Canstar (interest based on $25,000 term deposit)

Falling Returns

Of course, it's easy looking back and working out what the best strategy was, but planning ahead is more difficult. The Reserve Bank has lowered the cash rate 150 basis points since February 2013, with banks and other providers passing on the cuts above and beyond the fall in the cash rate. Some continue to slash rates, even with no change by the RBA since August 2016. Data from financial comparison site Mozo shows 83 term deposit rates were cut in the first three weeks of January, while only 17 rose.

Rates are at record lows, and aren't going anywhere fast, according to Curve Securities CEO Andrew Murray.

“The expectation going forward is for it (the cash rate) to remain unchanged potentially for all of 2018,” he says, and due to high household debt, when the RBA eventually moves, “rates will not move too far… it would have a very pronounced effect on mortgage holders”.

Canstar research head Steve Mickenbecker believes term deposits are no longer delivering returns neccessary for long-term investing.

"The days of retiring and putting money into term deposits are gone," he says.

Banks are also seeing a shift in the term deposit client base in a low wage growth environment. A Westpac spokesperson told Eureka Report, "While historically they (term deposits) have attracted customers 65 years and older, we are seeing increasing interest from younger customers".

Inflationary Risks

The bigger potential impact on term deposits comes from inflation. Any future rise could cause some longer period term deposits to lose value in real terms because, Mickenbecker says, returns are now sitting uncomfortably close to inflation: “it's a pretty skinny margin…there's not a great rate around”.

Murray is less concerned with inflationary pressures: “Wage growth is holding back the domino effect of moving to spending, retail sales and ultimately inflation,” he said. With unemployment still relatively high, there is little sign of wage growth on the horizon.

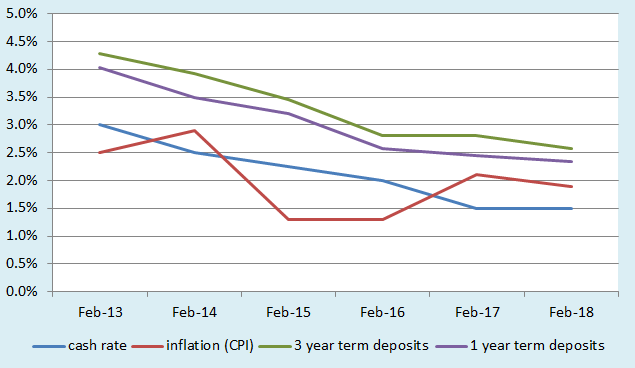

Chart: Term deposit rates compared to the cash rate and inflation

Source: RBA, ABS, Canstar

For those happy to risk rising inflation over the next few years, smaller financial institutions like Qudos, ME and QBank are offering 3 per cent interest on three-year term deposits. AMP Bank's 3.2 per cent, five-year term deposit is one of the highest rates available. The larger banks, however, are not bothering to compete with these smaller companies, with ANZ offering 2.5 per cent and NAB 2.7 per cent on three year terms.

Mickenbecker says this is down to the trust built in Australia's older banks, even with the Federal Government's deposit guarantee for balances up to $250,000, “people still feel their big bank is more stable and secure…when you've got market share you don't need to offer the best rates”.

Active Management

This is no excuse for not shopping around. As Eureka Report has covered previously, most banks will automatically roll over maturing term deposits unless instructed not to. Mickenbecker says it's hard to make positive returns if you aren't actively managing your term deposits, “you should never give a bank the ability to roll over at maturity”. Searching for more competitive rates or speaking to your bank for alternative term lengths can help.

Even if actively managing term deposits, Murray says it's worth holding multiple deposits of different lengths to minimise risk, “five years might be a bit long to put all your eggs in one basket”.

If locking funds into term deposits isn't appealing, there are a handful of other options to consider. Most savings accounts have a low base interest rate but do offer competitive introductory rates. Changing banks regularly to take advantage of those offers is possible, but it can be administratively time-consuming.

Murray mentions ING's Savings Maximiser, which has a variable rate of 2.8 per cent, (provided you deposit $1000 monthly and meet some other conditions) as a more practical alternative: “You've still got flexibility to draw money out and you don't have a honeymoon rate,” he says.