The recession Australia could have

Summary: The probability of a real recession occurring is very low over the next year or so as consumers are in a good space and the LNG export boom hasn't even started. A technical recession is a higher probability but the prospects for this are still slim. Historically, each of the precedents since the late 1970s featured a spike in interest rates or a global economic shock. |

Key take-out: At this point, talk of a global or domestic or global recession might make good press but it shouldn't be given undue emphasis in any investment decision. |

Key beneficiaries: General investors. Category: Economy. |

Could Australia really slip into a recession? After all, Canada has and they're just like us. Predominantly Anglo, open and dependent on commodities.

The short answer is yes – and at the same time, no. Economists at Goldman Sachs attribute a 33 per cent chance of a recession occurring before the next election and subsequently forecast that the RBA will resume easing in about six weeks. Similarly, economists at ANZ now think the RBA will cut twice in early 2016, starting in February.

I'm not trying to be smart by giving a yes/no answer. Much depends on what you actually mean when you talk of a recession: A real recession or a technical one. There is a difference and it's more than just some pedantic economic double speak.

The difference will matter a lot for your investment portfolio.

A real recession is when growth slumps and the unemployment rate rises. Australia has had two of these since the 1980s and in both instances the unemployment rate shot up into the double digits. In both instances monetary policy was the cause, as it was very restrictive and inflation was high. The world was in recession.

A technical recession on the other hand – or a ‘Claytons' (the drink you have when you're not having a drink) recession – is one where it's not really a recession. Even so, GDP growth may manage to be negative for two consecutive quarters. Naturally such an event would see many commentators break out into spontaneous applause and rapturous laughter.

That clarification out of the way, the probability of a real recession occurring is very low over the next year or so. Consumers, the largest chunk of the economy, are in a good space. To get a real recession consumer spending needs to collapse. Yet this is unlikely given that jobs growth is strong and monetary policy is extremely stimulatory. Savings are otherwise high. Elsewhere, the LNG export boom hasn't even started and the construction boom has some way to go yet (see Putting this property market in perspective, September 16).

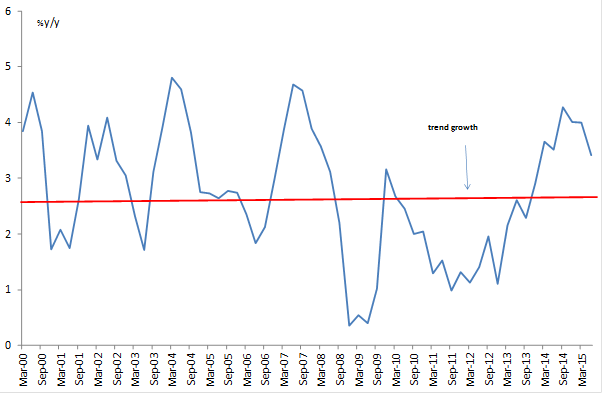

Chart 1: GDP excluding mining investment growing at a strong clip

Source: ABS, Eureka Report

All of this is why you see economic growth, excluding mining investment, growing at a strong clip. As chart 1 shows, growth outside of the mining sector is well above trend and has been for nearly two years now. That's why jobs growth has been so strong. Mining investment doesn't employ many people. Mining at its best employs 2 per cent of the work force.

The non-mining sector by contrast comprises about 92 per cent of the economy, it is a big employer (98-99 per cent) and is growing at a solid clip. The LNG boom mentioned above is expected to add quite a lot to this this economic growth. By itself, the RBA reckon that the LNG boom will add about 0.5 to 0.75 percentage points to GDP over the next two years. That's sizeable and something that will offset any fall from investment.

Despite this, the second option, the Claytons recession, is certainly a chance – a much higher probability than a real recession. Even so, the prospects for this are still slim, perhaps 15 per cent or so. Even assuming it did happen, it would reflect nothing other than dumb luck. An unfortunate timing effect more than anything. There are a few reasons for this.

First, on a sensitivity analysis I've done, it's very difficult to get two quarters of negative growth in GDP even assuming the peak of the housing construction cycle occurred in the March quarter of 2015.

That means I've punched in numbers that show large falls in mining investment and large falls in housing investment. I've also assumed below trend government and consumer spending – even presuming, in both cases, softer spending than what we've seen over the last year.

The economy would be weak admittedly, but not in recession.

As I mentioned earlier, you need to see falls in consumer spending to get a recession and that doesn't happen often. The last time was in the second half of 2008 and that was when mortgage rates averaged 9 per cent. Double what they are now.

Typically to get sustained falls in consumer spending you also need to see a fairly dramatic spike in the unemployment rate. Once again though, if you look back though history, you don't tend to get that without two conditions. It's happened four times since the late 1970s and in each case you saw either or both of:

- A spike in interest rates, or

- A global economic shock.

You begin to see the circularity. But it highlights a very important point: Australia doesn't just have spontaneous spikes in unemployment .They are caused by a surge in interest rates or some kind of global economic shock. Thought of another way, high unemployment doesn't cause a drop off in spending nor cause recessions. Recessions, usually induced by high interest rates, instead cause high unemployment, which then tends to crunch consumer spending.

This brings me back to the other reason a real recession is a low probability and why even a Claytons recession is unlikely. That's because and as I discussed last week (Global growth fears are unfounded, September 23) the idea that global growth is faltering is not true. It is unfounded – there is no evidence for it.

With that in mind it's best that investors ignore talk of either a global or domestic recession at this point. It might make for good press and is certainly thought provoking, but it shouldn't be given undue emphasis in any investment decision.