The pressure is rising on Aussie property

Summary: Australia's housing market isn't the safe investment vehicle that it once was. |

Key take-out: New lending activity suggests that house prices are either at or near their peak. |

Key beneficiaries: Property investors. Category: Economics. |

The Australian property market has become an increasingly unappealing investment vehicle outside of hotspots in Sydney and Melbourne. With real house prices well below their peak in most capital cities, rents declining and new apartment buildings popping up everywhere, domestic investors are facing a monumental shift in Australia's property market.

Property investors enter (and re-enter) the market for a variety of different reasons. Some buy property in search of capital gains; others are looking for a reliable source of income. But maximising your return requires consideration of both income and capital and needs to focus on the future rather than the past.

This week I wanted to explore three separate issues that will shape Australia's property market for domestic investors. The first is growth in rents or the rental yield available for property investors. The second is capital growth. The third and final issue is new housing supply.

Rents and rental yield

By international standards, the rental yield on Australian investment property is exceptionally low. The national rental yield for Australia is 3.3 per cent – below the standard variable mortgage rate – and it is lower again in property hotspots like Sydney and Melbourne. Once you account for strata fees, other utilities and interest costs, the effective rental yield on Australian property is often negative or negligible.

Overseas, particularly in countries with less favourable negative gearing concessions, you can regularly find rental yields in the vicinity of 7-10 per cent per annum.

This has long led to the suggestion that most property investors are infatuated with capital gains rather than rental income. This is true to some extent but ignores the importance that many retirees and older investors place on rental income to support their standard of living.

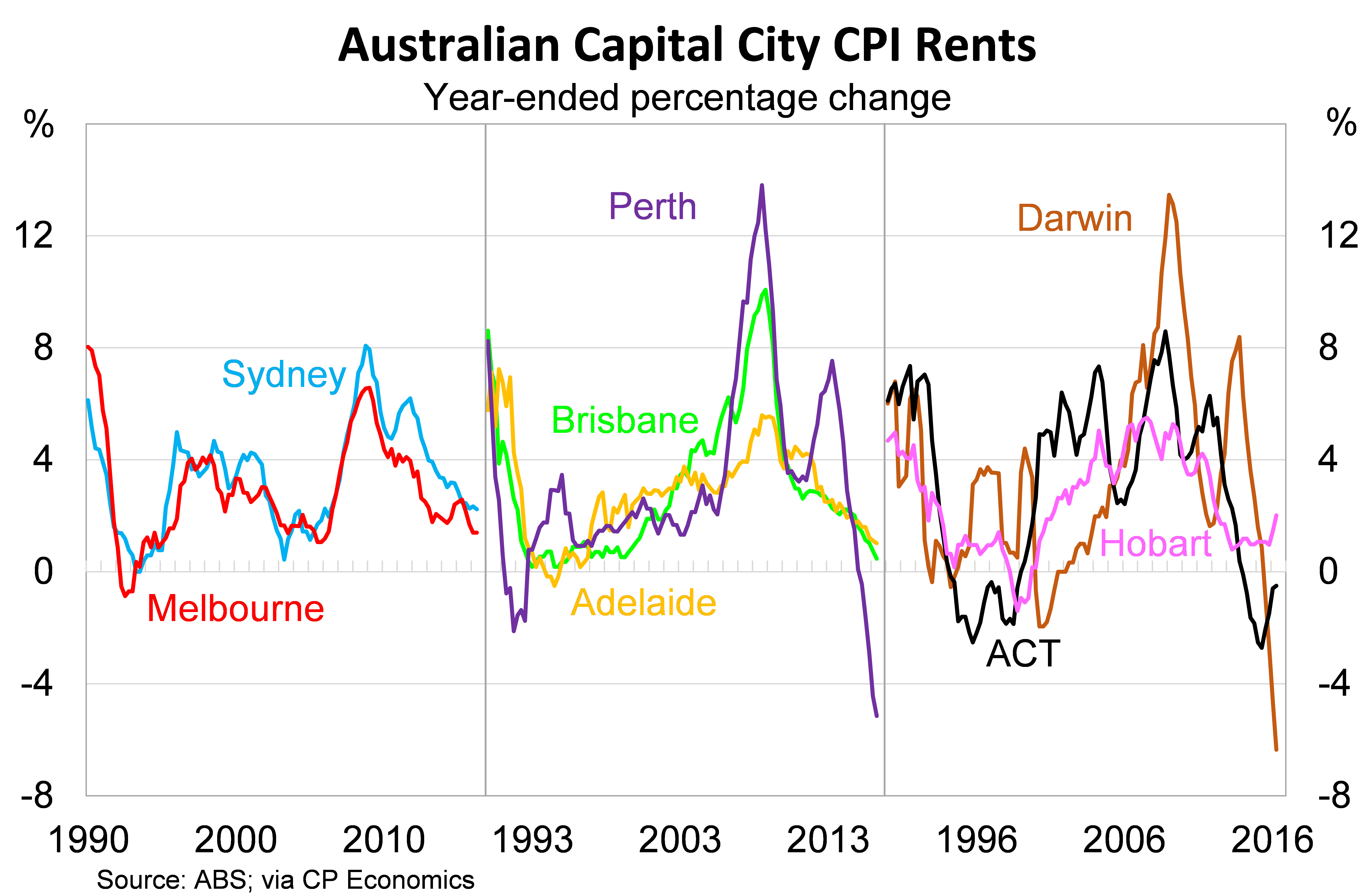

The bad news for property investors is that rents have taken a turn for the worst. We have two main measures of national and capital city rents. The first is derived from the inflation figures, known as CPI rents, and measures the change in rents across the entire rental stock. The second is a private sector measure from the property group CoreLogic that measures changes in newly negotiated rents. The latter is a more volatile measure but provides a better assessment of near-term shifts in rental conditions.

Neither measure is giving property investors cause for optimism.

National CPI rents rose by 0.7 per cent over the past year and once we account for inflation real rents actually fell by 0.8 per cent. National rents are now growing at their slowest pace since the December quarter of 1994.

But analysing a national rental market is of limited value to investors. Each capital city differs significantly with regards to demand and supply, so we need to break these figures down.

The national figures hide the remarkable weakness in Perth and Darwin where rents have declined by 5.2 per cent and 6.4 per cent, respectively, over the past 12 months. Other capital cities have fared better – Sydney rents are up by 2.2 per cent and Melbourne rents by 1.4 per cent – but there isn't a single mainland rental market that could be regarded as strong.

Hobart is perhaps the exception with rents rising at 2 per cent over the past year – though newly negotiated rents are rising at a faster pace – and rental yields sit well above the national average. For investors focused on rental income, Hobart is currently the city of choice.

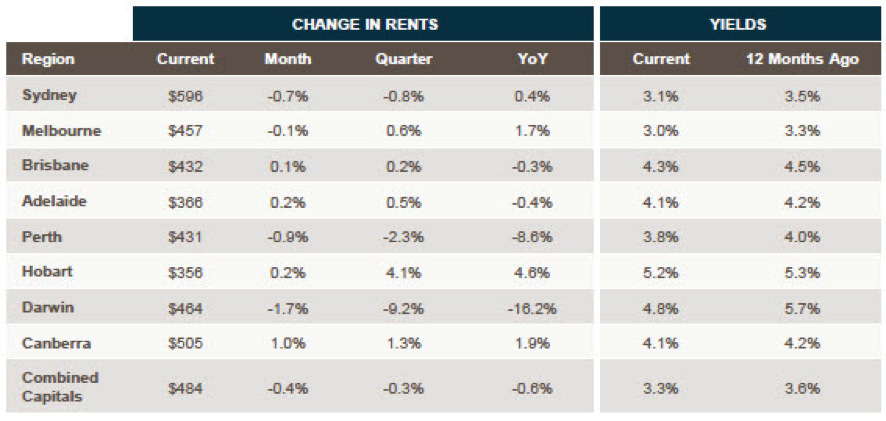

The CoreLogic data on newly negotiated rents paints a similar though bleaker picture. According to CoreLogic, newly negotiated rents fell by 0.4 per cent in June and are 0.6 per cent lower over the past year. Rents have collapsed in Perth (down 8.6 per cent over the year, or $41 a week) and Darwin (down 16.2 per cent, or $90 a week).

The table below, obtained via CoreLogic, contains rental growth and rental yields for each of the capital cities. The rental yield is highest in Hobart (5.2 per cent) and lowest in Melbourne (3 per cent). (More analysis on rents by CoreLogic can be found here.)

Source: CoreLogic

Rental yields nationwide have been squeezed over the past 12 months. In some cities this has been driven by growth in house prices, such as in Sydney and Melbourne, while in Perth and Darwin it reflects the fact that rents are falling more quickly than prices.

It's also worth pointing out that while capital city rents are performing poorly in aggregate there are some suburbs where rental growth remains quite strong. (For a list of these regions see here.)

House prices

Investors focused on capital gains also have a lot to think about. Property outside of Sydney and Melbourne hasn't been a great investment for the best part of 5-10 years. I touched upon this back in June but it is worth reiterating (Why the golden days of property investment are over, June 6).

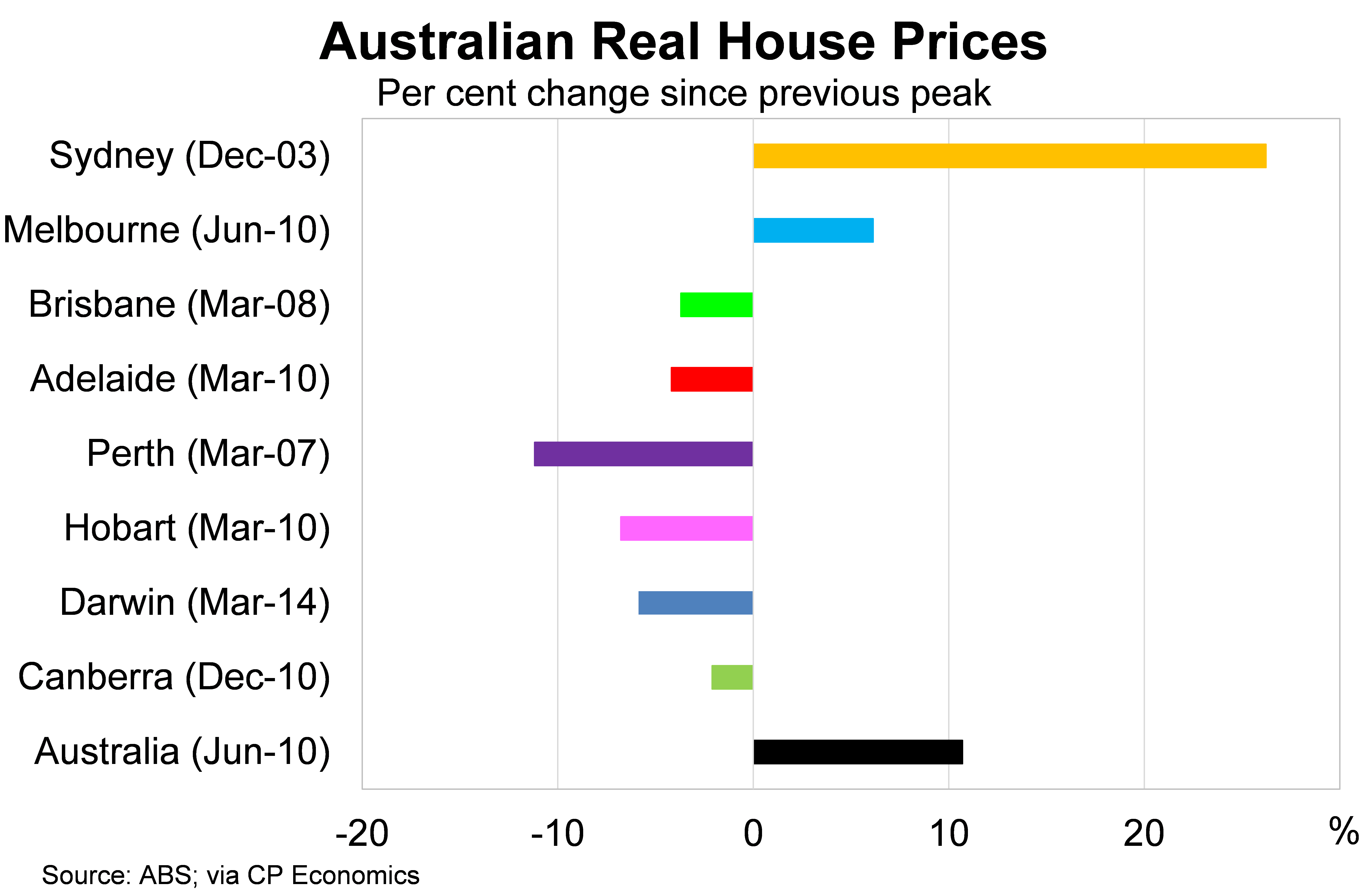

Real house prices across most capital cities have failed to post genuine capital gains over the past 5-10 years. Real house prices in Perth, for example, are currently 11 per cent below their peak in the March quarter of 2007. Prices in Brisbane today are lower than they were eight years ago. In most other capitals, real house prices were higher in 2010 than they are today.

The two exceptions have obviously been Sydney and Melbourne where prices have boomed over the past few years. Strong investor demand, particularly among foreign buyers, has created a housing market that couldn't be more different to those across the rest of Australia.

The graph below shows how real house prices have changed compared to their previous peaks.

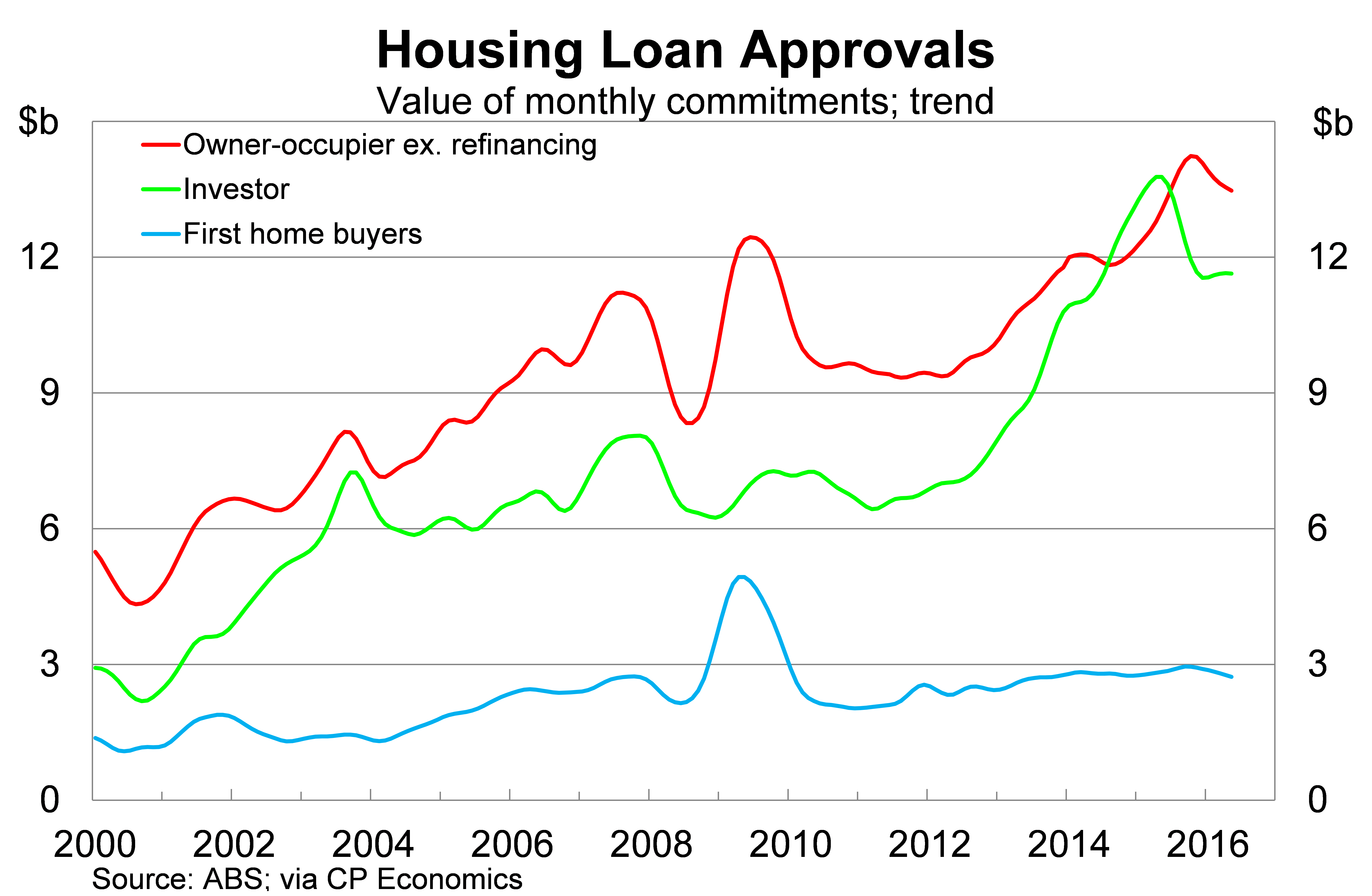

Lower interest rates – including Tuesday's rate cut by the Reserve Bank – are likely to support house prices in the near-term. Nevertheless, new lending activity suggests that house prices are either at or near their peak. New lending activity has now fallen 6.8 per cent from its peak and mortgage lending is typically a superb indicator of house price developments.

Mortgage lending is still at a very high level – as the graph below indicates – but it must keep rising to support house prices. If new mortgage lending continues to ease then it is likely that house prices will follow suit. That weakness should be concentrated in Sydney and Melbourne – since these capital cities drove the initial rise in lending – though weakness in the likes of Perth is expected to continue over the next few years.

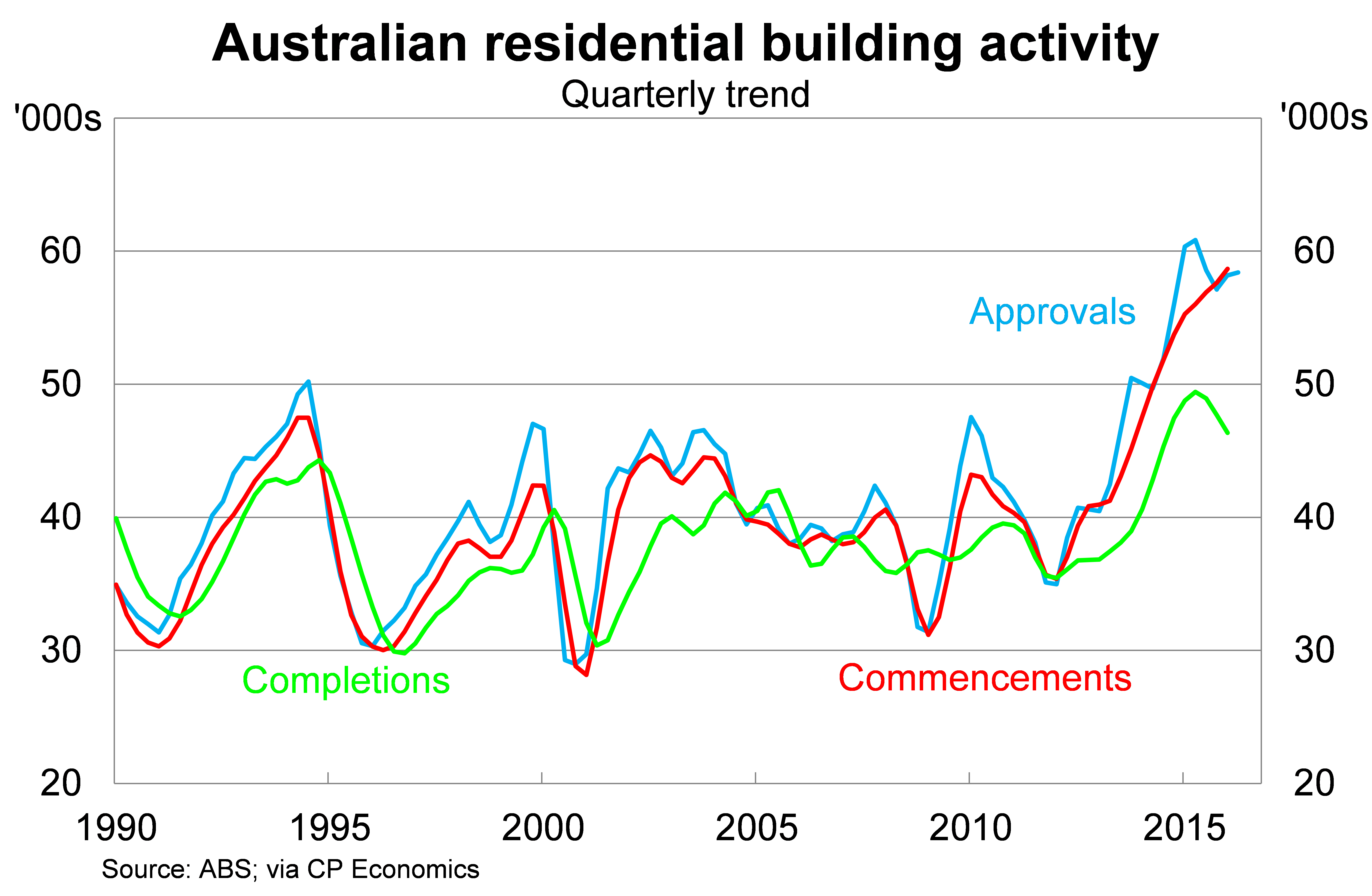

Housing supply and residential construction

The final issue worth discussing is the supply of new housing. House prices and rents are partly determined by the demand for property but also by the supply of new property being constructed. Supply restrictions – which have existed in the past – can place upward pressure on prices and rents. A surplus of new property, though, can create the opposite scenario.

If you take a look around the Sydney or Melbourne skylines you'll see that there is no shortage of new property developments beginning to take shape. Our biggest cities are awash with cranes building new apartments in inner-city areas.

But while residential construction activity remains elevated, the data on residential building approvals and completions suggest that activity has passed its peak. It will remain at an elevated level in the near-term – see the 'commencements' line on the graph below – but activity will be somewhat weaker than in the recent past.

In the near-term this should be sufficient for new supply to outpace population growth. Combined with low wage growth and lower mortgage lending and it appears likely that new housing construction will put downward pressure on rents and house prices over the next year or two.

Rental growth is hamstrung by weak wage growth – since prices are determined in large part by the capacity of renters to pay – and it is unlikely that investors will see a big pick-up in rental income until wages begin to improve. House prices, by comparison, may find additional support via lower interest rates and foreign demand but it will be difficult for markets such as Sydney and Melbourne to replicate their recent gains.

For property investors and prospective property investors, it is important to recognise that the Australian housing market isn't the safe investment vehicle that it once was. It has slowly and subtly changed over the past decade and now presents a much greater risk than it has in the past.

We now face unprecedented weakness in rental markets and poor capital returns outside of Sydney and Melbourne. Most cities simply don't offer the capital gains that are sufficient to reward the risk involved with taking on 6-10 times your income in debt. And if house prices aren't rising then you've really got to ask yourself "what's the point?" particularly when term deposits offer a higher return than rents.