The factors that will shape UK growth

Growth in the UK moderated somewhat in the December quarter but prospects remain solid for the year ahead. Lower oil prices will support household spending but the big uncertainty is productivity growth, which could be a game changer for the UK if it has finally begun to improve.

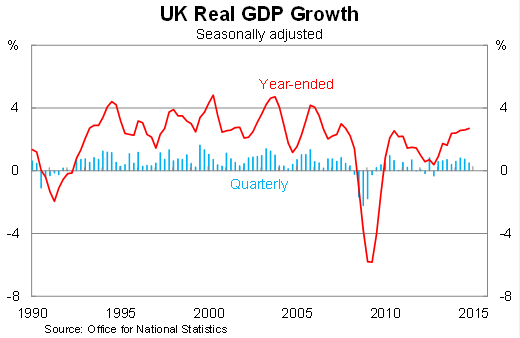

Real GDP rose by 0.5 per cent in the December quarter, missing market expectations, to be 2.7 per cent higher over the year. Although the pace of quarterly growth slowed -- down from 0.7 per cent in the September quarter -- annual growth is running at its fastest pace in seven years.

Growth was driven by services (up 0.8 per cent in the December quarter) and agriculture (up 1.3 per cent). This was partially offset by weakness in production (down 0.1 per cent) and construction (down 1.8 per cent). Services contributed 0.6 percentage points to quarterly growth, while construction subtracted around 0.1 percentage points.

It is too soon to tell whether the slowdown in December is meaningful or simply reflects quarterly volatility. There is also the possibility that growth will be revised up -- this is just a preliminary reading -- particularly with regards to construction activity, which was somewhat weaker than other indicators suggest.

The outlook for the UK economy remains fairly bright but there are a number of challenges and opportunities that will shape growth over the upcoming year.

Household spending will continue to receive a boost from low oil prices. Inflation has taken a beating in recent months and is now just 0.5 per cent higher over the year -- the slowest rate of inflation since 2000 (Don't be too concerned about deflation in the UK, January 14). The result is stronger household budgets and that will continue to underpin household spending in the months to come.

Global growth does remain a key concern though. The recovery in the US continues to find its footing and appears poised for stronger growth than the Bank of England predicted back in November.

But Europe remains a concern. Even with the ECB's new quantitative easing program, it remains unlikely that it will prove sufficient enough to drag the eurozone towards a persistent recovery. As a result, British exports continue to face an uncertain future -- conditions could pick up more quickly than commonly believed but are equally likely to remain depressed for the foreseeable future.

One area where the effects of quantitative easing are more certain is with respect to the British pound. Expect the sterling to be somewhat stronger against the euro than the BoE would prefer and potentially an impediment to near-term growth. The Federal Reserve is still expected to raise rates later this year -- certainly much earlier than the BoE -- and that may provide some currency relief further out.

However, the key challenge for the UK economy relates to productivity growth -- or the lack thereof. The labour force is growing strongly, the unemployment rate is down to its lowest level since August 2008, but unless productivity begins to respond, the current recovery will prove unsustainable.

In a recent speech, Kristin Forbes, a member of the BoE's Monetary Policy Committee, said that “key forces which may have been holding back productivity growth may now have faded, such as: low business investment during the crisis; a weak banking system that was inefficiently allocating capital; and limited labour market mobility which inefficiently allocated workers.”

That may well be the case but the BoE has made it a habit of overestimating productivity growth and has had to revise those expectations down consistently since the crisis began. However, if Forbes is correct, that is the type of development that could shift UK growth prospects higher, lead to stronger wage demands and eventually result in more rapid policy normalisation.

The UK economy is tentatively poised right now. Employment is strong, wages are slowly picking up but inflation remains at low levels. Growth should remain moderate, potentially stronger than expected, if productivity growth rises, although there are clear concerns about the construction sector.

Will the BoE raise rates this year? That's uncertain. The most likely scenario for a rate hike is a situation where oil prices begin to stabilise and employment growth flows through to higher wage demands. Stronger productivity could counteract this but I'd expect the wage response to occur more quickly and push inflation towards the BoE's annual target.

However, if oil prices take longer to stabilise -- spreading out the pass through to domestic prices -- then the BoE is likely to delay a hike until next year.