The construction risks for property investors

| Summary: Rising supply within the higher-density apartment sector threatens to put downward pressure on apartment prices and rents. |

Key take-out: The concentration of construction in higher-density properties means that the construction boom won't have the same spillover effects that we have seen during past booms. |

Key beneficiaries: General investors. Category: Economy, property. |

Residential construction has been a bright spot for the Australian economy, supporting growth during a difficult period, but the ongoing boom presents a risk for property investors.

New data on building approvals, which typically leads construction activity by a good 12-18 months, suggests that residential construction will remain strong into 2018. This rising supply, particularly within the higher-density apartment sector, threatens to put downward pressure on apartment prices and rents. We are already seeing this to some extent with apartment price growth in Sydney and Melbourne trailing that of detached housing.

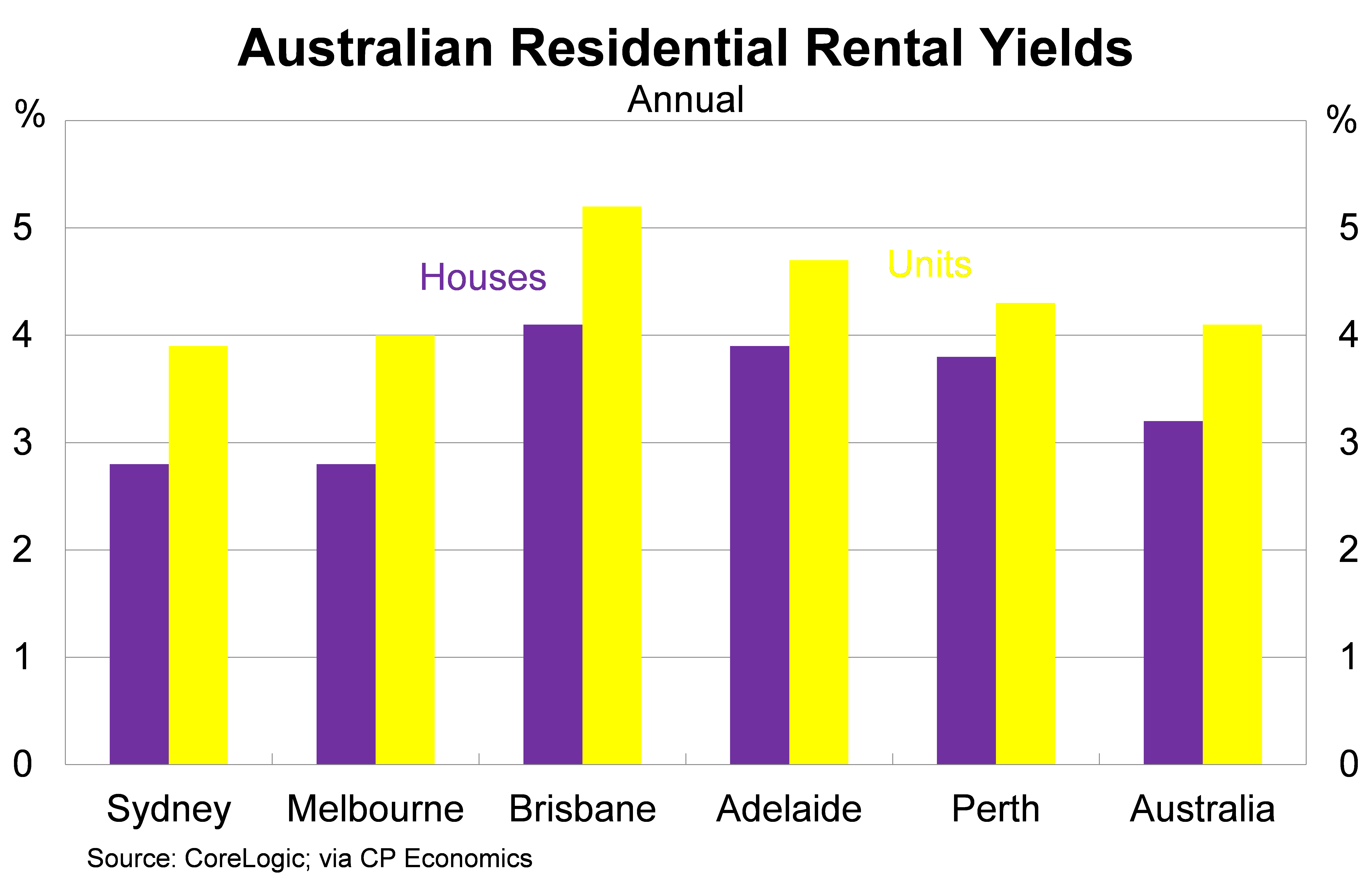

Adding further concern, newly negotiated rents are falling across most cities and rental yields have tumbled to their lowest level on record (summarised in the graph below). With so much new supply set to be completed over the next two years we can expect rents and yields to fall further before they begin to improve.

Earlier this week the Australian Bureau of Statistics released new data on building approvals, which measures the number of houses and apartments approved for construction. It is a useful leading measure of residential construction activity and one of the measures closely watched by policymakers across the country.

Building approvals rose by 0.6 per cent in August on a trend basis, to be 4.4 per cent higher over the year. Monthly approvals currently sit slightly below their peak established in April 2015.

Growth has been concentrated in higher-density approvals, which should come as no surprise to those readers who frequent inner-city Melbourne and Sydney. Approvals for private higher-density dwellings have increased by 12.4 per cent over the past year and currently sit at their highest level on record.

Approvals for private detached housing have been somewhat weaker and currently sit 5.3 per cent below its peak. Month after month we are seeing a shift towards inner-city apartment living. This is partly being driven by changing preferences but also by necessity – people want to live where the jobs are. The narrowing of Australia's manufacturing base, as well as the rise of services, is forcing Australians towards inner-city jobs.

A construction boom will inevitably give rise to concerns about oversupply. Have property developers over-invested in response to rising property prices across Sydney and Melbourne?

There is no definitive answer to this question. Estimating under and oversupply in the housing market is a complicated business and typically there are too many unknowns to arrive at a definitive answer.

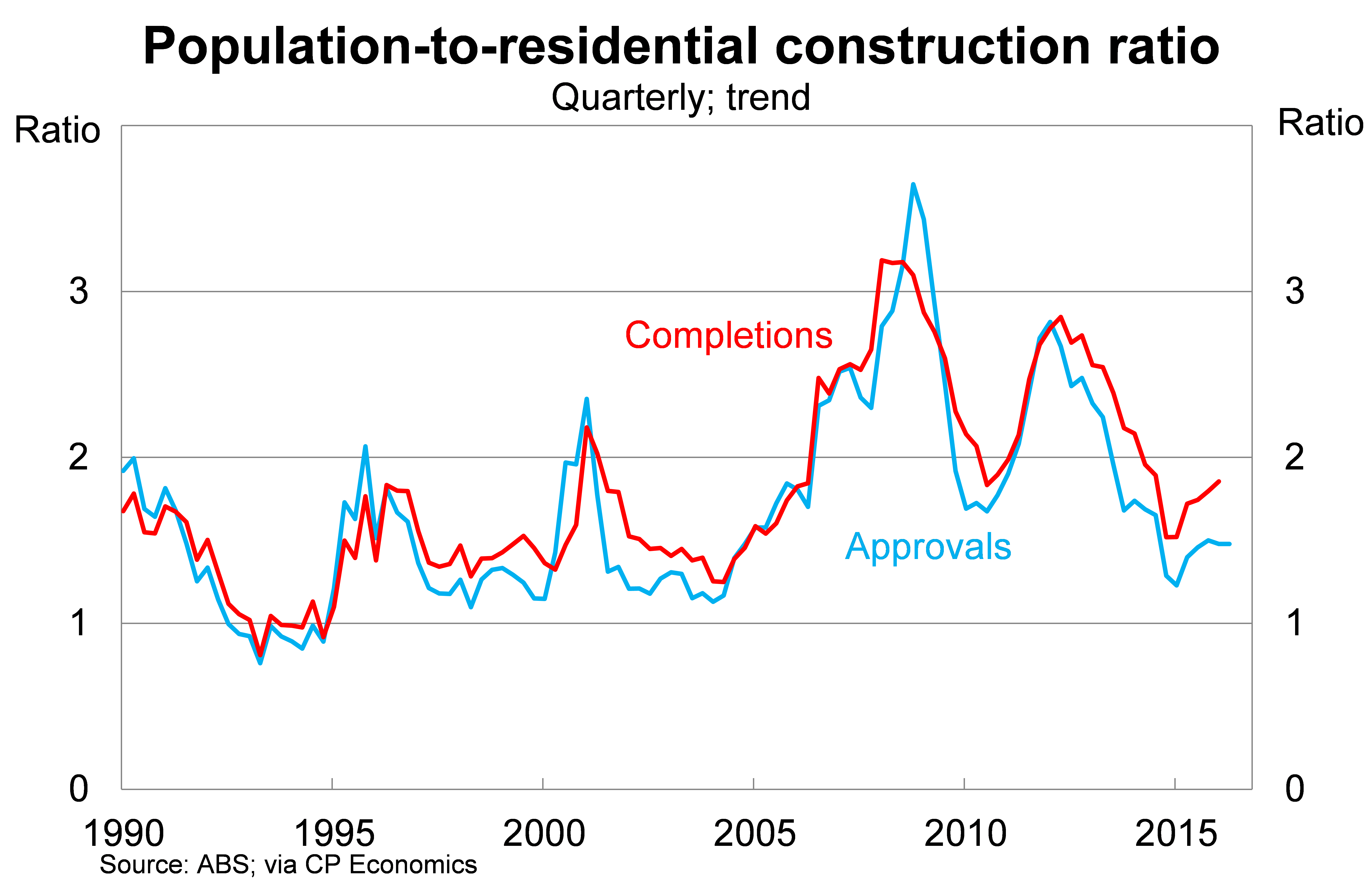

Nevertheless, one useful technique is to compare building approvals or completions against population growth. This measure doesn't say anything about the rate of housing formation or average household size but it does provide a rough proxy that might prove useful for investors.

The graph below shows that supply imbalances have eased in recent years as residential construction has increased. There is a great deal of divergence from state to state; relative supply is rising fastest in South Australia (where annual approvals exceed population growth) and slowest in Victoria (ratio of 1.9) and NSW (ratio of 1.6).

This would provide some evidence in favour of the view that supply shortages can help to explain the residential property boom in Sydney and Melbourne but also the weakness across the rest of the nation. It's also consistent with the recent decline in newly negotiated rents. Perhaps the most interesting implication though is that it indicates that the greatest risk of oversupply may currently exist outside of Sydney and Melbourne.

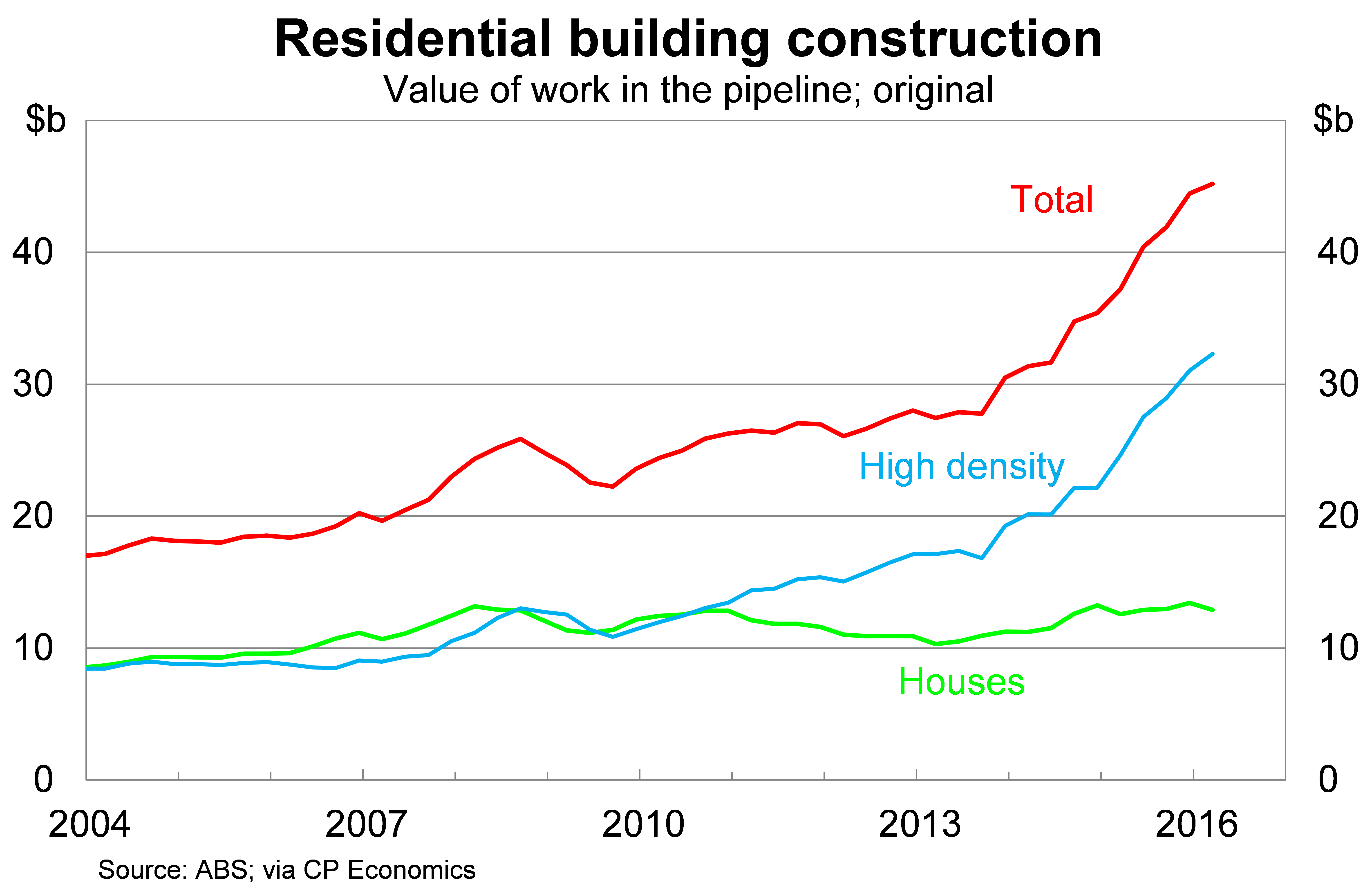

In analysing housing supply issues we can't just focus on approvals or construction activity completed. We must also assess the value of construction yet to be done. The data indicates that we still have a huge pipeline of construction that needs to be completed and this will keep residential construction activity at a high level through to at least 2018.

The graph below shows the construction pipeline for detached and higher-density properties.

The concentration of construction in higher-density properties means that the construction boom won't have the same spillover effects that we have seen during past booms. Construction of detached housing often leads to a renovation boom, but that isn't possible in the higher-density sector.

Those living in apartments are also less likely to purchase household goods, particularly high-quality household goods, so the retail response to the construction boom may prove muted compared with past episodes. So it's a mixed bag for key retailers, such as Harvey Norman, Myer and David Jones, who tend to outperform during construction and renovation booms.

Investors will need to balance these risks. They know by now that the housing market isn't quite as buoyant as it was during 2014 and 2015. The big gains are over and finding strong capital growth will require more research and greater due diligence than it has in the past.

Rental yields are often a minor consideration for property investors – hence the popularity of ‘negative gearing' – but it would be foolish to ignore the recent fall in newly negotiated rents. The size of the construction pipeline all but ensures that rents will fall further over the next couple of years.

A word on monetary policy

Finally, I wanted to touch briefly upon the Reserve Bank of Australia's board meeting this week. As expected it decided to leave the official cash rate at 1.5 per cent. The cash rate has been cut by 325 basis points since October 2011.

According to the RBA, “the Board judged that holding the stance of policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.” The board statement offered little insight into the future direction of policy, although the market still believes that the next move is down.

The market is currently pricing in a 24 per cent change of a rate cut in November and a 78 per cent chance of a cut by June next year. Market expectations will shift later this month on the back of new inflation figures for the September quarter (out October 26), as well as the usual raft of monthly releases such as employment and retail sales.

There is a clear reluctance from the RBA to cut interest rates further, emphasised in governor Philip Lowe's testimony before the House of Representatives last week, but I'm not convinced that their reluctance is credible. The bank has been reluctant to cut interest rates for the past two years but has folded each time our economic transition has been challenged by low inflation or an excessively high dollar.

Inflation remains the most important consideration for monetary policy but policy decisions elsewhere, particularly from the US Federal Reserve, will have important implications for the RBA. The Federal Reserve is expected to hike rates later this year but if they don't we may be faced with an Australian dollar that pushes towards US80c, which would undermine some of the recent improvement in our non-mining sector. If this eventuates then the RBA has little choice but to cut interest rates further regardless of its current reluctance.