Smooth operators

Summary: If share markets fall dramatically. Retirees' asset bases can become insufficient to meet their needs. Investors can hold a diversified portfolio of income stocks, which can reduce stock specific risk, but it can't overcome general market risk. New products in the quant sector are using powerful risk management techniques to address this issue. |

Key take-out: A managed risk strategy can be used to overcome the limits of traditional products like annuities and help retirees manage risk. |

Key beneficiaries: General investors. Category: Strategy. |

The Murray report into the financial system has picked up on the hype from the annuity sector to recommend that more post-retirement “income” style products should be designed and included in retiree portfolios.

When Nobel laureates like Robert Merton spot shortcomings in our current obsession with accumulating large capital bases for retirement, we do need to be aware of the importance of income certainty in retirement.

The benefit of equity income investing is the main reason for the popularity of bank stocks for many Australians. High dividends from good companies, which grow their earnings over time with the prospects of growing yields for investors, can be a good way to fund retirement income needs. The problem of course is that many retirees will eventually have to “draw down” on their portfolios, selling stocks progressively as they age to maintain their retirement lifestyle. That's where sequencing risk and tail risk come into play – if share markets fall dramatically during this draw down phase, retirees' asset bases can quickly become insufficient to meet their needs – as more and more shares are required to be sold down at reduced prices.

There are a few ways to try to reduce this problem:

- Owning a diversified portfolio of income stocks directly or through a product like an ETF or managed fund (this reduces stock specific risk but can't overcome general market risk);

- Investing in a product which uses a mechanism to select and rotate through a variety of asset classes to produce enhanced levels of income – often these products invest in stocks, hybrids and fixed income assets which does diversify the sources of return but also can't overcome general market risk);

- Invest in “combo” style products like annuities where the riskiness of equities is balanced by heavy allocations to fixed income, which does reduce volatility and equity risk but which can also significantly reduce levels of income payments especially in low interest rate environments;

- Invest in “Dynamic Asset Allocation” (DAA) products which aim to move rapidly between risky assets like stocks, into cash holdings when market risk rises (the so-called “risk on/risk off” approach);

- Invest in the new wave of absolute return style funds which are managed using quantitative techniques and derivatives to target good returns with risk management to protect against downside risk.

The good news is that new products in the quant sector such as the Plato Australian Shares Income Fund (Managed Risk) use powerful risk management techniques and are leading the way in product development in this space.

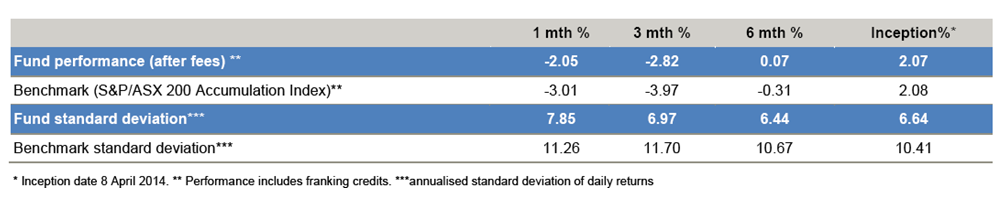

The Plato “Managed Risk” fund invests into the well-established Plato Australian Shares Income Fund and adds a smart risk management overlay developed to reduce volatility and minimise downside risk. The new fund was launched in April this year and since then has produced returns in line with the ASX 200 index but with significantly lower volatility – broadly in line with its design objectives.

Source: Plato Investment Management

The Plato fund is a classic example of the risk managed quant fund. It uses a mathematically based approach to select stocks for their bias towards producing higher than normal levels of income. It then overlays a derivatives strategy developed by the global risk management firm, Milliman Inc. Milliman is probably a new name to most Australian investors, even though it was established in 1947 and provides risk management services globally for over $500 billion of assets and in respect of over 60 million individual account holders.

That's an impressive pedigree but even more exciting is the technology it provides to funds like Plato. This Milliman technology was in use by a number of insurance companies and institutions during the GFC and showed strong resilience in protecting portfolios against loss, and is now being deployed in products available to retail investors (like the Plato fund, and a new ETF issued by Betashares, which also has a focus on equity income).

The Milliman derivative overlay is known as the “Milliman Managed Risk Strategy” and rests on two simple ideas:

- That the volatility of portfolios can and should be capped at levels around the long term market average by using derivatives and this reduces the risk of large falls in capital value when markets crash;

- That downside portfolio risk can be limited by using put options to insure against market falls.

Both these ideas are not new but when used traditionally, the costs associated with buying derivative protection acts as a drag on performance, eroding returns to below acceptable levels. Fund managers like BT profited massively from buying put options prior to the 1987 crash, but the problems of picking when to buy puts (ie the market timing issue) makes this an expensive hit and miss strategy for most investors. As a result, most professional managers shy away from using put options to manage downside risk, which makes the Milliman risk overlay all the more compelling as a lower-cost alternative to buying put options.

Similarly, traditional volatility capping relies on selling down stocks during periods of heightened volatility – this can reduce risk but also crystallises losses in a falling market and leads to high portfolio turnover and tax inefficiency.

The beauty of the MMRS is that it uses smart derivative ideas to implement both aspects synthetically – ie, without the need to physically sell stocks or buy put options. It accomplishes this by:

- Short selling share futures contracts when stock market volatility rises – this leads to the volatility of the underlying portfolio being capped at desired levels because the net equity exposure is reduced (without needing to physically sell stocks);

- Using this approach of capped volatility, when markets trend downwards the MMRS enters into further short selling to replicate the techniques that would be used by the seller of a put option. This means that the MMRS creates the risk profile of a fund which has purchased put options, but at far lower cost.

The MMRS is managed daily and relies on market signals to determine the extent of short selling that needs to be actioned each day.

This is certainly a complex approach, but the returns delivered by the MMRS during the GFC showed significant out-performance over other methods – and hence the MMRS is being actively used around the world for its strong potential to overcome the problems of sequencing and tail risk.

In the Plato fund, the MMRS is overlaid onto a broad basket of ASX blue chip stocks which are selected using quant methods developed by Plato. This selects between 50-120 stocks based on the Plato in-house model which targets stocks with a likelihood of paying a strong dividend and at the same time, as having the prospect of recovering quickly from the fall in share price after the dividend is paid.

This approach is known as the “Dividend Run Up” strategy and is based on the idea that stocks with growing earnings will be bid up by investors so that the price fall after a dividend is paid will quickly be offset by share price increases. This strategy is a way of harvesting dividends from stocks while having some immunity from price falls after dividends are paid. There is research and academic support for the validity of this strategy (click here).

This strategy leads to high levels of turnover which in the case of the Plato fund can be as high as 150% pa, so the Plato fund is marketed as being most suitable to investors in retirement phase and paying 0% tax.

Franking credits are also targeted by the Plato Fund – something that many Australians recognise as highly valuable in retirement phase. That's why the bizarre suggestions in the Murray FSI that we should scrap our dividend imputation system (because of the perception by Murray that this distorts investments in favour of Australian shares) is misguided. Instead of scrapping imputation, investors should consider using risk management techniques like the MMRS to control downside risk.

That leads to the rationale for the Plato Fund. Readers of Eureka Report like to invest directly for themselves. In most cases that's a great approach – but to reduce the risks to capital as investors move to retirement phase, externally managed strategies like the MMRS should be carefully considered.

The Plato Fund targets a return of 3% pa over the ASX 200 accumulation index and charges fees of 0.99% pa. By delivering access to the MMRS to retail investors it shows how investment technology can be used to overcome the limits of traditional products like annuities at the same time as helping retirees manage risk.

Dr Tony Rumble provides asset consulting services to financial product providers and educational services to BetaShares Capital Limited, an ETF provider. The author does not receive any pecuniary benefit from the products reviewed. The comments published are not financial product recommendations and may not represent the views of Eureka Report. To the extent that it contains general advice it has been prepared without taking into account your objectives, financial situation or needs. Before acting on it you should consider its appropriateness, having regard to your objectives, financial situation and needs.