PM Capital's patience with Asia pays off

Summary: PM Capital Asian Opportunities Fund is trading at a 15 per cent discount and its fund managers have a strong track record over the last eight years. The managers have been patient, buying into new positions on weakness over the last few months. Although some commentators talk down emerging markets, these portfolio managers point out that they are buying businesses, not markets. |

Key take-out: The fund plans to use education as a strategy to close the gap between share price and NTA, as well as continuing to perform well so rational market participants take notice. |

Key beneficiaries: General investors. Category: LICs. |

To shed some further light on a recent top up in the LIC model portfolio I sat down with PM Capital Asian Opportunities Fund portfolio manager Kevin Bertoli late last week to discuss the portfolio and the investment opportunities the team sees in Asia. You can also catch up on our original story on the fund here: PM Capital Asian Opportunities Fund looks beyond China, July 27.

The Asia-focused LIC PAF is currently trading at a 15 per cent discount to the latest reported NTA. The NTA of the portfolio is updated on a weekly basis to keep investors well informed of the value. Unlike LICs which report monthly there is very little guess work to be done here in the value of this portfolio.

The team members running this portfolio are experienced and have so far delivered returns in a difficult market by sensibly deploying capital gradually. They also have a proven track record over the last eight years of successfully delivering the strategy with an annualised return after fees to unit holders of 18.5 per cent. This exceeded the benchmark by 10.7 per cent pa.

To me it is simple. You have a fund manager trading at a 15 per cent discount to the current value of the portfolio. Since inception that portfolio has grown in value from $0.98 to $1.13 over the course of twelve months. The portfolio they are starting to replicate has achieved returns of 18.5 per cent over eight years. You can fluke numbers for one or two years. You're pretty lucky if you continue to fluke things over an eight year period.

MS: Performance has steadily grown since inception in a choppy market to say the least. What have been the main contributors to that performance?

KB: Firstly we've been patient with our cash. Over the last three to four months we've used general weakness in the market to buy into new positions and we were able to get in at very good levels. Donaco International (ASX: DNA) which is our largest position at 10 per cent has performed well over the last three months despite the general weakness.

We also had a good story with iProperty Group (ASX: IPP) with the takeover from REA Group. We have also had a good story in Wumart Stores Inc which increased 77 per cent after receiving a takeover offer.

These individual stock stories plus the cash and the timing of the deployment are what the performance can be attributed to.

On the cash holding did you top up in existing names or did you see further opportunities and themes developing?

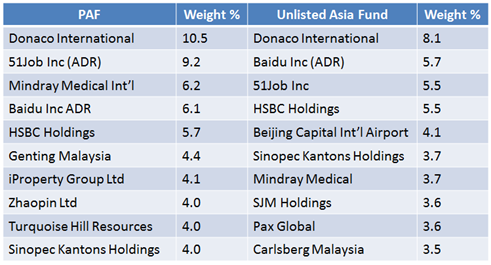

There have been a few names we have been keeping an eye on that are in our unlisted portfolio and we were able to buy into those recently as they reached more attractive entry points. The portfolio is now replicating the unlisted PM Capital Asian Companies Fund.

We topped up on some of our gaming related stocks and also increased our position in Baidu Inc ADR at $US145 and it is now trading close to $US200. We were also able to buy Pax Global Technologies, a payment technology business which we have been following closely for 12 to 18 months now. It had been sold down from $13 to high $6s. We took the opportunity to get in below $7.

For us it was individual investment ideas that drove the deployment of cash as opposed to new themes evolving.

PM Capital's LIC holdings starting to mirror the unlisted fund

There have been a number of market commentators talking down the forward looking prospects of emerging markets. When you hear this what are your thoughts as far as managing a portfolio in these markets?

Firstly we need to take a step back. We are not buying markets. We are not just buying and selling stocks. We are buying businesses. We take the time to look under the bonnet of businesses. If you look at our portfolio there is only one bank and there is one commodity company. Those two sectors are 50 per cent of the index and they make up less than 10 per cent of our portfolio. There are areas of the market that I am not participating in. I am not buying Chinese banks and Chinese coal companies because I think the outlook for those businesses is impaired over the next few years.

But there are businesses that do have good growth prospects over the next five to ten years. And it is the time when the commentators say, “the outlook for emerging markets is looking soft” that we get to take advantage of.

What are the biggest misconceptions people have when it comes to investing in Asia?

I think there are two. When it comes to investing in Asia people either want to or they don't. By that I mean you will see people buy emerging markets as one whole bucket of shares and not individual businesses. That's the big problem when it comes to people “investing in Asia”. They buy everything or they sell everything. Just like any market there are going to be businesses you want to own and ones you don't. We want to get people interested in the company stories. Not the short term one month PMI number or industrial production numbers etc.

Secondly, people just assume investing in Asia is investing in China. It's not. And our holdings show this.

What is being done about the gap between share price and NTA? What is going to close it?

Two things here. Firstly performance. We'll stick to our knitting and keep doing what we do. We've performed well in the unlisted fund and the LIC now has a good solid base to launch from. And over time what should happen in a rational market: participants should take notice of it and will close the gap.

Secondly and something we can have more control over is getting out there and educating people out there. Get them to buy the stock specific stories and the fund approach. Demonstrate to them our ability to rotate capital through a series of similar ideas as opposed to just buying the wider market. Because when people listen to the talking heads and become skittish about emerging markets they will be less inclined to sell out of PAF than one that is more closely replicating the market.

We could go out and start a buy back as a quick fix but that would just perpetuate a problem the LIC has and that is size. We have the options coming up next year and if they get exercised the size of the fund will double and this will help provide greater liquidity for shareholders.

But it comes back to education. We want people to consistently see us delivering the same message and we start to build a following of people who understand the philosophy and want to participate in our long term view of Asia.