Oil: Time to take another look

Summary: The question of whether we've hit a bottom or not for crude oil is unanswerable as temporary short-term factors and sentiment overwhelm the market. But none of these can be long-term influences so the greater probability is that energy prices restart an upward trajectory at some point. Big name long-term investors are throwing more money at the sector and would hardly take the risk if they expected a sustained large fall in commodity prices from this point. |

Key take-out: There is no rush but if your investment horizon is long enough and you can tolerate significant downside volatility, it might be a good time to research some beaten up energy stocks. |

Key beneficiaries: General investors. Category: Commodities, oil and gas. |

Inside the commodities market we're seeing some very intriguing price action. Indeed our colleagues at Barron's are openly wondering if we are at the bottom of the cycle (see today's piece Have oil and industrial commodities bottomed?). Certainly, the commodity that deserves intense focus just now is oil.

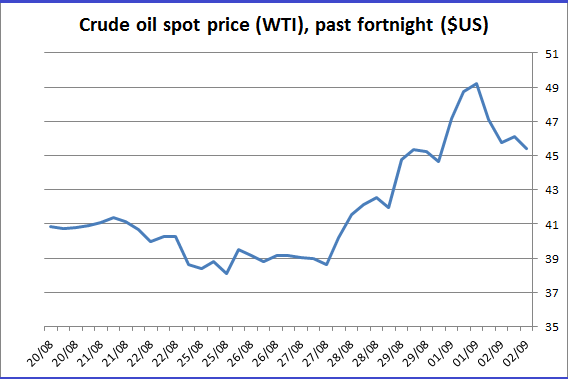

West Texas crude had surged by over 27 per cent from late last week to early Tuesday morning. That was the largest percentage gain since 1990. Sounds huge – and it is, although realistically the $US11 spike only took crude prices back to where they were in late July. That may erase all the losses of that month, but we can't overplay the move.

As oil prices fell just over 8 per cent overnight (Tuesday September 2), volatility is certainly elevated. August alone saw about six or seven trading days with moves over 4 per cent, while the last four trading sessions have been around 6 per cent or more.

Chart 1: Crude oil spot price

Source: Bloomberg, Eureka Report

The difficulty investors have in trying to make sense of this price action is that there doesn't appear to be one clear catalyst that has driven moves in any direction. And certainly nothing of substance.

As best as I can tell, it seems to be a combination of generally small events such as the US Energy Information Administration's decision to change the way it estimates oil production. This one action had the effect of reducing the amount of oil that the US produces by about 13.2 million barrels. Gone, just like that. In some cases, average daily production was revised down, by 150,000 barrels per day.

Similarly, there were rumours doing the rounds that Saudi Arabia had had enough of low prices and was seeking to talk to other oil producing nations, both within and outside OPEC, in order to set a ‘fair' price for oil. If there is something in that, then moves to the upside could be substantial. The problem is we just don't know if there is any substance to those reports or not. Last night's slump for instance was driven by rumours that the Saudis weren't going to talk to anyone.

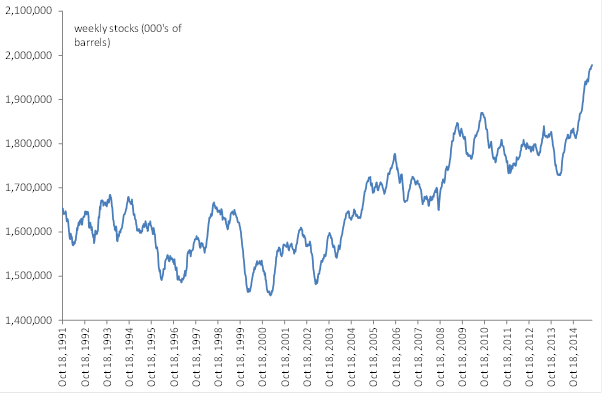

Overlaying all of that is this fear over China and data showing that inventories of crude in the US are rising. And it's true US inventories are surging – just look at chart 2 below.

Chart 2: US crude stocks surge

Source: Bloomberg, Eureka Report

Yet to show you how overplayed this kind of news flow is, consider that since the peak oil scare of 2007-08, the surge in US petroleum stockpiles represents only about two weeks' worth of consumption. The US consumes approximately 19 million barrels per day. Then consider that the weekly fluctuations that seem to drive, or at least contribute to, these huge moves in crude oil prices a represent half a day's worth of consumption at most. Indeed, much of the time these moves actually only represent an hour or two worth of crude consumption. And yet the volatility that kind of information can unleash is remarkable. It goes to show you just how crazy markets are at the moment.

Against that backdrop, the question of whether we've hit a bottom or not for crude is unanswerable. Some analysts are talking a return to $US20 and hand on heart no one can argue against that. At least as a short-term phenomenon. Namely, that's because it is temporary short-term factors and sentiment that are overwhelming the market at the moment. This includes the rally in the US dollar, the dramatic outflow of funds from the commodities sector (derivatives), and a push by western governments to ensure lower commodity prices. Not to forget heightened anxiety over China.

None of these can be long-term influences though, which is why the greater probability is that energy prices recommence an upward trajectory at some point. Admittedly investors may have to wait some time. For a start, the Fed don't seem to know what they are doing, and these relentless fears over China are unlikely to abate over the next six months, perhaps longer.

Yet at some point they will die down. The Fed may hike, taking the US dollar even higher, but not too long after they hike, every other central bank around the place will start raising rates too. Noting that the US dollar is at a decade high or more, close to two decade highs in some cases, the US dollar will likely weaken over the next few years – providing some support for commodity prices. Similarly, few dispute that while China is engineering a slowing of its economy now, its long-term growth prospects are strong – as are the rest of the emerging markets.

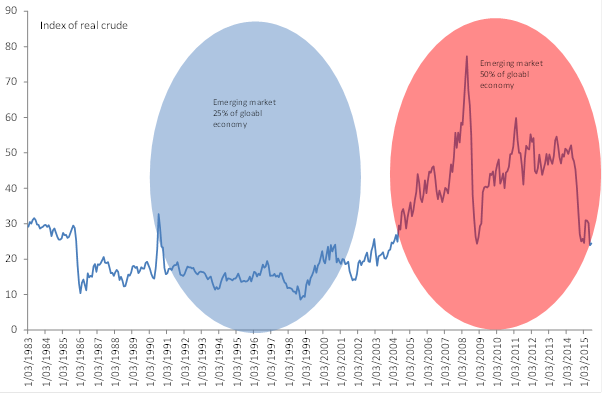

Chart 3: Real crude prices weak

Source: Bloomberg, Eureka Report

Against that backdrop real (inflation adjusted) crude prices now are very weak. They're back down to where they were before the pick-up in the emerging market economies (almost). Of course, in the late 90s/early 2000s, the emerging markets made up only 25 per cent of the global economy. These days it's 50 per cent and growing rapidly.

Now given the emerging markets make up 90 per cent of the global population, that 25 per cent jump (from 25-50 per cent) represents a huge lift in crude consumption. Real crude prices shouldn't be where they are now on the fundamentals and are unlikely to stay here. Especially when, and contrary to popular mythology, there is no global supply glut of crude.

So for investors, it all comes down to your investment horizon. Energy stocks like our large miners are unloved and have taken a beating. I can't say this is the bottom. Yet on a long-term view, they look to offer tremendous value. Some stocks for instance, like Woodside, aren't too far off their GFC lows.

More money is certainly being thrown at the sector and by some big name long-term investors. Warren Buffet for instance recently disclosed a $US4.5 billion stake in a refiner called Phillips 66. That purchase compliments existing oil assets Buffet holds – namely in transport and the like. Given his investment philosophy, most interpret Buffet's move as a vote of confidence in the sector – at the very least in end use energy consumption.

Another famous investor, Carl Icahn, has also placed a large vote of confidence in the energy sector, taking an 8.5 per cent stake in a firm called Freeport-McmoRan. Now admittedly Icahn tends to invest in companies that he can clean up and release value. At the same time though, an investor would hardly take that risk if they expected a sustained large fall in commodity prices from this point.

So if your investment horizon is long enough and you can tolerate significant downside volatility, it might be a good time to research some beaten up energy stocks. There is no rush certainly, but when certain sectors or stocks fall foul of market sentiment, and appear to diverge form long-term fundamentals, it's often a good time to pick them up.