No longer unstoppable? Coles and Woolworths brace for battle

Summary: Australian supermarkets could follow the traumatic path of UK retailers, as overseas discounters open local stores and gain market share. Aldi and Costco pose a threat to the sales of Woolworths and Coles. If rival discounter Lidl were to come to Australia, the situation could become worse for the majors. |

Key take-out: Despite differences between the Australian and UK grocery markets, the spread of discounters is likely to affect the majors' margins. |

Key beneficiaries: General investors. Category: Shares. |

The major supermarkets' duopoly may appear unstoppable, with Woolworths and Wesfarmers-owned Coles regularly criticised for using their market power to pressure farmers and suppliers. But this concentration of power is changing. Changing consumer preferences are forcing retailers to respond, while German discount retailer Aldi has continued its aggressive expansion throughout the east coast and is set to roll out more stores across the country.

The traumatic experience of supermarket chains in the UK may offer warning signs for local retailers, which have traditionally not been strong yield stocks themselves. Share prices for the UK majors have been falling, with Tesco sliding 50% over the last 12 months and Sainsbury dropping 44% over the same period. These “high street” retailers – along with Morrison and Asda – have been losing market share to both Aldi and rival discounter Lidl.

Tesco has its own particular headwinds, after admitting to the market that it had made a £250 million accounting error and would have to delay its earnings report.

The remarkable feature of the rout in British listed supermarket shares is that they have long been a backbone of portfolios for conservative investors. Even the world's “greatest living investor” Warren Buffett had not just been an investor in Tesco but had been accumulating shares in the supermarket group in recent times. Buffett has now called his Tesco investment “a big mistake”.

For Australian investors the big question is …could it all happen here? On closer inspection there are particular issues at UK retailers – especially the allegedly overstated profits at Tesco. But on a more fundamental level, if a seemingly unstoppable supermarket duopoly can be brought down by new market conditions in the UK, the Australian situation must be at least under question.

The majority of Australian share investors are likely to have investments in either Wesfarmers (currently a Sell on Eureka Report stock recommendations) or Woolworths (currently a Hold on Eureka Report stock recommendations) – the two stocks heavily dominate the listed retail sector.

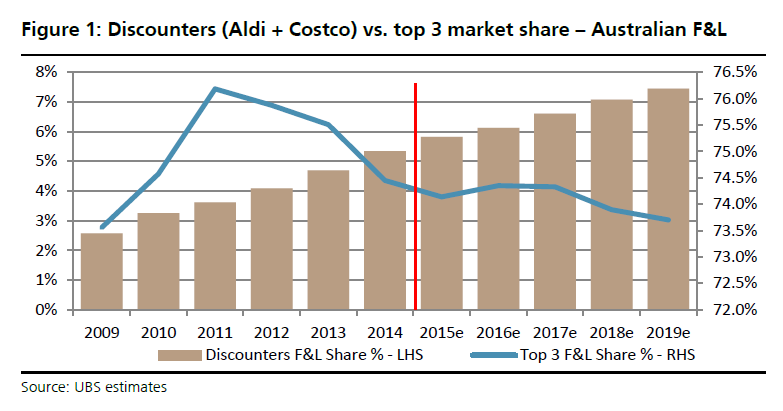

UBS Australia analyst Ben Gilbert compared the environment for supermarkets in the UK with Australia and found reasons to worry. “We are becoming more concerned about the threat that the grocery discounters (Aldi and Costco) present to both sales and margins of the major supermarket chains, namely Woolworths, Coles and particularly the independents,” he wrote in a recent research note.

“The Aldi and Costco models are highly efficient, offer compelling value to customers, and are very hard for the major supermarket chains to compete against. The threat is further compounded by the risk of potential new entrants (Lidl and Amazon Fresh),” Gilbert wrote. Based on the UK situation, the threat to Australian supermarkets' margins is greater than the threat to sales, as traditional chains make heavy investments in price to compete with their discount rivals, he wrote.

Gilbert warned the discounters' business models are “virtually unstoppable” given their compelling value to consumers and high level of efficiency.

UBS conservatively estimates Coles will lose $313 million in sales per year to Aldi alone over the next five years, equivalent to a 1.2% impact on annual like-for-like sales. It estimates the hit to Woolworths' like for like sales will be slightly less in percentage terms, at 1.1%, or $352 million per year over the same period. “Traditional chains need to build trust,” Gilbert writes. “We believe Coles is doing the best job in Australia, particularly around price.” But all major supermarkets will need to invest in price, staff, marketing, technology, formats and systems, he says. He notes Woolworths' greater than forecast capital expenditure in recent years.

At Morningstar, senior equity analyst Tim Montague-Jones says that Woolworths' larger scale gives it a “slight competitive advantage”. He believes both the majors are rolling out stores at a similar magnitude, both are focusing on their fresh produce offer, both are using data to gain insights and both are concentrating on home brands to compete with Aldi. “It's a very competitive marketplace. It definitely favours a retailer with a bigger scale.” But he says both the majors have a “phenomenal” scale advantage, which gives them cost advantage, adding he expects them to continue performing well as independent supermarkets and specialty retailers falter.

Meanwhile, Platypus Asset Management chief investment officer Don Williams says: “The outlook for both of those companies is as tough as it's ever been.”

Deutsche Bank research points out a key difference between the Australian experience and the changes in the UK. In the UK, there are two discounters, which invest in price not only to compete with the major chains, but also to compete with each other, which in turn increases the price investment that the majors need to make in response, analyst Michael Simotas says. If Lidl were to launch in Australia, it would need to spend a number of years building scale before making significant price investment, and the group would likely find it difficult to obtain sites, given Aldi has already spoken of its challenges in buying appropriate property, he says. Simotas says Coles and Woolworths should be able to gain market share for another five to 10 years, given the differences between the two countries.

Another difference in the UK is the presence of premium supermarkets Waitrose and Marks & Spencer, Deutsche Bank says. Major supermarkets in the UK have been squeezed at both ends – by discounters and by premium providers. In Australia, Coles and Woolworths may face competition from boutique specialty stores, but not from major high-end chains. “David Jones tried it [a premium grocery offering] and it didn't work – they couldn't make money,” Morningstar's Montague-Jones says.

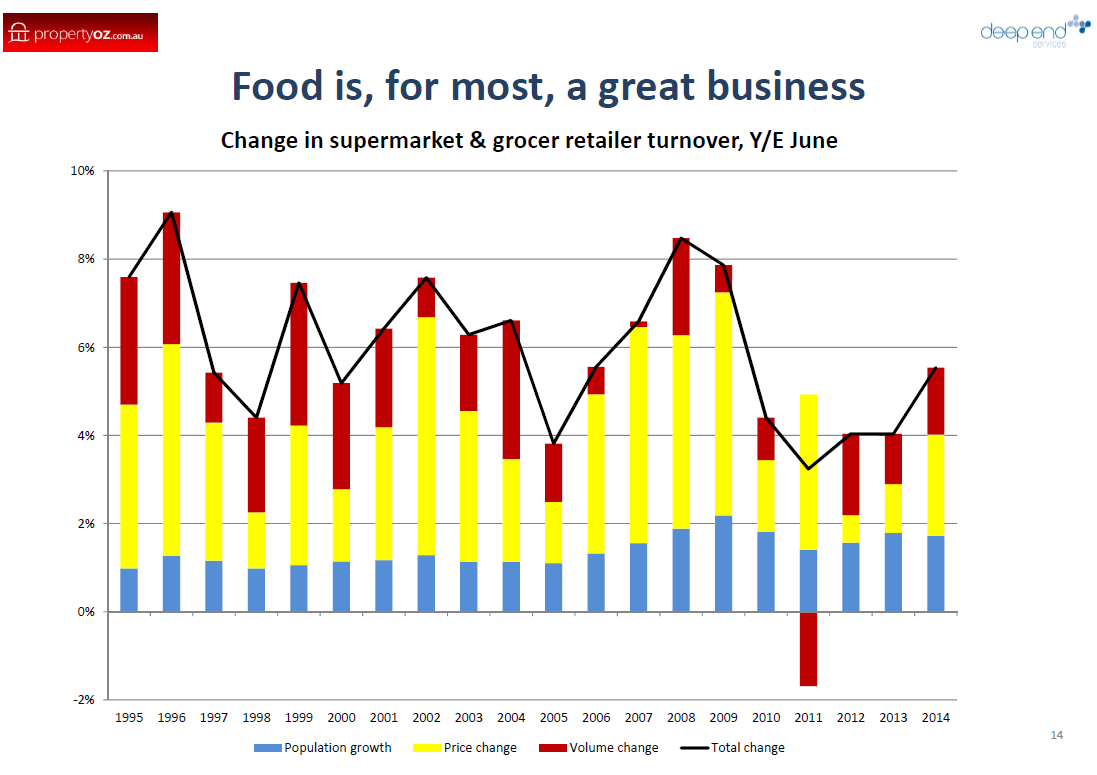

Yet the major Australian supermarkets have consistently reported both price growth and volume growth over the past 20 years, according to Justin Ganly, managing director of retail and property consultancy Deep End Services.

As Ganly points out, just one year out of the past 20 showed a volume decrease, and that was related to a shortage of bananas in 2011 after a cyclone hit north Queensland.

Source: Deep End Services

Another advantage for overseas retailers keen on expansion is that Australia is a relatively stable economy, compared to emerging economies in Asia, says Deloitte partner and national leader for retail David White. “There certainly is room for other grocery retailers in Australia,” White says. “The fact Aldi has been successful and gained customers will be a good sign for someone like Lidl to think about coming into Australia.”

Analysts watching the Australian market estimate Aldi's market share at between 5% and 10%, and the German retailer has just announced a few days ago plans to open up to another 130 stores in Western Australia and South Australia in coming years (http://www.afr.com/p/business/companies/aldi_prepares_for_competition_not_dRM2UI70RrJv3e9Z52um1J). They also say the impact of Costco should not be underestimated, while speculation has been swirling that Lidl could open locally in coming years.

Juggernauts Woolworths and Coles may not be unstoppable after all. The UK experience suggests that the presence of one discount chain is enough to eat into the margins of the majors. And if two discounters establish a foothold in the Australian market, competing with each other, this could drive down prices even further for everyone else. Two sharemarket darlings could well fall out of favour.