Murray inquiry: Why the banks thank Murray

Summary: APRA has until the end of next year to make sure our banks are “unquestionably strong” but the regulator hasn't defined what “unquestionably strong” means. APRA has also said international comparisons shouldn't be the only benchmark for measuring the strength of our banks. The banks have core capital of twice the minimum requirement, with recent capital raisings to boost that further, and score highly on measures such as asset quality and management quality. |

Key take-out: Perhaps the banks are closer to being “unquestionably strong” than the market has currently priced. |

Key beneficiaries: General investors. Category: Bank stocks. |

The government's response to the Financial System Inquiry was disappointing. It's not that the response contained anything new – but that's the point. It didn't contain anything new and in fact endorsed the current regulatory approach and all the uncertainties that involves.

On the face of things, investors have at least two more years of not really knowing what it is that regulators want. The government has washed its hands and outsourced all decision making to a bureaucrat. Never a desirable situation.

Having said that there's a good chance that all this negativity on the banks will quieten down some – at least for the next six to nine months. Largely that's because APRA has until the end of 2016 “to take additional steps to ensure our banks have unquestionably strong capital”. As vague as that might sound, it allows (if APRA should choose) a decent time period for banks to raise whatever additional capital they might need organically. That is, through retained earnings and dividend reinvestment.

Now admittedly worrying questions on capital still linger. The big problem investors have got is that we just don't know what APRA is thinking exactly. The regulator hasn't defined what “unquestionably strong” is and no one else seems to know. Not even David Murray who said this week, in response to a question on whether banks needed more capital, that there were “many moving parts” and that it was “not possible to tell if they need more capital.”

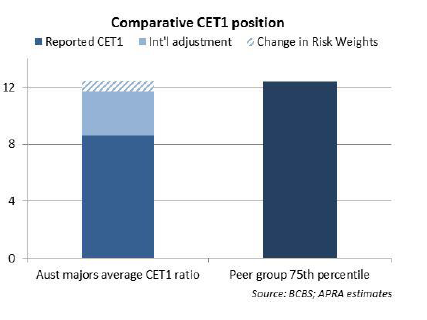

At this point, APRA appears content that recent capital raisings bring the big banks just within the top quartile of global banks (when it comes to tier 1 capital). The bigger question is whether they'll be expected to stay there, and if so, whether the bottom of the top quartile would be sufficient.

Chart 1: Banks' CET1 position

If it isn't, and banks are expected to stay “comfortably within the top quartile over the longer term”, then they need to raise a lot more capital. As at June 2014, APRA reckoned that the banks needed roughly 2 per cent in additional capital. So far they've done roughly three-quarters of that, so on a strict interpretation, they've still got a long way to go.

My read of things now though is that it's very unlikely APRA will require banks to remain in the top quartile.

Firstly and most important, it's an unreasonable goal. The banks that should be in that top quartile are the big global banks. The Citis, Goldmans and JP Morgans of the world. As big as they are, Aussie banks simply do not come close.

Secondly, APRA's own commentary suggests this won't be the long-term target. APRA's chairman, Wayne Byres, said in a recent speech that “we don't intend to tie ourselves to a precise percentile”. That's pretty clear. He went on to say that “we don't think international comparisons should be the ultimate benchmark against which unequivocally strong is judged”. One reason for this is because there is no universally accepted capital benchmark. Another is because APRA wants to be the ultimate judge as to what capital is required. That won't be the case if they are tied to a global benchmark.

On questions of capital then, and how much the banks will need to hold, “what ultimately counts” in the words of APRA's chairman, “is how much capital a bank has over and above its regulatory minima”. That is the domestically determined minimum requirements. As at June 2-15, APRA said that the banks had CET1 capital (core capital) that was twice the minimum requirement. Recent capital raising will boost that even further.

That the banks have to raise more capital is clear, but given APRA's stance on the limitations of international comparison and the primacy of domestically set capital ratios, might it be the case that the banks are much closer to being “unquestionably strong” than the market has currently priced?

Maybe. Especially when APRA's chairman reckons that “an unquestionably strong bank requires more than just plenty of capital. In banking, asset quality, liquidity and funding, earnings and management quality are also highly relevant.”

This is good news for Australia's banks because on each of these measures they score very highly indeed. Asset quality for instance is very high.

- Loan impairments are very low, around 0.5 per cent of total loans.

- Loan to value ratios are falling for new loans. Only one quarter of new loans issued are at an LVR of over 80 per cent. Average LVRs for total loans outstanding are approximately 30 per cent.

- On average, households have a mortgage buffer – amounts in offset accounts or redraws – of about two years scheduled repayments and that is rising rapidly.

- Commercial property exposures, as a percentage of total bank assets are low. Impairments in this space are at 0.6 per cent.

Other than that no one disputes that management quality at the banks is high and of course, Australian banks are some of the most profitable in the world. Similarly, as far as banks being able to ensure liquidity (being able to convert high quality assets to cash quickly) this has been taken care of by the Reserve Bank who said they'll provide the cash banks need for a fee.

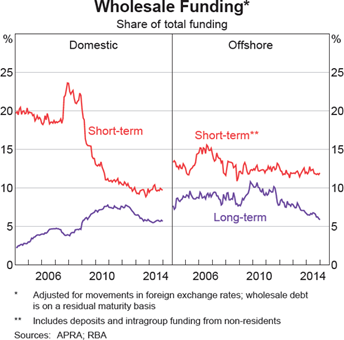

That just leaves funding. The concern here is that our banks are reliant on offshore funding for their operations, but this actually isn't true. Offshore funding in the wholesale market accounts for only 17 per cent of funding requirement for banks, down from about one-quarter in 2006. Domestic deposits account for 60 per cent of all funding which is up sharply from 40 per cent back in 2007.

Chart 2: Offshore funding is only a small proportion

In any case, if anyone is truly worried about the willingness of our banks to access global markets in a time of crisis, it's not the amount of capital that matters. The single most important factor will be the health of the government's balance sheet. If global investors see that the government has low debt and at worst, small budget deficits, then they will happily lend to its banking system. The whole financial system – the acceptance of money even, rests on one thing only: Confidence. That's why the balance sheet of the government and banks are inseparable, no matter how much regulators would like to try and change that. They can't.