Listed or unlisted infrastructure: What's better?

Summary: More investors are recognising the benefits of holding infrastructure assets in their portfolio.

Key take-out: Diversity, liquidity and volatility set listed and unlisted assets apart.

The road to infrastructure investing has become a lot easier for retail investors in recent years, with a plethora of listed shares and unlisted funds now available to those wanting exposure to this asset class.

Indeed, more self-managed super funds and private investors are recognising the attraction of infrastructure assets such as airports, toll roads, regulated utilities including electricity, gas and water companies, as well as ports and railway networks.

These are typically privatised assets, sold off by either national governments in Australia and overseas, or by state governments and territories.

The attraction is that infrastructure assets provide investors with relatively predictable and stable cash flows over the long term, which due to contractual arrangements are often set to rise in line with inflation. As such, these types of assets are less prone to broader market volatility.

But a question for all investors is whether it's better to access infrastructure via listed companies on the Australian Securities Exchange, or whether a better and less volatile course is through an unlisted infrastructure fund?

There are different schools of thought on this issue.

“It is possible to invest in infrastructure through direct shares or a managed fund, giving investors access to the advantages that this asset class offers, including a very attractive risk return profile with strong growth upside,” says 4D Infrastructure Chief Investment Officer Sarah Shaw.

“In fact, investing in listed infrastructure may be a better option for retail investors than an unlisted direct exposure.”

The reason, says Shaw, is that investing in listed infrastructure gives access to the same underlying asset profile as an indirect or unlisted exposure.

Furthermore, both listed and unlisted investing employ the same valuation techniques, and there is regular movement of assets between the listed and unlisted space.

The main differences are in how an investor owns that asset profile, or how they gain exposure to the fundamental assets.

Investors in listed investments, rather than unlisted, generally benefit from:

- Greater diversity: If an investor is gaining exposure through a fund of listed equities, they will be gaining exposure to a diverse stock portfolio covering different sectors and demographics.

- Greater liquidity: The listed sector has a shorter time to invest or divest. Investors in unlisted funds can face potential problems when trying to liquidate their holdings, although some funds have sufficient capital inflows to meet withdrawal demands.

- Less acquisition risk: Direct investment needs intense due diligence, requiring a much larger team, and ultimately leads to greater portfolio concentration risk and limits the investor type.

- Greater in-cycle volatility: As listed assets are re-priced daily, there is higher in-cycle volatility. However, this can present opportunities for active investors to take advantage of market volatility.

But Nicole Connolly, Executive Director of funds management group Infrastructure Partners Investment Fund, says market volatility is one of the key reasons why unlisted infrastructure is a better option.

“Infrastructure, and particularly unlisted infrastructure is attractive due to its typically stable, reliable returns and low correlation to equities,” she says.

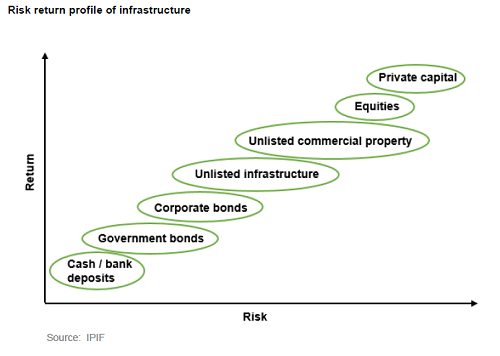

“Infrastructure in a portfolio sits between government bonds and equities in terms of risk return, making it an excellent portfolio diversifier.”

Unlisted infrastructure funds also tend to have exposures to a broader spread of assets, some of which are not available through listed securities.

For example, investors can readily access Sydney Airport and Auckland Airport shares on the ASX. However they can gain a much broader exposure to airports through unlisted funds that have indirect holdings in Melbourne, Perth, Brisbane, Adelaide, Launceston and other privatised domestic airports.

Another benefit of many unlisted funds is their exposures to offshore infrastructure assets, in Asia, Europe and the US. These assets are much harder to access through listed holdings.

Connolly says unlisted infrastructure investments account for between 7-12 per cent of major institutional investor portfolios, with the Future Fund having around 7 per cent ($11.7 billion) allocated to infrastructure and Australian Super 12 per cent.

Unlisted returns have historically returned around 9 per cent per annum, which is more than the yields from Australia's top dividend stocks of the big four banks and well above the rates of term deposits.

“Couple this with the recent uncertainty over the future of franking credits and dividends and it is little wonder that more investors are increasingly considering the predictable and consistent returns of unlisted infrastructure,” Connolly adds. “All without the associated market volatility of listed investments.

“The key is to determine which assets and projects will provide the greatest, and most consistent, returns,” she says.

“We actually think unlisted complements listed infrastructure. We don't think it's one or the other, but there's a place in a portfolio for both listed and unlisted infrastructure.”

Meanwhile, 4D Infrastructure's Shaw says active management is particularly important when investing in infrastructure to position for all points of a macro economic cycle.

“Utilities meet basic needs and are largely immune to macro cycles, making them an attractive defensive, resilient asset class in depressed markets.

“By contrast, user pay assets (toll roads, airports, ports and rail) are positively correlated to macro growth and represent a very attractive investment proposition in buoyant macro environments.

“Active management of these two infrastructure sub-sectors aims to smooth the volatility of the investment, again comparing favourably to a general index or ETF (that generally favours cyclicals) or direct shareholdings which have concentration risk.”