LIC spotlight: AMP Capital China Growth Fund (AGF)

Summary: As China's growth shifts from exports and investment to consumption and services, one LIC is encouraging investors to look beyond Australian resources stocks when it comes to China exposure. The AMP Capital China Growth Fund is focused on growth rather than income and its largest holdings include consumer companies focused on cars, beverages and media, as well as financial stocks. |

Key take out: The manager of this LIC is bullish on China's prospects as a way for Australian investors to diversify and gain exposure to growth. |

Key beneficiaries: General Investors. Category: Shares. |

China's surprise interest rate cut last week is the best economic news from the country in some time. The People's Bank of China cut the one-year lending rate by 40 basis points to 5.6% and the deposit rate by 25bp to 2.75%, and the move is expected to help stimulate growth. The cut comes soon after the conclusion of the China-Australia Free Trade Agreement, which will provide opportunities for Australian firms to export services and agricultural products, and also follows the opening of the Hong Kong-Shanghai Stock Connect, which allows foreign investors greater access to shares in Chinese companies (see Investing in China just got easier). For Australian investors, China is well and truly in the spotlight at the moment.

For AMP Capital, China has been a focus for some time. The firm was approved as a Qualified Foreign Institutional Investor in 2004, which allows for direct investment in Chinese shares. It launched its listed investment company, the AMP Capital China Growth Fund (AGF), in 2007. The group's Head of Asian Equities, Patrick Ho, is based in Hong Kong, where he manages the LIC and two other Asia-focused funds.

Ho warns that it's time for Australian retail investors to rethink their exposure to China as the country's growth shifts from exports and investment to consumption and services. His concerns come in the context of a steady fall in the iron ore price from above $US130 a tonne in January to below $US70 this week as supply from major producers continues to outstrip demand from Chinese steel mills, as well as an expansion in the Chinese middle class.

The problem is not that Australian retail investors are not interested in China – they already like the country and its strong economic growth. “Whenever I have a chance to visit our Sydney office, I get quite a bit of requests from media and local investors who would like to know more about the latest status in China,” Ho says. “China is their largest trading partner and most of the commodities like iron ore or coal are exported from Australia to China. Besides the domestic economy, China is key for investors to look at to see how the Australian economy will go.”

But he says a shift in thinking is required. Australian investors often have local resources companies in their portfolios, particularly major exporters BHP Billiton and Rio Tinto. “They argue they already have China exposure,” Ho says. “It could be true in the last two decades. Now, there is a bit of decoupling.”

As the growth drivers for China change, Australian investors can benefit by investing in Chinese consumer companies, he says. “We try to keep educating Australian investors that they might have to adjust.”

Ho has been working on this education process for some time, including penning an article for the ASX newsletter in February 2013 warning investors to look beyond commodities. “The shift from the consumption of basic necessities to discretionary products and services has sparked another round of growth in China,” he wrote, saying this “could offer Australian investors a diversified investment with an attractive upside”.

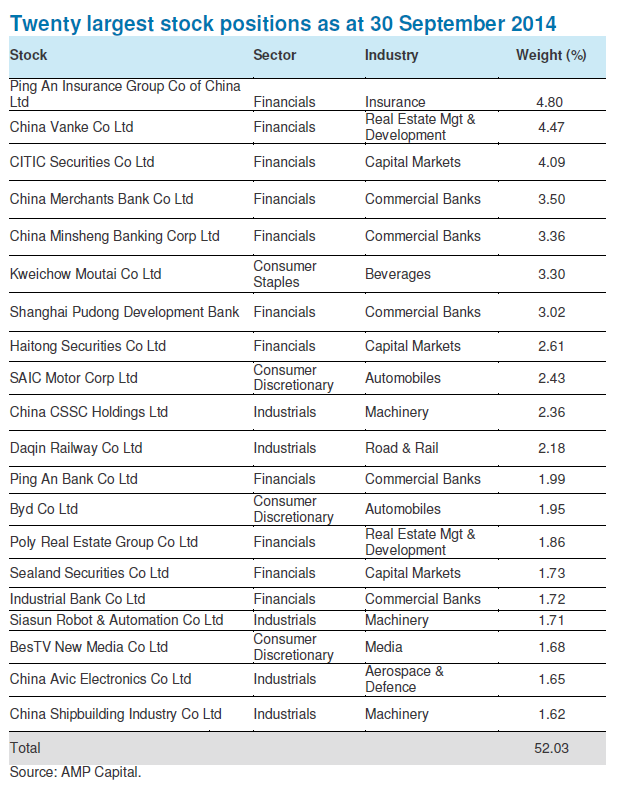

The fund's 20 largest holdings include consumer companies focused on cars, media and beverages (see Surprising news from the international investing experts). It also has positions in several banks and an insurer, as well as machinery and railway groups.

Balancing growth and price

Ho says the fund is focused on fundamental analysis, trying to pick stocks or sectors that offer attractive growth, at the right time. He says the danger in picking growth stocks is that it's possible to pay too much because the market has already priced in the growth. He aims to strike a balance between price and growth opportunity – for example, a stock on a price-earnings ratio of 20 times could still fit into the fund's investment philosophy if it has further potential.

Ho points out that equities and the real economy are growing hand in hand. Investors from around the world see their home market growing at a rate of only 1-2% and choose to invest in China and other parts of Asia due to the higher growth prospects. He says Australian investors used to be even more focused on their home market as the dollar was elevated due to the commodity rally, but have paid China more attention recently as the currency has fallen.

Ho says he has a relatively stable outlook for China's growth going forward, despite the frequent airing of concerns about a property bubble or a hard landing. GDP growth jumped after a RMB 4 trillion stimulus package to respond to the GFC, but has since been normalising, and is reaching more of an equilibrium at around 7%, which is “still very decent”, he says. The Chinese market has seen a derating process because of economic uncertainty, but if this uncertainty is removed valuations could be rerated as people become more confident, Ho says.

Weighing up performance

AGF does not aim to pay regular dividends and is focused on long-term capital growth through investing in China A shares, or shares in Chinese companies that are listed on the Shanghai or Shenzhen stock. Asked about the new Hong Kong-Shanghai Stock Connect program, which will open up access to Chinese shares for overseas retail and institutional investors, Ho is quick to point out that the deal is not only about foreigners investing in China. A significant part of the deal will involve Chinese investors buying shares in Hong Kong-listed companies. In addition, all the settlement for the program will be done in renminbi, as China pursues the internationalisation of its currency, he points out. But Ho says although it is too early to see any trends yet, the program is likely to give foreign investors more experience in China.

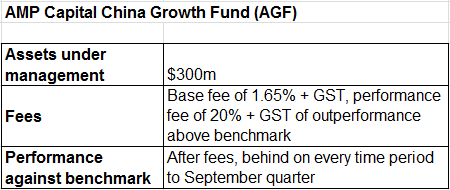

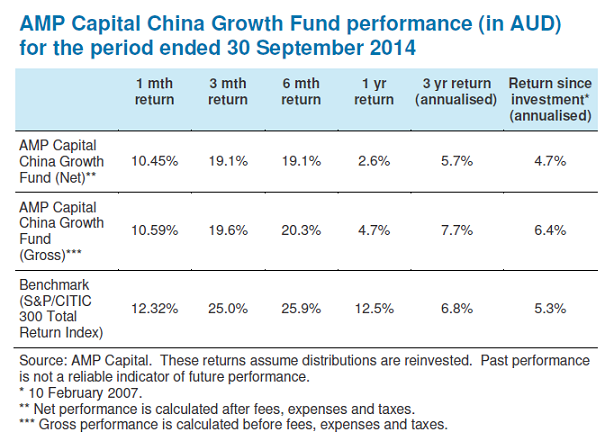

The fund's most recent update shows its performance has lagged its benchmark after fees when measured until the end of September, although it beat the benchmark before fees over the medium and longer term. Since listing in February 2007, the fund's returns have not been stellar, at 4.7% annualised net of fees, compared with 5.3% for the S&P/CITIC 300 Total Return Index. Ho says the fund has faced some headwinds this year, as improving sentiment has led to a lot of stocks running ahead of valuations. “Probably our stocks will be going to catch up with that, so I'm not that worried.” For the year ending June 2014, the fund performed worse than its benchmark, although for the year to June 2013, the fund outperformed.

Similarly, the fund has been listed for close to eight years and has assets under management of $300 million. Ho manages a total of $US1 billion across AMP Capital's three Asia-focused funds.

But Ho remains bullish on China's prospects as a way for Australian investors to diversify and gain exposure to growth. “We have been busy talking with media and investors to share our view on China,” he says. “We have a bit more of a positive outlook than other investors.”