Learning to live with cheaper oil in the Middle East

The steep decline in global oil prices, by 55 per cent since last September, has changed the economic dynamics of oil exporters in the Middle East and North Africa.

Our update of the Regional Economic Outlook, released yesterday, shows that these countries are now faced with large export and government revenue losses, which are expected to reach about $US300 billion (21 per cent of GDP) in the Gulf Cooperation Council and about $90bn (10 per cent of GDP) non-oil exporters in the region.

Where prices will eventually settle is, of course, uncertain, making it hard for policymakers to gauge how much of the bane is temporary in nature and what share of it they should expect to last.

In the short term, most of the oil exporters have the ability to draw down some of their accumulated financial reserves and so mitigate the impact of lower oil prices on economic activity and growth. However, with a more constrained fiscal outlook over the next few years, oil exporting countries would need to adapt progressively to new realities. Specifically, they would need to adjust their spending gradually and advance energy subsidy reforms.

This means that the growth models of the past decade that were anchored in rising government spending may no longer be sufficient. Instead, the private sector will need to become a much more self-sufficient engine of growth and jobs.

New realities

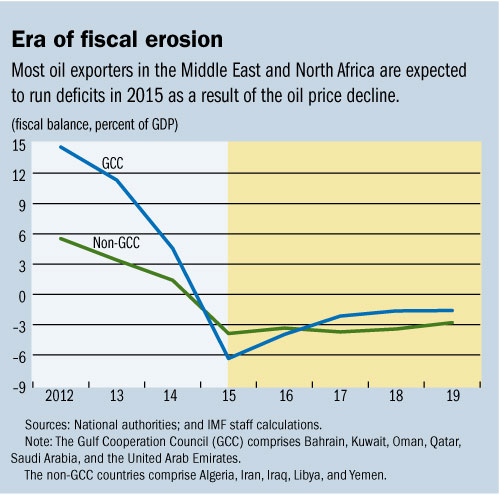

The oil price decline is expected to significantly erode fiscal positions across the region. Except for Kuwait, all countries in the region are expected to run fiscal deficits in 2015 (see chart).

The Gulf Cooperation Council fiscal surplus (4.6 per cent of GDP in 2014) is now projected to turn into a deficit of 6.3 per cent of GDP in 2015 -- a downward swing of about 11 per cent of GDP.

Fortunately, most oil exporters have large buffers in the form of foreign assets. These countries are generally expected to reduce the growth of government spending this year, but in a measured way.

Since the overall pace of adjustment is measured, we expect that countries will be able to avoid a very sharp negative effect on growth. We expect growth in the region's oil exporters to reach 3 per cent this year, somewhat higher than last year but still nearly one percentage point lower than we projected last October.

Need to change course

The region's oil-exporting countries are faced with a situation where their buffers are now eroding at varying speeds. Therefore, most countries will need to re-assess medium-term spending plans and, if lower oil prices persist, they will need to gradually adjust to new realities in the global oil market. Spending will need to be better prioritised to ensure it is efficiently meeting social and economic development objectives and options for increasing non-oil revenues should be considered.

Energy pricing remains an issue. The new fiscal realities facing most oil exporters make it all the more urgent to tackle the underpricing of energy products, which persists despite the fall in international oil prices. A number of countries have now started this process, and that is encouraging.

Looking ahead, government spending will likely be constrained for a number of years. Meanwhile, unemployment remains the biggest challenge for the region. High and sustained growth will be needed to meaningfully create jobs and raise people's incomes.

The growth model of the last decade that was anchored in rising oil prices and government spending will no longer work. Instead, countries will need to further diversify their economies to reduce reliance on oil revenues and reorient incentives toward export-driven production of goods and services.

This will require setting up reforms, especially in areas of the business environment, governance, education, and trade integration to enable the private sector to flourish and become a much more self-sustaining engine of growth.

Similarly, in many countries it will be important to enable nationals to participate more in the private sector labour market to avoid pressures on governments to play the role of employer of first and last resort -- a role they will find much harder to maintain during an era of lower oil prices.

This article was first published at iMFdirect. Reproduced with permission.