Is Canberra prepared for a China carbon slowdown?

The government is finding itself in the rather uncomfortable position of feeling a bit like former Labor treasurer Wayne Swan. It appears that, in spite of apparently choosing highly conservative assumptions about likely budget revenue, the government faces the prospect of having to make significant downgrades in expected revenue inflows due to a large slide in the price of iron ore and coal.

As the Parliamentary Budget Office illustrated in a report released recently, the outlook for the government budget is built on a series of assumptions of what is believed to be likely to occur into the future. But these can turn out to be wrong for a variety of reasons (as we are now seeing) which can have a material impact on the government budget. For that reason we need to actually prepare for a variety of potential plausible scenarios, not just one single outcome.

In relation to our current predicament, China is taking everyone by surprise yet again, but this time it's on the downside for the mining sector. It is now shifting from a focus on growth via industrial sector expansion and construction activity, towards an emphasis on services and greater concern for the quality of economic expansion. In other words, expansion of the economy that doesn't come with so many bad side-effects in terms of damage to people's health and a bunch of buildings and industrial plants for which there is insufficient demand.

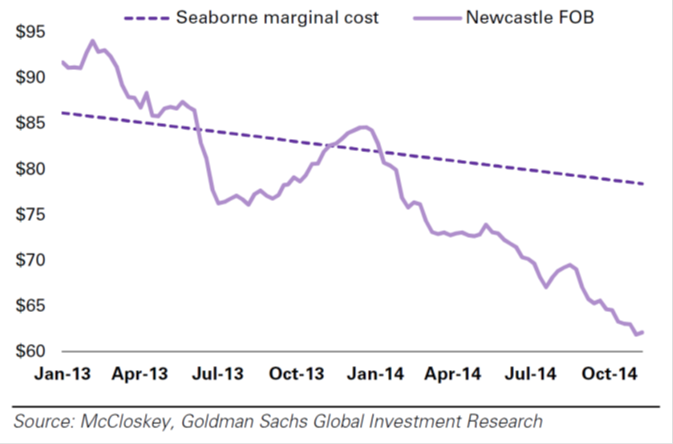

This sudden shift in China's demand for basic commodities has led to a dramatic slide in the price of thermal coal. As the slide below from Goldman Sachs commodities analyst Christian Lelong illustrates, coal producers haven't been able to reduce costs (dotted line) fast enough to keep up. In spite of Queensland Premier Campbell Newman's plans to throw hundreds of millions of taxpayers dollars at even more thermal coal supply from the Galilee Basin, something has to give and it will be cutbacks in supply.

Figure 1: Thermal coal prices (Newcastle FOB) declining faster than coal production costs ($US)

Ominously for the coal sector, our China Spectator editor Peter Cai writes in a column we've published today that the Chinese Government's National Reform and Development Commission is looking to use the international imperative of containing carbon emissions to help force economic reforms within the Chinese economy that will make it more efficient.

Given how badly Australia's Treasury has been surprised by the sudden turnaround in the demand for Australia's commodities, and the recent US-China carbon cutting announcement, a recently released paper from the think-tank Beyond Zero Emissions should provide pause for thought – it could get a whole lot worse.

Author of the report, Dr Stephen Bygrave, is a long-time Canberra public servant from the SES ranks. He has been close to a range of major energy and climate policy initiatives over the years and appreciates how economic forecasts play a pivotal role in influencing bureaucratic thinking.

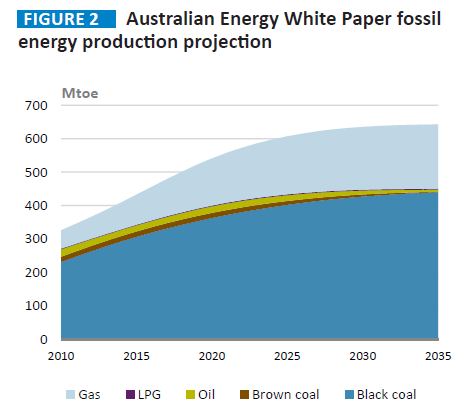

In particular the forecasts produced by the Bureau of Resource and Energy Economics play a pivotal role in reinforcing the view not just of Tony Abbott but Canberra more generally, that Australia's economy will rise on the back of an expansion in the use of fossil fuels. According to BREE the outlook for fossil fuels (as shown below) is onward and upward, and this fed directly into the last Energy White Paper produced under Labor.

Figure 2: Australian Energy White Paper fossil energy production projection

Source: Beyond Zero Emissions (2014) A fossil economy in a changing world

But what if they're wrong? What if world leaders from the US to China, Germany, UK, France and South Korea – to name just a few – really were serious when they say they believe global warming to be a grave threat to the welfare of future generations? What if they did decide to back up their words with deeds?

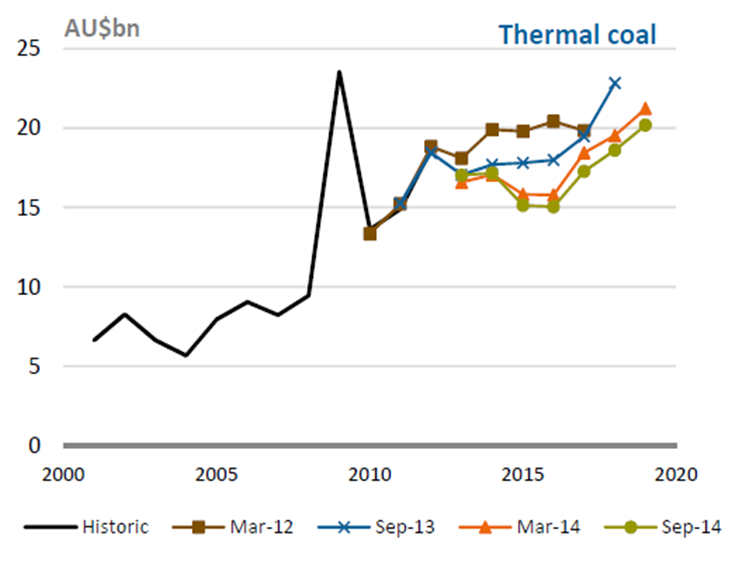

Since that original Energy White Paper forecast was produced, BZE points out that BREE has found itself having to repeatedly revise down its forecasts for thermal coal export revenue as shown below.

Figure 3: BREE thermal coal export revenue projection revisions

Source: Beyond Zero Emissions (2014) A fossil economy in a changing world

But maybe these revisions represent a short-term anomaly, what about the longer term?

Well for the BREE forecast to still remain correct, based on BZE analysis Australia's domestic and exported emissions would need to be allowed to double to 2.5 gigatonnes of CO2 per annum. Meanwhile the rest of the world, to have contained global warming with around a 50 per cent chance to less than 2 degrees, would have dramatically lowered overall emissions.

Putting this together comes up with an implausible result: Australia's fossil fuel production would be allowed to grow from 3.6 per cent of the world's emissions to 16 per cent. Is this really realistic?

While lobbyists in the fossil fuel industry are very fond of quoting the International Energy Agency's World Energy Outlook to suggest that growth of coal and gas is inevitable, they tend to neglect the fact that the Outlook contains several scenarios, not just the one they quote from. In addition to a reference scenario the IEA also prepares projections of demand for different energy sources based on two other scenarios:

– New Policies Scenario: this takes into account not only existing already implemented energy and climate policy commitments but also assumed implementation of those policies recently announced, albeit in a cautious manner.

– 450ppm Scenario: which looks at an idealised path for the globe to stabilise greenhouse gas emissions at 450 parts per million in CO2 equivalent

BZE have taken the relatively simple step of comparing BREE's forecasts against the alternative scenarios by the IEA where governments do act to contain their emissions.

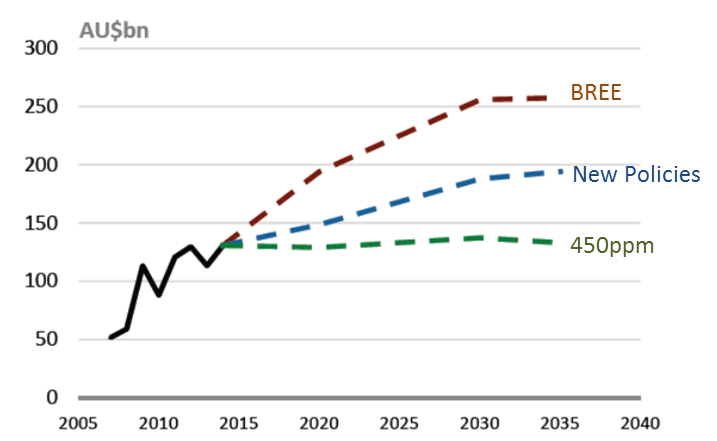

The chart below tells the story. The high case in brown is BREE's forecast of gross revenue from Australia's exports of gas, thermal coal, metallurgical coal and iron ore. The middle case (blue) is derived from the IEA's 'New Policies Scenario' and the low case (green) from their '450ppm Scenario'.

Figure 4: Comparison of total gross revenue from exports of gas, thermal and metallurgical coal and iron ore under BREE and IEA projections assuming action on carbon emissions.